The oil market continues to send mixed signals, with a pending U.S.-China trade deal and potential production cut extension--or deepening--by OPEC counterbalanced by rising crude inventories and an ominous warning about a looming oil glut by the IEA. Oil prices have mostly been treading water in this sea of uncertainty, with WTI prices sitting nearly 8% above the one-month low of $54.18 per barrel.

Yet, even in the event that the bulls end up carrying the day, they might soon have to contend with yet another monster: a contango.

After remaining at or near backwardation for much of the year, the oil market has returned to contango--a situation that could punch big holes in any gains by oil futures traders.

Contango and Backwardation

Contango and backwardation are terms commonly used in commodity futures markets.

A contango market is one where futures contracts trade at a premium to the spot price. For example, if the price of a WTI crude oil contract today is $60 per barrel but the delivery price in six months is $65, then the market is in contango.

In the reverse scenario, supposing the price of a WTI crude oil contract today is $60 per barrel but the delivery price six months down the line is $55, then the market is said to be in backwardation.

A simple way to think of contango and backwardation is: Contango is a situation where the market believes the future price is set to be more expensive than the current spot price, whereas backwardation is said to occur when the market anticipates the future price to be less expensive than the current spot price. Related: Airstrikes Disrupt Production At Libyan Oilfield

The premium future price for a particular contract is usually associated with the cost of carry that includes storage costs and risk of obsolescence.

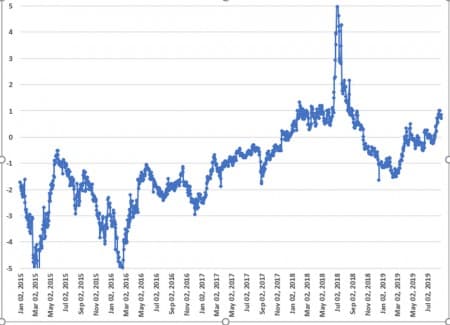

U.S. Futures Prices: 1st Month Minus Fourth Month Contract

Source: Forbes

In the chart above, a negative reading indicates backwardation while a positive one indicates contango. Backwardation indicates a bearish situation while contango portends the opposite.

To understand why contango and backwardation matter, it's important to understand that the vast majority of futures traders have no intention of handling the underlying physical commodity once their futures contracts expire--which would be impractical anyway for traders with contracts for hundreds of thousands or millions of barrels of oil.

Rather, these traders and speculators find other traders who are willing to hold their contracts to expiration and, in many cases, buy new replacement contracts (aka contract rolling).

In a contango market, the price of the replacement futures contracts is higher than the contract just sold, which in effect creates a small but significant loss that can quickly add up to potentially huge losses in time.

To understand the serious ramifications that contango can have on your portfolio, consider that the United States Oil ETF (NYSEARCA:USO), one of the most popular energy ETFs that rolls its contracts every month, pays high premiums on oil futures contracts (contango) that can cost investors anywhere from 10-80% per year.

Getting around contango

At this juncture, many readers might wonder why traders even bother investing in oil futures at all, especially when you consider that contango has occurred in the oil markets about 60% of the time over the past decade.

Given the ongoing volatility in oil markets, investing in the oil futures markets is a decidedly risky venture. Nevertheless, there are a few methodologies that traders can use to circumvent this challenge.

#1 Constantly monitor the futures curve

The most obvious solution to skirt the negative effects of contango is by constantly monitoring the futures curve and only investing in the market when it’s in backwardation.

When the curve is sloping upwards, trading futures contracts will erode your capital especially if you do it frequently. As USO has demonstrated, the cost over the course of the year could nearly wipe out your capital.

#2 Invest directly in oil companies

Another obvious solution is to avoid the futures market altogether and invest directly in oil companies instead.

Investing directly in companies that drill, distribute and/or sell oil is a reasonable alternative to holding oil futures. Related: The Natural Gas Nation Every Exporter Is Targeting

However, it’s also important to bear in mind that many of these companies frequently fail to accurately track oil prices closely enough--and the difference can be pretty dramatic.

For instance, in 2008 during the oil mega-bull market, oil prices climbed 200% compared to an 88% gain by oil and gas giant, Exxon Mobil Corp. (NYSE:XOM).

Another reasonable, if not precise, method is by investing in large energy ETFs such as Vanguard Energy ETF (NYSEARCA:VDE) and the Energy Select Sector SPDR ETF (NYSEARCA:XLE) that offer diversified exposure to the industry.

The biggest risk of investing in these ETFs is that they frequently display large tracking errors because they invest in both oil and gas companies whereas price movements by the two commodities do not necessarily correlate. They also invest in exploration & drilling, equipment & transportation companies whose performance is not directly tied to energy prices.

Luckily, there are ETFs that track non-integrated oil companies. These include SPDR S&P Oil & Gas Exploration & Production ETF (NYSEARCA:XOP) and iShares U.S. Oil & Gas Exploration & Production ETF (BATS:IEO). These are not without risk, though, since they also invest in small companies that are hugely volatile due to idiosyncratic factors that may be unrelated to oil prices.

#3 Use a hybrid model

So far, we have observed that each methodology that tries to avoid the negative effects of contango has its own limitations due to the how the company or exchange traded fund operates.

Therefore, we can surmise that the best way to get around the problem is by employing a hybrid model whereby you invest in the cheapest futures contract that optimizes between USO, PowerShares DB Oil ETF (NYSEARCA:DBO) and the United States 12 Month Oil ETF (NYSEARCA:USL) when the futures curve is in backwardation, then shift to general energy ETF such as XLE, IEO or VDE when it’s in contango.

This methodology certainly requires a little more elbow grease and constantly keeping an eye on the futures curve to identify any flipping points. However, it can potentially yield better results than the other two methodologies executed in isolation.

By. Charles Kennedy for Oilprice.com

More Top Reads From Oilprice.com:

- Reuters Confirms That Iran Was Behind The Saudi Oil Attacks

- IEA Warns Of A Looming Oil Glut Ahead Of OPEC Meeting

- OPEC Optimism Lifts Oil Prices