There has been much talk lately about a potential oil glut in 2020, most notably by the IEA in their latest monthly oil report, but such predictions are predicated on two faulty assumptions, first being global oil demand estimates are accurate, and the second, strong US shale supply growth will continue unabated regardless of prevailing oil prices.

2020 Balances

A quick analysis of the IEA latest 2020 demand-supply balance indicate a potential 900,000 barrels daily surplus, if true, such a surplus is bound to weigh heavily on prices. Diving deeper into the numbers we notice that IEA expects global oil demand to average 101.7M barrels next year against a potential 102.6M barrels in global supply (should OPEC maintain its current 30M barrels in production). Looking at these numbers, right away a problem arises, namely the IEA is notorious for underestimating the actual level of global oil demand. For those familiar with the IEA tables, the IEA reconciles differences between supply and demand under the seemingly innocuous item labelled Miscellaneous to Balance. For the uninitiated this is what it means: When global oil supply and demand are at a given level, the difference between them (they are rarely exactly balanced) should translate either into an increase or decrease in physical oil inventories, but when the difference does not manifest itself in physical stocks, the IEA introduces the difference on paper under the Miscellaneous to Balance item.

(Source: IEA)

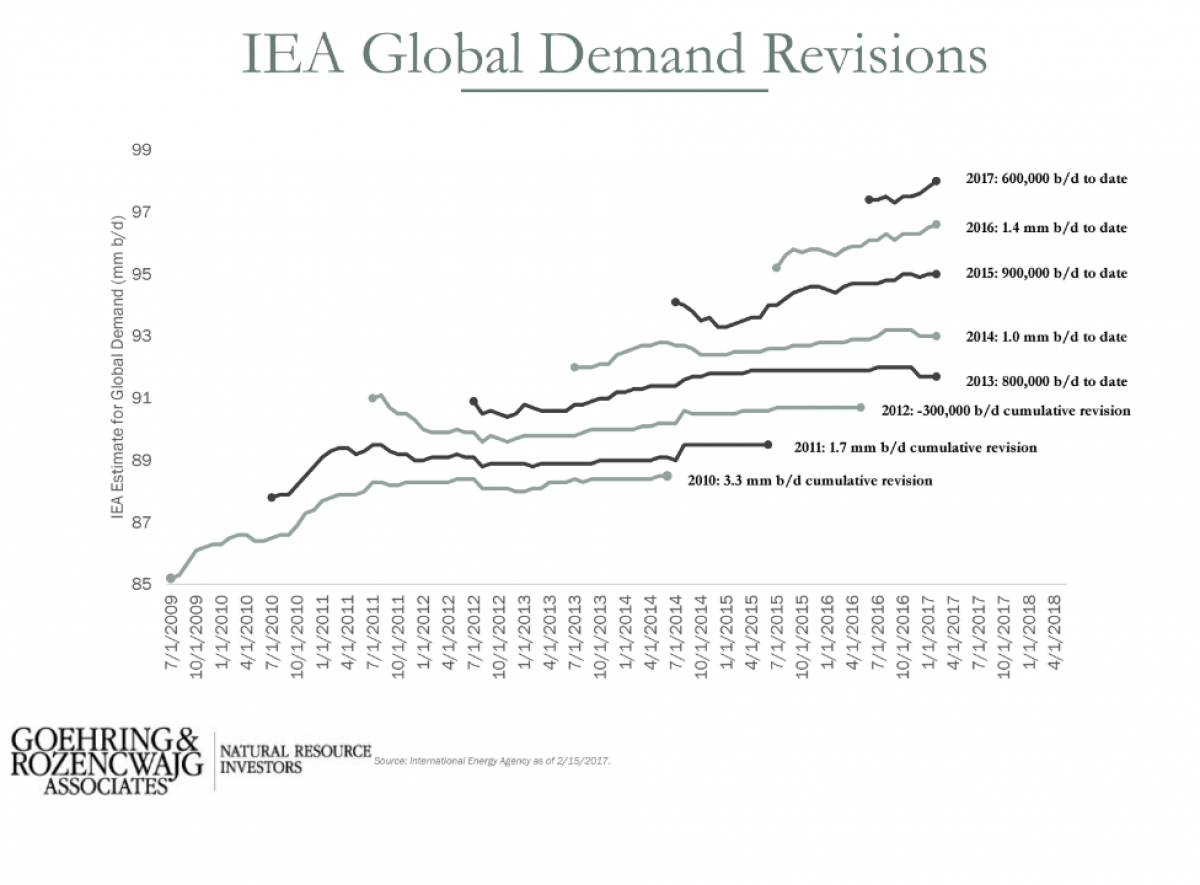

The Missing 400M barrels!

In 2018, global oil supply averaged 100.3M barrels per day, while demand (according to the IEA) averaged only 99.1M barrels per day, thus actual traceable oil inventories should have increased by 1.2M barrels per day, or 438M barrels increase for the year. However, since these excess barrels did not show in the OECD commercial or governmental stocks, the IEA classified the missing 1.2M barrels under the Miscellaneous to Balance. It is of course possible that some of these missing barrels will be located later, and some may have ended in non-OECD inventories, but the likelihood that the totality of the 400M barrels imbalance is stored somewhere is highly unlikely.

(Source: IEA)

As can be seen from the above, actual traceable OECD petroleum stocks increased by mere 18M barrels in 2018 (Q4/17 to Q4./18) as compared to an estimated increase of 438M barrels increase. In Q4/18 alone the IEA balances signalled a 2.3M barrels daily imbalance between supply and demand (210M barrels excess for the quarter) yet the actual reported increase in OECD inventories in Q4/18 is only 5M barrels. Such discrepancy between actual stocks and projected stocks is not new, eventually the lion share of the missing barrels is captured as missed demand in developing countries. In 2017, the WSJ calculated the average upward oil demand revision by the IEA at 880,000 barrels per year over the prior seven years. Related: Renewable Natural Gas Close To Taking Off In U.S.

(Source: Goehring & Rozencwajg)

Considering the substantial 400M+ barrels gap between reported and actual inventories in 2018, base global oil demand last year (and by extension this year) will likely be revised materially higher in the coming months. An eventual 600,000 barrel upward revision to global demand (which will still leave us with over 200M barrels missing) would reduce the expected 2020 oil-demand imbalance by two thirds from 900,000 barrels per day to only 300,000 barrels per day.

Surging US Shale Growth

In its latest OMR, the IEA revised 2019 non-OPEC oil supply growth slightly higher to 2M barrels (from 1.9M the month prior) mostly due to an upward revision for US and UK supply. Meanwhile, 2020 non-OPEC supply was revised down to 2.1M (from 2.3M) largely due to downward revisions for Russia and Oman following the July OPEC+ deal. For both 2019 and 2020, US supply growth dominates non-OPEC supply growth, with US supply representing 90% of 2019 non-OPEC supply growth and 65% of the 2020 total.

(Source: IEA)

This rosy picture of US supply growth, most of which tied to strong growth in US shale basins, stands at a stark contrast to the recent slew of warnings by the major O&G service providers following the release of their Q2 results:

John Lindsay, CEO of Helmerich & Payne:

“Our expectation of seeing the bottom of the Company’s rig count during the quarter turned out to be premature as the full effect of the industry’s emphasis on disciplined capital spending continues to reverberate through the oil field services sector. As such, H&P exited the quarter in the U.S. with 214 active rigs, which was slightly below the low end of our guidance range. We are reluctant to predict another bottom and see further softening during our fourth fiscal quarter as our guidance would indicate.

Andy Hendricks, CEO of Patterson-UTI:

"E&P companies are being extra vigilant this year in monitoring their spend due to commodity price volatility and the increased focus on spending within their budgets. We believe E&P companies are slowing drilling and completion activity to smooth their spending run rate and reduce the risk of budget exhaustion later in the year. Our rig count, which averaged 158 rigs during the second quarter, is expected to average 142 rigs during the third quarter."

Pall Kibsgaard, CEO of Schlumberger:

“The cash flow focus amongst the E&P operators confirms our expectations of a 10% decline in North America land investments in 2019 ... We continue to see US shale oil as the only near- to medium-term source of global production growth, albeit at a slowing growth rate, as E&P operators continue to transition from an emphasis on growth to a focus on cash and returns, with consequent restraining effects on investment levels.”

Jeff Miller, CEO of Halliburton:

“I believe that our customers' activity cadence for the rest of the year will be dictated by their focus on remaining within their announced CapEx budgets and generating free cash flow. Some will slow down as they've been very efficient and will scale back completion programs for the rest of the year to stay within their CapEx guidance. Others may drop rigs, but will continue working down their docks. Majors will most likely continue executing their growth plans in the U.S. shale to meet their longer term objectives. As a result of these different customer behaviors, we expect that activity in North America will be slightly down in the third quarter.”

It’s worth noting that Halliburton has cut its North American workforce by 8% and idled a large number of rigs and fracking equipment as a result of the slowdown in North American drilling and fracking activity.

Core Laboratories, Q2 earnings press release:

“The average third quarter 2019 U.S. rig count is projected to be down. While operators continue to focus on generating FCF and returns on investment … As a result, Core projects U.S. onshore completion activity to be flat sequentially.”

Such warnings by O&G service providers should be viewed as an early warning system as to the future trajectory of US shale supply. Back in 2015, a similar wave of warnings (such as this and this) by US O&G service providers preceded a marked decline in US shale production growth the following year. Related: Norway Looks For Bigger Role In European Gas Markets

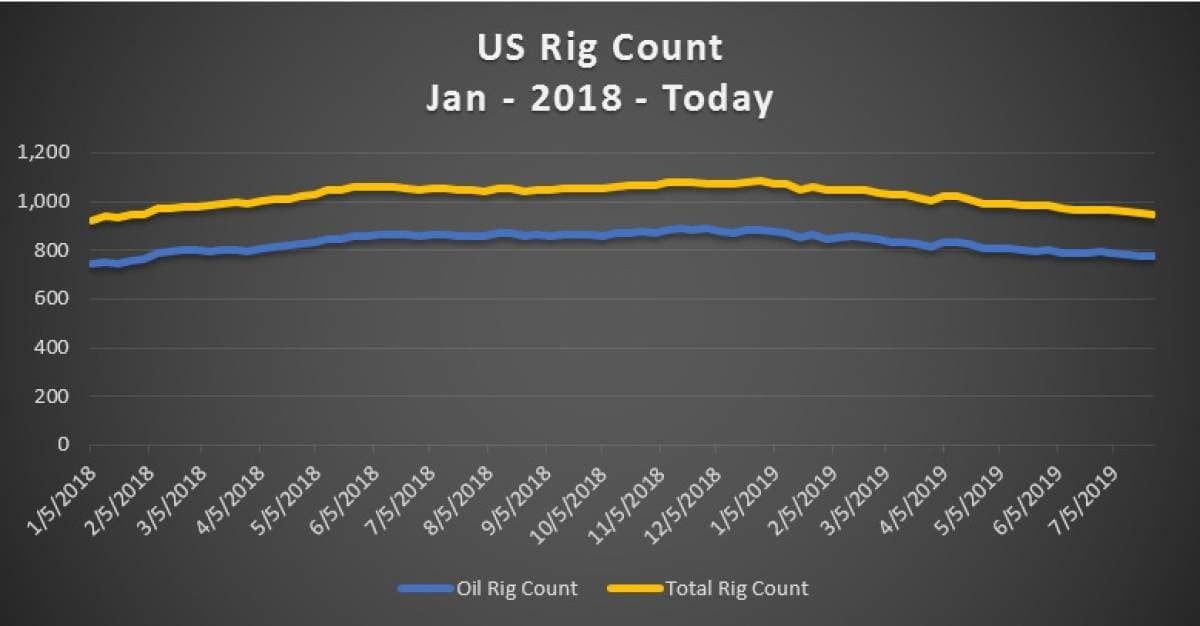

Beside O&G service providers slowdown warnings, the slowdown in US shale activity is clearly apparent in the 13% decline in the US rig count between December 2018 (1083 rigs) and today (946 rigs). Excluding natural gas focused rigs, the decline in the US oil rig count since the November 2018 peak stands at 112 rigs (888 rigs to 776 rigs).

(Source: Semper Augustus Capital, Baker Hughes)

On July 26th, upon analysing O&G service providers Q2 results, Altacorp, issued the following projection for the US rig count:

“The management teams guided to a reduction in rig count in the coming months, and we understand that E&Ps have been advising drilling contractors that they will be laying down rigs to stay within their budgets. It now appears that the US land rig count – after averaging around 960 in Q2/19 – may average around 880 in Q3/19 and around 860 by Q4/19.”

If Altacorp’s projection is accurate, the YoY decline in the US rig count by Q4/19 will stand at 20% or an approximate decline of 220 rigs in one year.

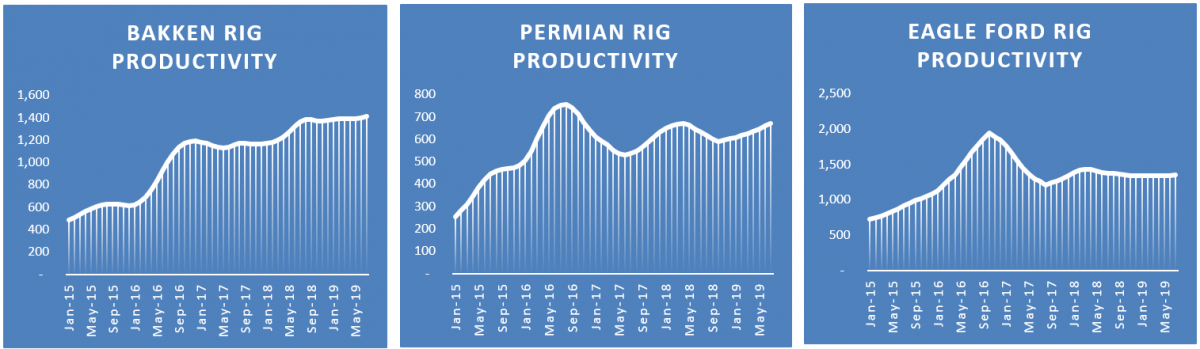

Historically, some of the decline (or at times the totality of the decline in the rig count) has been countered by an improvement in rig productivity, but even on that metric US production is set to disappoint with oil rig productivity improving by only 5.5% between November 2018 and July 2019, against a 13% decline in the oil rig count during the same period. As a matter of fact, US oil rig productivity in the three key US shale basins (Permian, Bakken and Eagle Ford) has hardly changed since mid-2018. Without a pickup in productivity, a 20% decline in the rig count by Q4, could translate into a potential flattening, if not an outright decline, in US shale production in 2020.

(Source: Semper Augustus Capital, EIA)

The vocal activity warnings by O&G service providers, the steady decline in the US rig count, and the flattening in US rig productivity does not argue for a material increase in US oil production. Between 2019 and 2020, the IEA projects US liquids supply to increase by a cumulative 3.1M barrels, if this increase was to slow by a mere 20% to 2.5M barrels as result of the slow down in drilling and fracking activity, the global oil supply balance in 2020 would dip into a 300K deficit (assuming a 600K Miscellaneous to Balance adjustment), and this is without factoring recent reductions in expected output by other non-OPEC producers such as Brazil which constitute a key component of the IEA 2020 non-OPEC supply projections.

Conclusion

The IEA chronic underestimation of global oil demand combined with the market erroneous belief in the unshakable resilience of US supply growth, is painting an overly bearish picture of the global oil demand-balance in 2020. As I have argued in the past (The New Oil Order) US shale has introduced a new dynamic oil market balancing force that official agencies (such as the IEA) are still struggling to properly account for in their projections. Historically, the IEA has struggled with capturing the exact level of global oil demand, understandably so, considering the vast scope of the oil market. Supply, on the other hand, was easier to project due to the concentrated nature of oil production in few OPEC countries and a handful of non-OPEC mega projects, but with the advent of shale, projecting global oil supply has become a challenging task as well. Consequently, when agencies such as the IEA are unable to properly track global demand and are unable to account for fast changes in US shale supply, one has to take their 2020 oil glut predictions with a grain of salt.

By Nawar Alsaadi for Oilprice.com

More Top Reads From Oilprice.com:

- The Permian Boom Is On Its Last Leg

- An Unusual Development In Natural Gas Markets

- Natural Gas Glut Is Crushing US Drillers

There is already a glut. Attempts to start a war in the Gulf won't reduce that glut for years.