“If you repeat a falsehood long enough, it will eventually be accepted as fact.”

In the financial markets, and economics, it is a common occurrence for the media and commentators to latch onto a statement which supports a cognitive bias. They then repeat that statement until it is a universally accepted truth.

When such a statement becomes universally accepted and unquestioned, well, that is when you should probably question it.”

Last week, I had a conversation with a friend of mine about the plunge in oil prices in recent weeks. One of the biggest fallacies about plunging oil prices, and subsequently lower gasoline prices, is that it is a huge windfall for consumers. Even President Trump stated as much last Wednesday morning. To wit:

Oil prices getting lower. Great! Like a big Tax Cut for America and the World. Enjoy! $54, was just $82. Thank you to Saudi Arabia, but let’s go lower!

— Donald J. Trump (@realDonaldTrump) November 21, 2018

But is that really the case?

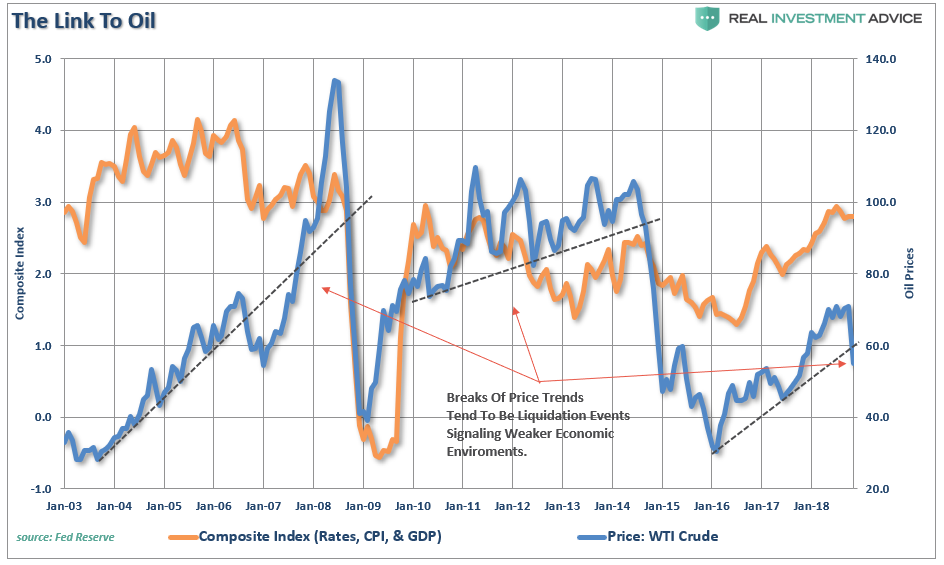

Oil prices are indeed important to the overall economic equation and, as I showed recently, there is a correlation between the oil prices and inflation, and interest rates.

“Oil is a highly sensitive indicator relative to the expansion or contraction of the economy. Given that oil is consumed in virtually every aspect of our lives, from the food we eat to the products and services we buy, the demand side of the equation is a tell-tale sign of economic strength or weakness…the chart combines rates, inflation, and GDP into one composite indicator to provide a clearer comparison. One important note is that oil tends to trade along a pretty defined trend…until it doesn’t. Given that the oil industry is very manufacturing and production intensive, breaks of price trends tend to be liquidation events which have a negative impact on the manufacturing and CapEx spending inputs into the GDP calculation.”

(Click to enlarge)

“As such, it is not surprising that sharp declines in oil prices have been coincident with downturns in economic activity, a drop in inflation, and a subsequent decline in interest rates“

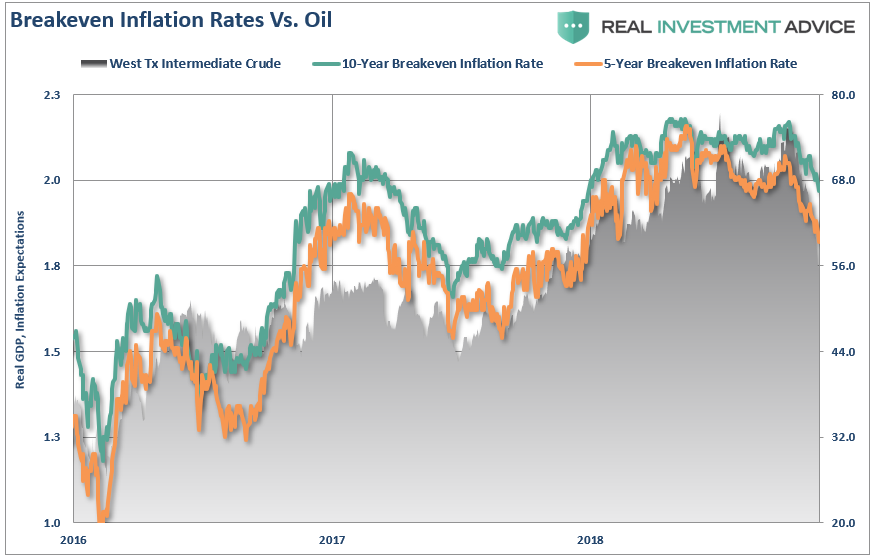

We can also view the impact of oil prices on inflation by looking at breakeven inflation rates as well. As I noted in “Oil Sends A Crude Warning:”

“The short version is that oil prices are a reflection of supply and demand. Global demand has already been falling for the last several months and oil prices are now waking up that reality. More importantly, falling oil prices are going to put the Fed in a very tough position in the next couple of months as the expected surge in inflationary pressures, in order to justify higher rates, once again fails to appear. The chart below shows breakeven 5-year and 10-year inflation rates versus oil prices.”

(Click to enlarge)

Zero Sum

The argument is that lower oil prices gives consumers more money to spend certainly seems entirely logical. Since we know that roughly 80% of households in America effectively live paycheck-to-paycheck, they will spend, rather than save, any extra disposable income.

Spending in the economy is a ZERO-SUM game as for each positive impact there is an equal and offsetting negative impact. Falling oil prices are an excellent example of this as gasoline sales are part of the retail sales calculation.

Let’s take a look at the following example:

• Oil Prices Decline By $10 Per Barrel

• Gasoline Prices Fall By $1.00 Per Gallon

• Consumer Fills Up A 16 Gallon Tank Saving $16 (+16)

• Gas Station Revenue Falls By $16 For The Transaction (-16)

• End Economic Result = $0

Now, the argument is that the $16 saved by the consumer will be spent elsewhere, which is true. However, this is the equivalent of “rearranging deck chairs on the Titanic.”

Related: Goldman: Oil Prices Set For Rebound In 2019

So, let’s now extend our example from above. Oil and gasoline prices have dropped so John, who has $100 to spend each week on retail related purchases goes to the gas station:

• Big John Fills Up His Truck For $60 (Used To Cost $80) (+$20)

• Big John Spends His Normal $20 Per Week On His Favorite Craft Beer

• Big John Then Spends His Additional $20 Savings On Roses For His Wife (He Makes A Smart Investment)

————————————————-

Total Spending For The Week = $100

Now, economists quickly jump on the idea that because he spent $20 on roses, there has been an additional boost to the economy. However, this is false. John may have spent his money differently this past week but here is the net effect on the economy.

Gasoline Station Revenue = (-$20)

Flower Show Revenue = +$20

—————————————————-

Net Effect To Economy = $0

(Click to enlarge)

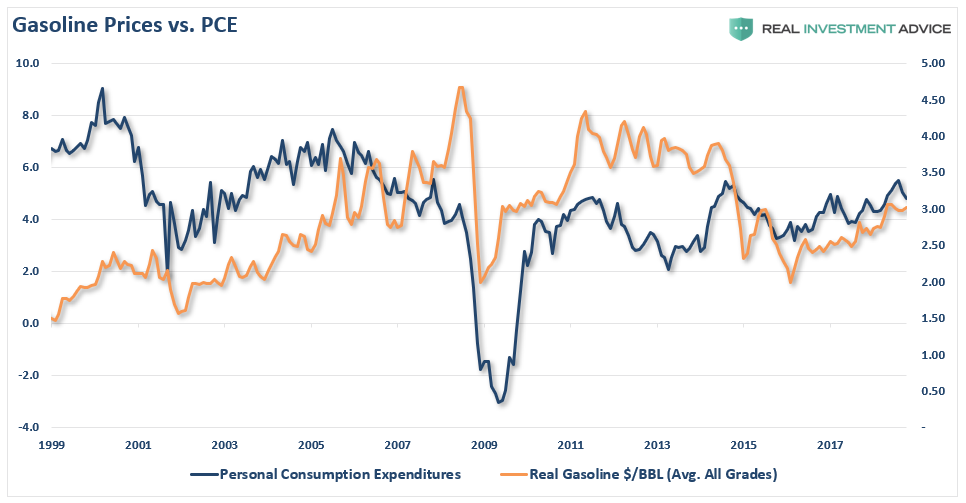

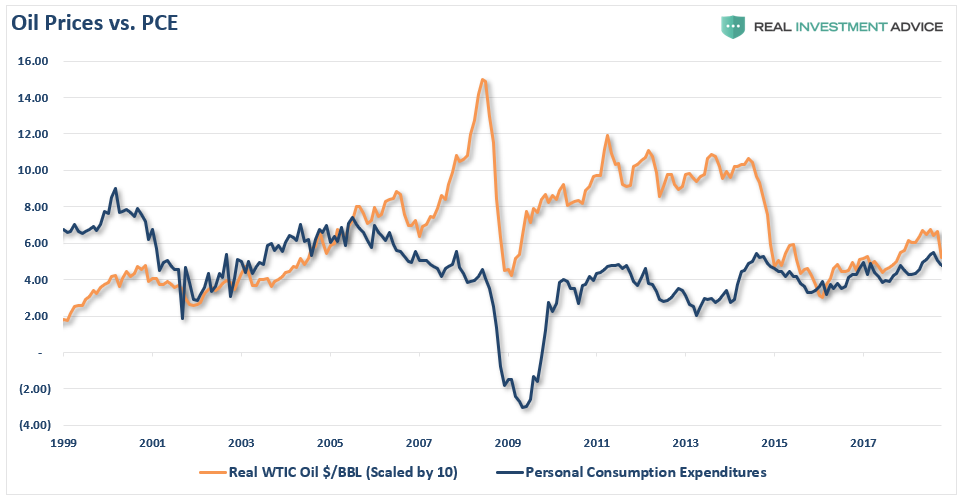

As shown, falling gasoline prices have historically equated to lower personal consumption expenditures and not vice-versa. In fact higher oil and gasoline prices have actually been coincident with higher rates of PCE previously. The chart below show inflation-adjusted oil prices as compared to PCE.

(Click to enlarge)

While the argument that declines in energy and gasoline prices should lead to stronger consumption sounds logical, the data suggests that this is not the case.

The only thing that will increase consumer spending are increases in INCOME, not SAVINGS. Consumers only have a finite amount of money to spend. They can choose to “save more” which is a drag on economic growth in the short-term (called the “paradox of thrift”) or they can spend what they have. But they can’t spend more.

A Bigger Drag Than The Savings

Another important issue to this analysis is that falling oil prices are a bigger drag on economic growth than the incremental “savings” received by the consumer.

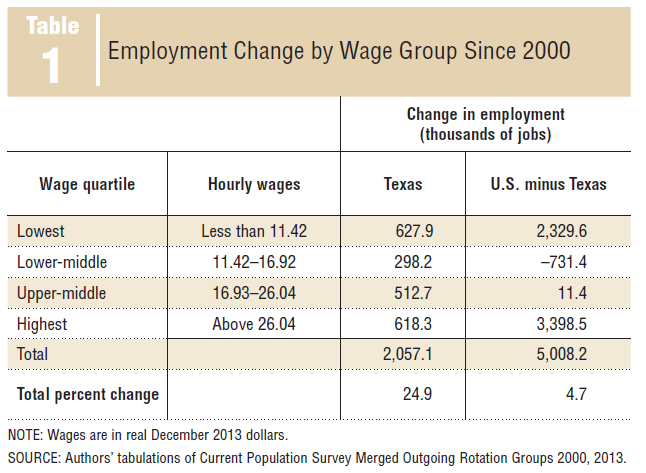

In 2014, when oil prices were plunging, I discussed the issue of the impact on oil and gas production as it relates to oil prices and the economy. To wit:

“Oil and gas production makeup a hefty chunk of the “mining and manufacturing”component of the employment rolls. Since 2000, when the oil price boom gained traction, Texas has comprised more than 40% of all jobs in the country according to first quarter data from the Dallas Federal Reserve.“

(Click to enlarge)

(Click to enlarge)

The obvious ramification of the plunge in oil prices is that eventually the loss of revenue will lead to cuts in production, declines in capital expenditure plans (which comprises almost 1/4th of all capex expenditures in the S&P 500), freezes and/or reductions in employment, and declines in revenue and profitability.

Related: The Oil Powerhouses Replacing OPEC

Let’s walk through the impact of lower-oil prices on the economy.

First, declining oil prices leads to declining revenue for oil and gas companies. Given that drilling for oil is a very capital intensive process requiring a lot of manufactured goods, equipment, supplies, transportation, and support, the decrease in prices leads to a reduction in activity as represented by Capital Expenditures (CapEx.) The chart below shows the 6-month average of the 6-month rate of change in oil prices as compared to CapEx spending in the economy.

(Click to enlarge)

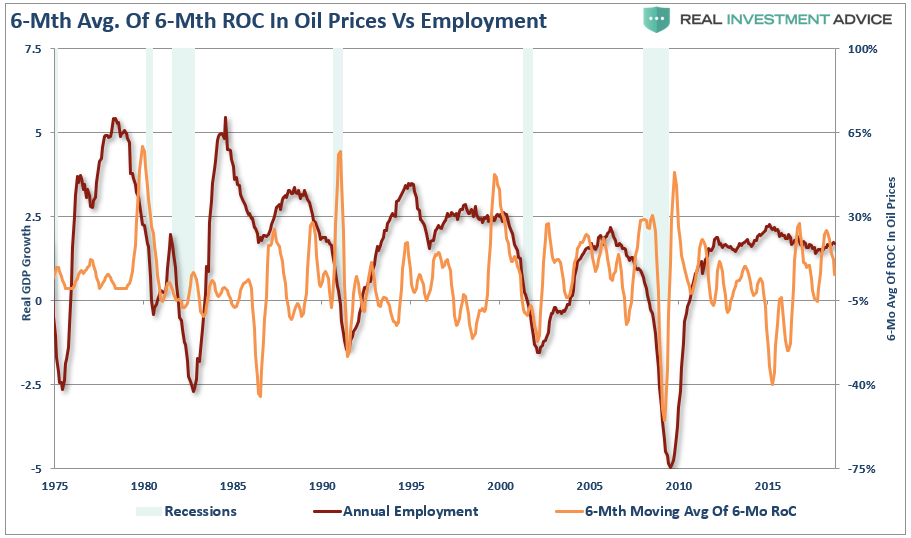

Of course, once CapEx is reduced the need for employment declines. However, since drilling for oil is a very intensive prices, losses in employment may start with the energy companies but all of the downstream suppliers are also impacted by slower activity.

(Click to enlarge)

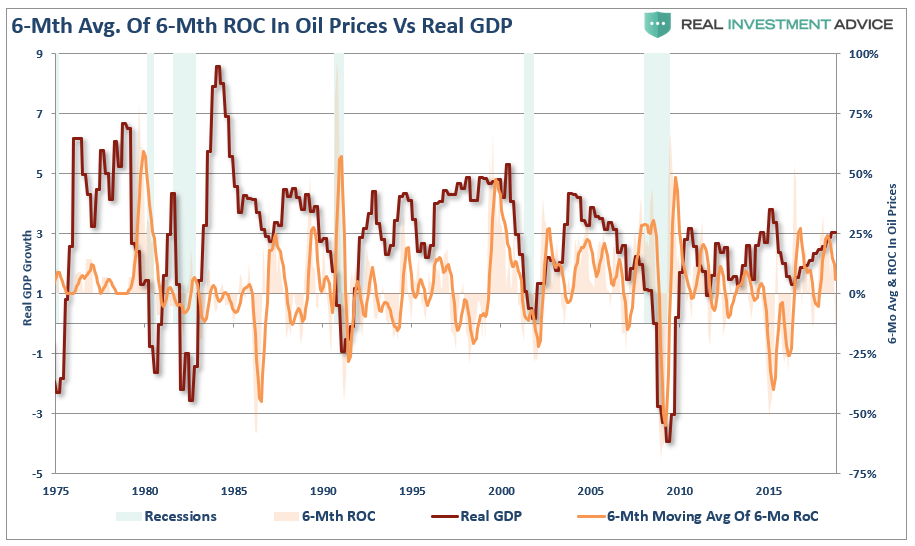

As job losses rise, and incomes decline, it filters into the economy.

(Click to enlarge)

Importantly, when it comes to employment, the majority of the jobs “created” since the financial crisis have been lower wage paying jobs in retail, healthcare and other service sectors of the economy. Conversely, the jobs created within the energy space are some of the highest wage paying opportunities available in engineering, technology, accounting, legal, etc. In fact, each job created in energy related areas has had a “ripple effect” of creating 2.8 jobs elsewhere in the economy from piping to coatings, trucking and transportation, restaurants and retail.

If oil prices, a reflection of global economic demand, remains depressed for a considerable period of time, the negative impacts of loss of employment, reductions in capital expenditures and declines in corporate profitability could outstrip any small economic benefit gained from lower oil prices. For those of us who have lived in Texas long enough to remember the oil rout in the early 80’s, the greatest fear going into 2019 is that oil prices remain low.

Simply put, lower oil and gasoline prices may actually have a bigger detraction on the economy than the “savings”provided to consumers.

Newton’s third law of motion states:

“For every action there is an equal and opposite reaction.”

In any economy, nothing works in isolation. For every dollar increase that occurs in one part of the economy, there is a dollars’ worth of reduction somewhere else.

President Trump should be implementing fiscal policy which would lead to stable oil prices at a level which supports healthy and robust economic activity.

Unfortunately, he isn’t.

By Real Investment Advice

More Top Reads From Oilprice.com:

The global economy wasn’t able to reconcile itself with the collapse of oil prices then because the main ingredients that make up the global economy, namely, global investments, the oil industry and the economies of the oil-producing countries have all been undermined.

While it is true that low oil prices could reduce the cost of manufacturing, thus helping the global economy to grow, it is a short-term benefit as this is vastly offset by a curtailment of global investment which forces companies around the world to cut spending, sell assets and make thousands, if not millions, of people redundant. There has been a loss of 1.50%-2.00% annually in global economic growth during the period of 2014-2016.

The seven major oil companies in the world – Royal Dutch Shell, BP, Exxon Mobil, Chevron, Total, ENI and Statoil lost more than a $1 trillion in revenues and lower market value and cancelled more than $200 bn in oil & gas investments reducing their share of global oil production.

Moreover, global investment in upstream exploration from 2014 to 2020 is projected to be $1.8 trillion less than previously assumed, according to leading US consultants IHS.

The Arab Gulf oil producers alone lost an estimated $289 bn in oil revenues between 2014 and 2016 not to mention losses by other oil-producing nations including Russia and the United States.

A continuation of low oil prices leaves no winners only losers. It also demonstrates the destructive power of low oil prices.

The news that oil companies have lost an estimated $1 trillion since the oil began its latest slide over a 50-day period since October demonstrate the importance of high oil prices to the global economy.

I have always argued that a fair price for oil ranges from $100-$130 a barrel. Such a price is good for the global economy since it invigorates the three biggest chunks of the global economy, namely, global investments, the economies of the oil-producing nations and the global oil industry.

As for the United States, it is doubtful whether the steep decline in oil prices would provide a boost to the US economic recovery. And while the price decline would certainly provide the equivalent of a sizable tax cut for US consumers, it will deliver a major blow to the increasingly important US oil industry which is estimated to employ around 2% of the US workforce. It is also raising the risk of major defaults on the hundreds of billions in loans that have been extended to the domestic shale oil industry and the rising cost of servicing that debt.

The US economy will definitely be worse off with low oil prices. To prove the point, let us make a rough calculation. The United States imported 10 million barrels a day (mbd) in 2017 according to the 2018 BP Statistical Review of World Energy. Let us assume that it will import the same this year. A reduction of oil prices from say $80 a barrel to $60 now would have reduced US budget deficit by an annualized $73 bn in 2018. On the other hand, the reduction in price would have cost US shale oil producers $73 bn in losses being the difference between their breakeven price of $60 a barrel and an $80 dollar oil. This could be projected to lead also to a loss of production estimated between 1 -2 mbd valued at $29 bn–58 bn. When you add all these losses we come to an annualized total figure of $102-$131 bn against a reduction of budget deficit of $73 bn meaning that the United States will end up worse off by $29 bn-$58 bn. However, if you add also the cost of lost jobs to the equation and the rising debts of the US shale industry, we end up with a much higher figure.

President Trump is absolutely wrong to say that lower oil prices are like big tax cut for America and the World.

Dr Mamdouh G Salameh

International Oil Economist

Visiting Professor of Energy Economics at ESCP Europe Business School, London

I also believe that I read an article claiming that each cent a gallon of gas fall per year, provides a 1 billion dollar injection for the economy.

I believe your premise is based on a fixed oil supply. Instead, we are seeing an increase in supply that is growing faster than the growth in demand. So, your crude indicator is probably not applicable. Also, the reason consumption is growing more slowly is due to efficiencies rather than lack of activity. Again, looking at my personal economy, the electric bill is 30% lower. I'm not sitting in the dark, I am using LEDs. My refrigerator, dryer, boiler, and automobiles consume less energy. Less people are competing for fossil fuels as solar, wind, and other alternatives begin to have a meaningful impact.

Your speculation about US jobs may also be imprecise as consumption is being transferred from imported to domestic production.

I believe lower energy prices are a paradigm shift not an indicator of economic activity. You may consider the incremental savings 'crumbs', but people on fixed incomes are very sensitive to price changes. I am amazed that President Trump has been able to improve the economy while keeping inflation at bay. Enjoy the ride!

Thus, low oil prices are good for the economy, and the world.

This statement is true. No oil price manipulation propaganda, just plain economic truth.

Capitalism works. It drives prices down. Trump's motivations are complicated and he's undoubtedly monkeying around with industrial policy in very counterproductive ways, but high oil prices don't benefit many other than producers. Since extractive industries aren't tyoically subject to strong productivity increases they aren't good candidates for carrying the economy.

Gain to US consumer = 2*20 = US$40

Loss to US producer = -20

Loss to Saudi producer = -20 (or any other OPEC producer).

Thus there is a net gain to the economy of US$20.

However, also agree that employment et al in Crude Oil producing states such as Texas may be impacted by much lower Crude prices. The emerging shale boom, which is helping US reduce dependence on imported Crude Oil, will be impacted.

Guess US$50 (+-10%) WTI is as good a price for stability on both sides. Dallas Fed data indicates Shale producers make decent returns at this level of Crude oil pricing.

If gas goes to 25 cents a gallon, there would be billions of dollars freed up for dining, entertainment, travel. The money is multiplied and would lead to an even larger boom.

In this simplistic model, the proof is obvious. Lower oil prices have a MUCH LARGER impact on domestic GDP than high oil prices. The rest of the above examples ignore the obvious. People spend money one way or the other.