Markets have hit a rough patch – and oil is on the negative end of just about every indicator that appeared in the last week. Let’s go through them all and perhaps try to find where the light at the end of the tunnel might appear.

First to consider are the equity markets at large. No one can ignore the pressure that particularly EM and European markets have been under in recent weeks, and in the last weeks that pressure was transferred to the US markets through a small rise in interest rates from the Federal Reserve. Since then, equity markets have acted more bearishly, and this has created a general ‘risk off’ trade that has affected commodities as well. As we noted last week, indications of a hardening of the US/China trade war hasn’t helped matters either.

But on to energy specifically – here are the three biggest trends have negatively impacted oil.

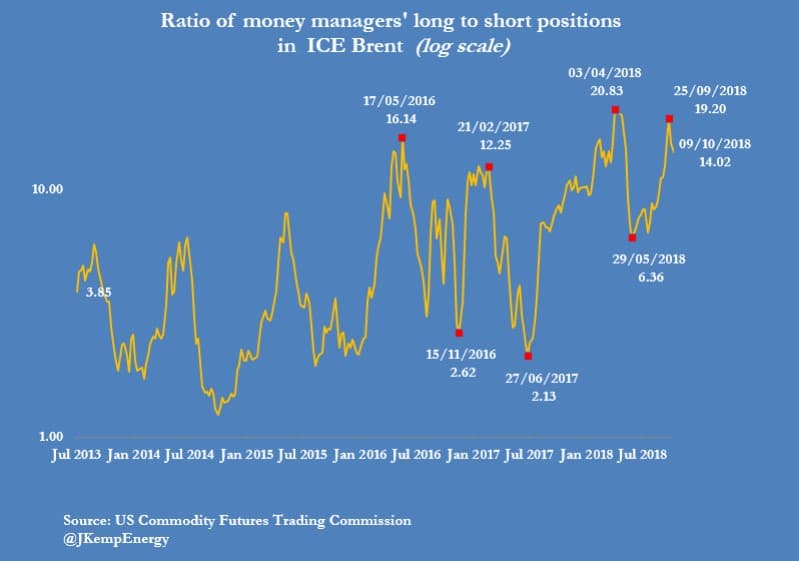

1 – The withdrawal of hedge fund money from futures. We noted the historically high ratio of longs to shorts in futures in this column two weeks ago, and mentioned the likelihood of a sell-off in oil based solely on those positions being liquidated – below the ratio from September 25th:

(Click to enlarge)

And the contrasting chart on October 10th:

(Click to enlarge)

All indications are this withdrawal of money from oil positions will continue to pressure markets for a while yet, but on the positive side, sets up for a strong rally when positions inevitably are re-initiated…

Markets have hit a rough patch – and oil is on the negative end of just about every indicator that appeared in the last week. Let’s go through them all and perhaps try to find where the light at the end of the tunnel might appear.

First to consider are the equity markets at large. No one can ignore the pressure that particularly EM and European markets have been under in recent weeks, and in the last weeks that pressure was transferred to the US markets through a small rise in interest rates from the Federal Reserve. Since then, equity markets have acted more bearishly, and this has created a general ‘risk off’ trade that has affected commodities as well. As we noted last week, indications of a hardening of the US/China trade war hasn’t helped matters either.

But on to energy specifically – here are the three biggest trends have negatively impacted oil.

1 – The withdrawal of hedge fund money from futures. We noted the historically high ratio of longs to shorts in futures in this column two weeks ago, and mentioned the likelihood of a sell-off in oil based solely on those positions being liquidated – below the ratio from September 25th:

(Click to enlarge)

And the contrasting chart on October 10th:

(Click to enlarge)

All indications are this withdrawal of money from oil positions will continue to pressure markets for a while yet, but on the positive side, sets up for a strong rally when positions inevitably are re-initiated – at lower crude prices.

2 – Stockpiles in U.S. crude surprisingly increase. U.S. crude stockpiles increased 6.5m barrels, not an unusual increase to see, but at a very unusual time of the year. Some of this was clearly related to overhang from Gulf storms during late September and early October, but also to the secondary transport services of train and truck that has been helping to withdraw crude where pipelines are already oversubscribed. The chart below shows how unusual these two last stockpile increases were compared to the previous year, in yellow, and the last 10 as well:

(Click to enlarge)

Finally, the brutal murder of Saudi journalist Jamal Khashoggi in Istanbul has left a pall over the Saudi government, and therefore the leaders of OPEC. While one might think that this event should have nothing whatsoever to do with how energy markets will trade, the truth is that the Saudis require the confidence of the US government to operate freely on many levels – and no one wants to invest in the price of an oil barrel that is currently in conflict with its prime Western ally. All threats of Saudi retaliation if pressed on the Khashoggi matter are mere wind, and one of two outcomes will need to happen before oil can resume a constructive course: Either the matter will slowly be forgotten, or the Saudis will make reparations without admitting guilt. Until one of these two outcomes comes to pass, we shouldn’t plan on oil to regaining the confidence of traders.

(Click to enlarge)

In general this has all translated to a mini-bear market that has overcome both oil and U.S. equities at large – and we must wait to see a change in one if not all three of these indicators before we’ll again be confident in the resumption of oil’s price rise.

To access this exclusive content...

Select your membership level below

COMMUNITY MEMBERSHIP

(FREE)

Full access to the largest energy community on the web