The oil industry is more profitable than at any time in years, yet the industry could fail to supply enough oil to meet global demand in just a few years’ time.

A series of second quarter earnings reports over the past two weeks has revealed surging profits across the oil industry, with some companies posting earnings that are double or triple from a year earlier. But even though they are flush with cash, the industry has not returned to the profligate spending levels that were common prior to the 2014 market downturn.

Depending on one’s perspective, that could be a good thing or a bad thing. According to Carbon Tracker, the oil industry has trillions of dollars of projects in the pipeline that will become financial risks as governments around the world seek to address climate change. In essence, lots of oil and gas reserves will remain in the ground due to forthcoming taxes, regulation or simply demand destruction as alternatives take hold. Against this backdrop, a shortfall in spending is not such a bad thing.

On the other hand, energy agencies and forecasters, such as the International Energy Agency, have warned that the current pace of spending by the global oil industry is insufficient.

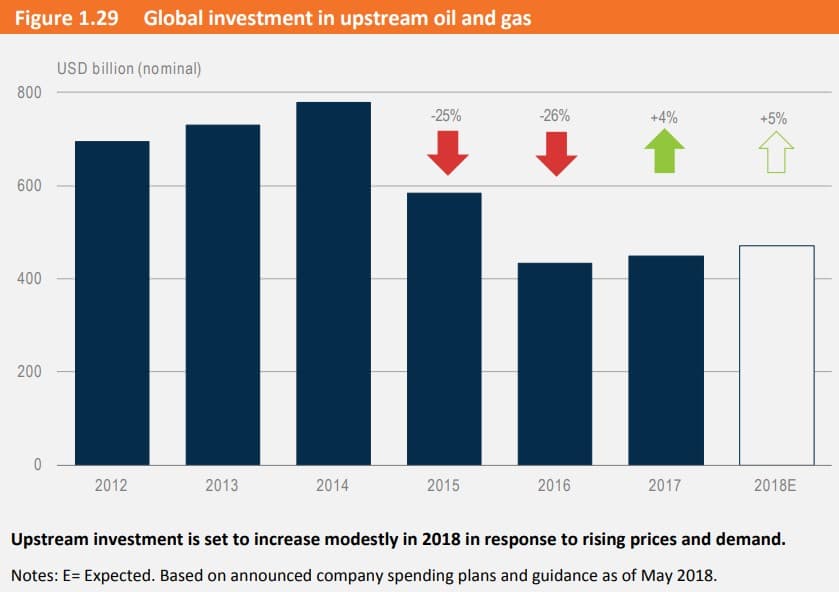

The downturn that began in 2014 led to a severe cutback in spending on exploration and development. Spending plunged by 25 percent in 2015, followed by another 26 percent decline in 2016. Since then upstream expenditures have bottomed out, rebounding 4 percent last year. The industry is only track to increase spending by another modest 5 percent in 2018. But there is little sign that the industry will return to spending at the same rate that it did prior to the downturn.

(Click to enlarge)

Related: The Most Important Waterway In The Oil World

Lower spending has translated into a steep drop off in new discoveries. In 2014, the industry discovered an average of about 1,350 million barrels of oil equivalent (mboe) every month. In 2015, that average ticked up to 1,404 mboe per month, according to Rystad Energy. But that figure fell off of a cliff in 2016, crashing to just 697 mboe/month, and fell again to 625 mboe/month last year.

New discoveries are set to rebound to 826 mboe/month in 2018 as drilling activity rebounds, Rystad Energy says, up 30 percent compared to last year. ExxonMobil’s three discoveries in Guyana represent a big slice of that total.

But the discoveries are still a fraction of what they used to be, back when the oil industry was spending much more. According to Rystad Energy, the oil industry needs to add around 33 billion barrels of oil every year, but the industry is on track to only add 20 billion barrels in 2018.

“An uptick of 30% from the abnormally low levels in 2017 might seem encouraging, but E&P players are currently facing a low reserve replacement ratio, on average of less than 10%. This is worrisome considering the impact on global oil supply in long term,” Espen Erlingsen, Head of Upstream Research at Rystad Energy, said in a statement.

As that pipeline begins to dry up over the next few years, a supply gap could emerge. “The years of underinvestment are setting the scene for a supply crunch,” Virendra Chauhan, an oil industry analyst at consultancy Energy Aspects, told the Wall Street Journal.

Related: The Three Best Oil Majors Of 2018

Of particular concern is the rate of depletion at conventional fields. “After more than three years of E&P underinvestment, the international production base has started to show accelerating signs of weakness with noticeable year-over-year production declines in 15 of the world's producing countries,” Schlumberger CEO Paal Kibsgaard told analysts on an earnings call. “These developments underline the growing need for increased E&P spending in particular in the international markets as it is becoming apparent that the new projects coming online over the next few years will likely not be sufficient to meet the increasing demand.” The average decline rate climbed from 3 percent in 2014 to 6.3 percent in 2016, although it improved to 5.7 percent in 2017.

U.S. shale production is expected to slow over the next year, but then accelerate once again after several Permian pipelines come online in late 2019 and early 2020. The Permian will be one of the largest sources of supply growth in the medium-term. But most analysts expect shale output to plateau in the 2020s before entering decline. The lack of new large-scale projects scheduled to come online in the early 2020s raises the risk of a supply crunch.

On the other hand, with peak demand looming, maybe it won’t be a problem after all?

By Nick Cunningham of Oilprice.com

More Top Reads From Oilprice.com:

- The Oil And Gas Boom Sends U.S. GDP Soaring

- Coke, Meth And Booze: The Flip Side Of The Permian Oil Boom

- $40 Billion LNG Project Finally Starts Up

By 2020, 15 million barrels a day (mbd) of new oil supply may be needed to meet a projected annual average rise in global oil demand of 1.59 mbd and also offset an annual natural depletion rate in global oil production estimated by the IEA at 5% or 4.8 mbd, virtually equivalent to losing the current output of Iraq.

A major underpinning factor for the projected steep rise in oil and gas demand is the growing world population and the emergence of megacities. Twenty-five years ago there were only 10 urban areas in the world that could boast more than 10 million inhabitants. Now there are more than 37 so-called “megacities” worldwide. By 2040 the United Nations estimates that nearly 65% of the world’s population will call cities home.

According to the IEA, the world needs $44 trillion in investment in global energy supply between now and 2040 to meet the coming global energy needs. A lack of investment will cause oil production to decline steeply and 80% of the current new oil supply is needed to offset natural declines.

The oil industry desperately needs new sources of oil, and they need new investors

and technologies to find those sources quickly.

Dr Mamdouh G Salameh

International Oil Economist

Visiting Professor of Energy Economics at ESCP Europe Business School, London