Friday July 13, 2018

In the latest edition of the Numbers Report, we’ll take a look at some of the most interesting figures put out this week in the energy sector. Each week we’ll dig into some data and provide a bit of explanation on what drives the numbers.

Let’s take a look.

1. Automation hits oil and gas industry

(Click to enlarge)

- Automation and robotics are eliminating jobs in the oil and gas sector. Oil drillers are producing more oil than ever before, but they no longer need legions of workers to do so.

- Output has climbed to 10.9 mb/d recently, but employment is 21 percent lower than it was in 2014, according to the Wall Street Journal.

- Despite the oil boom and the drilling frenzy, the jobs are not coming back in the same way.

- Devon Energy (NYSE: DVN), for instance, has trimmed its workforce to 3,100, down from 5,500 in late 2014. Drilling and construction costs are down by 40 percent over that timeframe, while initial production rates are up by some 450 percent.

- Trucking is the one sector that is sorely hurting from a shortage of workers. Truckers can still receive six-digit salaries.

- Ironically, one oft-cited solution to the pipeline bottleneck in the Permian is trucking oil to the Gulf Coast, but the nationwide trucking shortage makes that unlikely.

2. Lack of pipeline capacity or too many pipelines?

(Click to enlarge)

- Matching midstream capacity to upstream supply is a…

Friday July 13, 2018

In the latest edition of the Numbers Report, we’ll take a look at some of the most interesting figures put out this week in the energy sector. Each week we’ll dig into some data and provide a bit of explanation on what drives the numbers.

Let’s take a look.

1. Automation hits oil and gas industry

(Click to enlarge)

- Automation and robotics are eliminating jobs in the oil and gas sector. Oil drillers are producing more oil than ever before, but they no longer need legions of workers to do so.

- Output has climbed to 10.9 mb/d recently, but employment is 21 percent lower than it was in 2014, according to the Wall Street Journal.

- Despite the oil boom and the drilling frenzy, the jobs are not coming back in the same way.

- Devon Energy (NYSE: DVN), for instance, has trimmed its workforce to 3,100, down from 5,500 in late 2014. Drilling and construction costs are down by 40 percent over that timeframe, while initial production rates are up by some 450 percent.

- Trucking is the one sector that is sorely hurting from a shortage of workers. Truckers can still receive six-digit salaries.

- Ironically, one oft-cited solution to the pipeline bottleneck in the Permian is trucking oil to the Gulf Coast, but the nationwide trucking shortage makes that unlikely.

2. Lack of pipeline capacity or too many pipelines?

(Click to enlarge)

- Matching midstream capacity to upstream supply is a tricky business. Pipelines take time to build, and when they come online they provide a huge increase of capacity in lump fashion.

- The Permian is suffering from a lack of pipeline capacity, which is worsening by the day. Bloomberg New Energy Finance puts current capacity at 2.9 million barrels per day. The backlog of drilled but uncompleted wells is growing fast as drillers hold off on completions.

- A series of projects are set to come online next year, adding another 2 mb/d of pipeline capacity.

- But at that point, there could be too much pipeline space. Shale drillers will only fill up those lines two years later.

3. Saudi inventories dwindle

(Click to enlarge)

- At the start of 2017, when Saudi Arabia was trying to rebalance the oil market and engineer an increase in prices, it deliberately curtailed exports to the U.S. by hiking the price for its oil. Why?

- EIA data is some of the most closely-watched and most transparent data in the world, so a decline in inventories in the U.S., as reported by the EIA, would impact market psychology.

- Now that Saudi Arabia wants to cool the market, the Kingdom could flip that old strategy on its head.

- By drawing down Saudi inventories and flooding the U.S. with oil, Liam Denning of Bloomberg argues, Saudi Arabia could create the perception of ample supply. As that oil starts showing up in EIA data as an increase in inventories, market jitters about a supply shortage would fade.

- Saudi oil shipments to the U.S. are up sharply, rising to 800,000 bpd, up from 700,000 bpd in the first quarter.

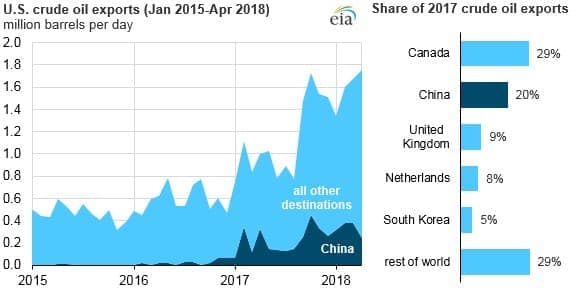

4. U.S.-China trade war could hit crude trade

(Click to enlarge)

- China has emerged as a key buyer of U.S. crude oil, accounting for a fifth of total U.S. oil exports in 2017.

- That was enough to make China the second largest buyer of American crude after Canada.

- The escalating trade war between the two countries could impact the crude flows, however. The U.S. imposed $34 billion worth of tariffs on China last week, and China quickly retaliated. The Trump administration is considering a further $200 billion in tariffs. China won’t be able to match that number but would surely respond.

- China is poised to put a 25 percent tariff on U.S. oil imports, which would force U.S. producers to send their crude elsewhere, perhaps at a lower price.

- The situation starts to get complex because the U.S. also wants China to stop buying oil from Iran.

- Chinese refiners are facing a conundrum: tariffs on U.S. oil, demands to stop buying Iranian oil, and lower shipments from Venezuela because of ongoing declines.

- Something will have to give. In that sense, the trade war puts more pressure on China to ignore U.S. sanctions on Iran.

5. Oil demand growth slows

(Click to enlarge)

- Higher oil prices are starting to put a strain on demand growth. In the first quarter demand grew at a 2-mb/d rate, year-on-year.

- That slowed in the second quarter to just 0.9 mb/d.

- For the full-year, the IEA expects demand to expand by 1.4 mb/d.

- The agency said that higher prices are “starting to take a toll.”

- “Several countries are also feeling the pain of higher oil prices, particularly so when combined with currency depreciation versus the US dollar,” the IEA said in a report this week.

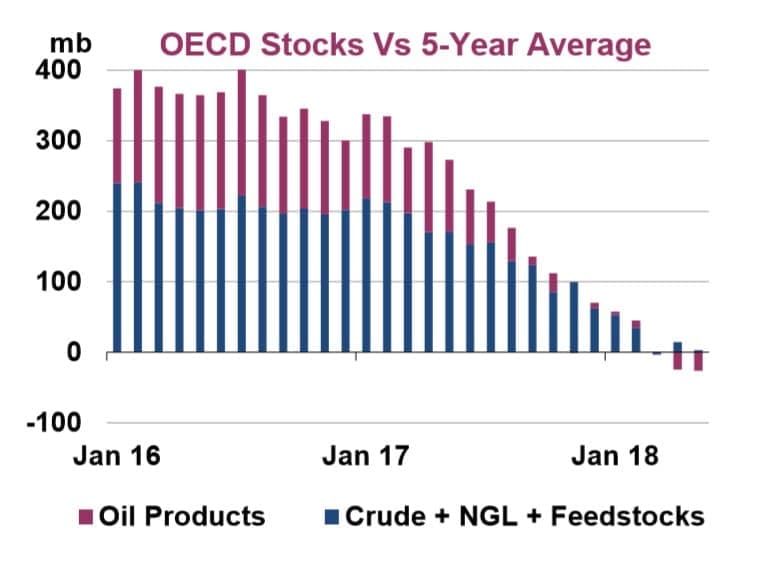

6. Stocks below five-year average

(Click to enlarge)

- OECD stocks rose in June by 13.9 million barrels, hitting 2,840 million barrels. The increase, however, was only half as much as is typical for this time of year.

- OECD inventories are still 23 million barrels below the five-year average.

- Crude stocks gained a negligible 1.3 million barrels, but refined product stocks rose by 14.5 million barrels.

- Digging deeper, the U.S. saw a very strong 18.4 million-barrel decline. Refineries stepped up processing and exports were also elevated.

- Preliminary data from the IEA indicates a decline in OECD inventories in June.

7. U.S. gasoline demand cools

(Click to enlarge)

- U.S. oil demand rose by 0.38 mb/d in April (the latest month for which data is available), a year-on-year increase of 1.9 percent.

- But gasoline demand fell by 71,000 bpd in April, compared to the same month in 2017. The decrease is likely the result of fewer vehicle miles traveled, which, in turn, is probably the result of higher gasoline prices. Average retail gas prices were 40 cents per gallon higher in April compared to a year earlier.

- Preliminary data suggests U.S. crude oil demand continued to rise in May and June, on the back of heavy petrochemical demand, even as gasoline consumption remained tepid.

- In fact, 2018 could mark the first year since 2012 in which annual gasoline demand declines.

- The EIA projects gasoline demand to fall ever-so-slightly this year, dipping by 10,000 bpd compared to 2017 levels.

- The last annual decrease took place in 2012, when oil prices routinely topped $100 per barrel.

That’s it for this week’s Numbers Report. Thanks for reading, and we’ll see you next week.