Friday September 7, 2018

In the latest edition of the Numbers Report, we’ll take a look at some of the most interesting figures put out this week in the energy sector. Each week we’ll dig into some data and provide a bit of explanation on what drives the numbers.

Let’s take a look.

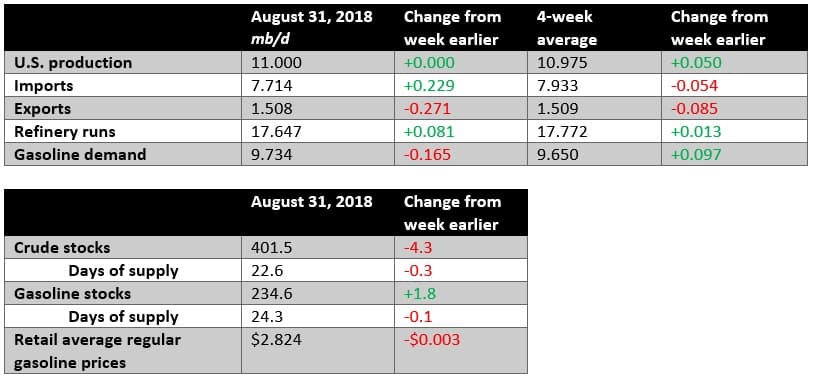

(Click to enlarge)

Key Takeaways

- Crude inventories fell again, dipping close to the 400-mb range.

- However, gasoline inventories rose, offsetting some of the crude draw.

- Oil prices fell after the mixed numbers were released, perhaps overshadowed by larger factors such as the threat of a trade war escalation.

1. DUC list continues to grow

(Click to enlarge)

- The number of drilled but uncompleted wells continues to grow, hitting 8,033 in July, up from 5,504 at the start of 2017 and 7,198 in January 2018.

- The Permian accounts for a large slice of the DUC backlog, with the total standing at 3,470 in July.

- According to the FT, executives from Schlumberger (NYSE: SLB) and Halliburton (NYSE: HAL) admitted at an industry conference that drilling activity in the Permian was slowing down, reducing their leverage in pricing negotiations with oil producers.

- Halliburton’s CEO said that the shale slowdown, combined with some project delays in the Middle East, will reduce quarterly earnings by 8-10 cents per share. The company’s stock fell by nearly 6 percent on that statement.

- Schlumberger’s CEO said that the…

Friday September 7, 2018

In the latest edition of the Numbers Report, we’ll take a look at some of the most interesting figures put out this week in the energy sector. Each week we’ll dig into some data and provide a bit of explanation on what drives the numbers.

Let’s take a look.

(Click to enlarge)

Key Takeaways

- Crude inventories fell again, dipping close to the 400-mb range.

- However, gasoline inventories rose, offsetting some of the crude draw.

- Oil prices fell after the mixed numbers were released, perhaps overshadowed by larger factors such as the threat of a trade war escalation.

1. DUC list continues to grow

(Click to enlarge)

- The number of drilled but uncompleted wells continues to grow, hitting 8,033 in July, up from 5,504 at the start of 2017 and 7,198 in January 2018.

- The Permian accounts for a large slice of the DUC backlog, with the total standing at 3,470 in July.

- According to the FT, executives from Schlumberger (NYSE: SLB) and Halliburton (NYSE: HAL) admitted at an industry conference that drilling activity in the Permian was slowing down, reducing their leverage in pricing negotiations with oil producers.

- Halliburton’s CEO said that the shale slowdown, combined with some project delays in the Middle East, will reduce quarterly earnings by 8-10 cents per share. The company’s stock fell by nearly 6 percent on that statement.

- Schlumberger’s CEO said that the market for fracking had “already softened significantly more than we expected” in the third quarter.

2. Without pipelines, Canadian oil moving by rail

(Click to enlarge)

- Last week, a Canadian court shot down a permit for the Trans Mountain Expansion project, a major pipeline recently nationalized by the Canadian government.

- The court decision throws the entire project into doubt. At a minimum, the decision delays the project by a year, pushing its in-service date off until 2022-2023, according to Scotiabank.

- Oil-by-rail shipments in Canada reached an all-time high of 205,000 bpd in June, up from 134,000 bpd as recently as February, and up from nearly zero before 2012.

- Shipping oil by rail will come increasingly commonplace with Alberta’s key pipelines on the sidelines.

- “[I]n a world where Line 3 is built but [Trans Mountain Expansion] and [Keystone XL] have stalled indefinitely, the additional demand for oil-by-rail will approach more than 400 kbpd by the mid-2020s, a 200% increase over current, already record-setting levels,” Scotiabank wrote in a note.

3. New FIDs picking up

(Click to enlarge)

- The oil market will continue to tighten, and Brent oil prices could average $75 in 2020, according to Barclays. The investment bank says it is bullish on oil, much more so when it issued its medium-term oil market forecast of $55 last year, but still says that “we are not on the cusp of another boom cycle in oil prices because of an impending ‘supply gap.’”

- A number of analysts, including the IEA, have repeatedly warned that the low rate of investment in upstream production, down sharply since the 2014 market meltdown, is sowing the seeds of a supply crunch in the early 2020s.

- Barclays’ report this week dismissed that concern. The bank argued that investment is returning, even if it remains subdued compared to pre-2014. “New projects approved from 2014 to 2018 will materially add to supply between 2020 and 2025,” Barclays said, estimating that projects approved over the last five years will translate into 3.5-5.4 mb/d of fresh supply between 2020 and 2022. And, notably, that’s just from non-OPEC countries and from non-shale resources.

- Acknowledging the shorter queue of projects due to a sharp reduction in investment in the years after the 2014 price collapse, Barclays nonetheless said it is not a major concern. “[O]ur detailed modelling still suggests that the gap that may emerge will be deferred to 2024 and beyond and may not be as big.”

4. OPEC has high “fiscal breakeven” prices

(Click to enlarge)

- OPEC (along with its non-OPEC partners) has managed to rebalance the oil market and significantly push up oil prices over the past two years. Going forward, reports suggest that Saudi Arabia, OPEC’s most powerful member, wants oil prices to trade within a range of $70 to $80 per barrel.

- “The Middle East is the world’s most unequal region, in which the top 10% of citizens receive more than 60% of total income,” Barclays said in a note. Worse, the inequality is often along sectarian lines.

- “With these tensions, certain OPEC countries have a fiscal incentive to try to keep prices within a band above $70/b,” Barclays concludes.

- These oil-producing states have heavy social spending requirements. Saudi Arabia, for instance, will need oil to average $78 per barrel for its budget to breakeven. Bahrain needs $111 per barrel, Algeria $84, Iran $72, Libya $114, and so on.

- The upshot is that with OPEC back to managing the market, after a hiatus between 2014 and 2017, there is a good chance that the group will cut production if prices drop below the desired range. At the very least, Saudi Arabia may act unilaterally, if it can, to cut output when prices drop below $70.

5. Frac sand demand soaring

(Click to enlarge)

- Sand used in hydraulic fracturing has been soaring over the past few years, but growth is expected to continue rocketing upwards.

- Drillers in West Texas have historically had to ship in sand from mines in Minnesota and Wisconsin, at high cost.

- New sand mines are opening in Texas, and 20 are expected to be active right now, according to the Wall Street Journal.

- In fact, there could be too much sand supply, endangering mining projects. Sand supply is hitting the market at the same time that the Permian is entering a lull, with drillers throttling back because of pipeline constraints.

- Still, sand demand is at a record high, up 29 percent in the second quarter compared to a year earlier, according to the WSJ and IHS Markit. The Permian will account for half of sand demand by 2023.

Heard on the Street

Saudi Arabia preys on Iranian weakness:

“The shortfall in Iranian oil exports is prompting competitors to rethink their sales strategy. We believe this is also why Saudi Arabia has decided to raise its official October selling prices for shipments to Europe and to lower them for Asia.” – Commerzbank

U.S. sanctions on Iran increase odds of conflict:

“An unintended military escalation through miscalculation continues to be one of the most underappreciated risks in our view…Even if the probability of such a scenario remains relatively low, it would serve as the ultimate high-impact event for oil prices.” – RBC Capital Markets

Oil market is tighter than we thought:

“The oil market has changed since our last report in July 2017. US producers are resisting temptation and exercising capital discipline, OPEC and Russia have convinced market participants they are managing the supply of over half of global production, the US is using sanctions more actively, and several key OPEC producers are at risk of being failed states...In our fourth annual medium-term price forecast, we revise our price forecast for 2020 markedly upward from $55 to $75 Brent. We remain bullish on prices by 2025.” – Barclays

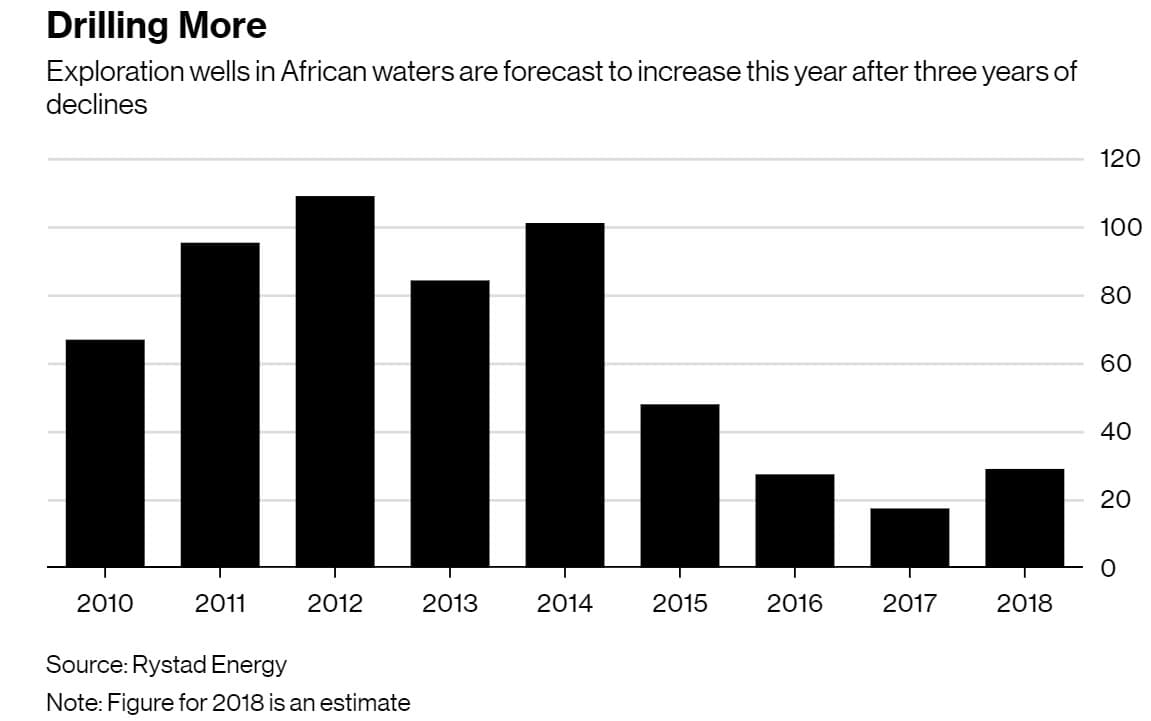

6. Oil industry returns to Africa

(Click to enlarge)

- The oil industry is going back to Africa, after withdrawing during the oil market downturn that began in 2014.

- “The majors starting to move into these areas for exploration again is probably the first sign of things picking up,” Adam Pollard, an analyst at consultant Wood MacKenzie Ltd., told Bloomberg. He said Africa “may be one of the first to get hit when the price goes against explorers, but equally it’s perceived to be one of the places where people are keen to get involved when the price is supportive.”

- The Baker Hughes rig count for Africa shows the number of rigs back up close to 100 onshore rigs as of July, up a fifth from 2016 levels. The number of offshore rigs stands at around 60, the highest in two years.

- According to Rystad Energy, the oil industry will drill 29 offshore wells this year, compared to just 17 last year.

7. Emerging market contagion a downside risk

(Click to enlarge)

- Emerging markets continue to get slammed. An index of emerging market stocks fell towards bear territory. Meanwhile, a basket of emerging market currencies is at its lowest since May 2017.

- This week, Saudi Arabia and Indonesia saw their indices slide. Argentina still looms as arguably in the most imperiled economy, with the peso down more than 50 percent on the year.

- In South Africa, factories reported the sharpest decline in output in more than two years in August, pushing the rand down further. South Africa entered a recession in the second quarter.

- Some analysts argue that these are country-specific problems and not indicative of a broader emerging market contagion, others are not so sure.

- It’s “no longer just about EM fundamentals,” Sameer Goel, the head of macro strategy for Asia at Deutsche Bank AG in Singapore, said in a Bloomberg TV. It’s “increasingly about contagion, which largely happens because of cross-holdings and the pressure of redemptions.”

That’s it for this week’s Numbers Report. Thanks for reading, and we’ll see you next week.