One of the most spectacular stories of 2019 started off in the first days of the outgoing year. Some 150 kilometers off the Nigerian coast, the oil major Total and its project partners brought onstream the Egina FPSO, the largest-ever built by the French firm. Then most of the news revolved around the new approaches employed for the purpose – most notably a third of the FPSO modules were built in Nigeria, boosting the project’s localization statistics. Yet as 2019 comes to a close, one can say with sufficient certitude that Egina has effectuated something which was previously unthinkable. Not only did it become the most expensive Nigerian crude, it conquered the European continent and became something of a brand there.

First, let’s look at the dry numbers. Egina is heavier than the average Nigerian crude, standing at 27.5 degrees API yet shares the low Sulphur content of its offshore peers at 0.17 percent. Given its high gasoil yield, the relative heaviness of Egina helped to transform it into a sort of ideal grade to refine for firms that aim to create IMO 2020-compliant bunker fuel. Total was hoping for something similar when it launched production in January 2019, however the divergence of Egina versus all the other grades became surprisingly wide in the past 2 months. The January 2020 official selling price (OSP) of Egina was set by NNPC at a $4.35 per barrel premium against Dated Brent, whilst other Nigerian grades were assessed at a $2.5-3 per barrel premium (see Graph 1).

Graph 1. Nigerian official selling prices (OSPs).

Source: NNPC.

Since OSP only give a certain indicative price range, they do not reflect Egina’s real market value which was recently assessed at a roughly $6 per barrel premium for FOB deliveries (late November witnessed trades going as high as a $7 per barrel premium). This is evidently also true for Bonny Light or Forcados, too, yet Egina’s pullaway is by any standard noteworthy. One year ago, Egina was on par with Forcados, one of the main winners of the pre-IMO 2020 period, today it yields an almost $1.5 per barrel premium over it. So, what is that unique about Egina? Briefly put, being distillate-rich and low in sulphur it turned out to be the ideal grade for Northwest European refiners (see Graph 2). All of the December loaders will end up in Europe, all but one did so in November 2019. Related: How Tech Is Making Oil Work Safer

Graph 2. Egina Exports in 2019 (kbpd).

Source: Thomson Reuters.

Refining Egina brings about a high yield of middle and vacuum distillates (around 80 percent in total), with gasoil accounting for more than half of the crude’s yields. High distillate yields throughout the second half of 2019 have compelled Europe’s refineries equipped with cracking units to see Egina as a highly suitable feedstock. Moreover, somewhat in contrast to some West African peers, the crude’s acidity is not a problem either – at 0.24 mg KOH/g it stands much better than rival Bonga (0.46 mg KOH/g) or Djeno (0.70 mg KOH/g), which anyways move predominantly eastwards. Still, given their preference for heavier low-sulphur crudes ti is remains an open question whether Asian refiners, especially Chinese ones, would like to include more Egina in their refining slates.

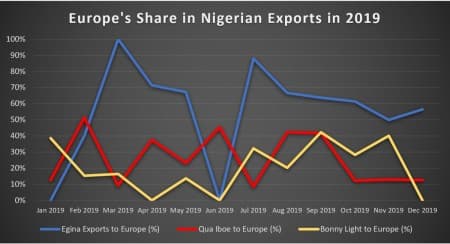

Graph 3. Europe’s Share in Nigerian Exports in 2019.

Source: Thomson Reuters. Related:Will Oil Bulls Rule 2020?

Interestingly, as soon as Egina ramped up production to its expected plateau of 200kbpd, Nigeria’s state oil company NNPC started to claim that Egina should be excluded from the West African country’s OPEC production tally as it is a condensate and not oil. This raised some eyebrows in the oil community as condensates generally have an API density of 45 degrees and higher, there is no precedent for crudes of 27 degrees API to be considered condensate. In an attempt to fortify its claim vis-à-vis OPEC, the Nigerian oil minister went to explain that the Egina field produces only 30-40 percent of crude, whilst the rest of production is condensate. Nigeria’s new 2020 OPEC quota is 89kbpd higher than before (1.774mbpd now versus 1.685mbpd before) – in a move that was not covered widely in media as Nigeria’s non-compliance with the Vienna agreements seems already to become the norm – hence, some leeway was made for new oil output from Egina.

With the above being said, what comes next after this? The Egina project, at 16 billion overall cost, was the most expensive one Nigeria has heretofore witnessed, yet recent moves by the Nigerian government which is poised to increase its tax intake from deepwater fields may indicate that another project of this scale might not be around the corner anytime soon. Egina was the second field to be commissioned from the Oil Mining Lease (OML) #130, after shareholders CNOOC (45%), Total (24%), Petrobras (16%) and SAPETRO (15%) launched Akpo in 2009. The 200MMbbl Preowei field might be the following project brought onstream, perhaps even by means of a tie-in to the Egina FPSO, however the assumed 2019 final investment decision did not materialize and was postponed into 2020, most probably because of the government’s royalty tinkering. Thus, the future of Nigerian deepwater might be tangibly slower than anticipated.

By Viktor Katona for Oilprice.com

More Top Reads From Oilprice.com:

- Is The Shale Boom Running On Fumes?

- Why This Oil Price Rally Won’t Last

- U.S. Shale Will Grow Regardless Of Oil Prices