The most prevalent view regarding future oil supply, as well as total energy supply, seems to be fairly closely related to that expressed by Peak Oilers. Future fossil fuel supply is assumed to be determined by the resources in the ground and the technology available for extraction. Prices are assumed to rise as fossil fuels are depleted, allowing more expensive technology for extraction. Substitutes are assumed to become possible, as costs rise.

Those with the most optimistic views about the amount of resources in the ground become especially concerned about climate change. The view seems to be that it is up to humans to decide how much energy resources we will use. We can easily cut back, if we want to.

The problem with this approach is the world economy is much more interconnected than most analysts have ever understood. It is also much more dependent on growing energy supply than most have understood. Surprisingly, we humans aren’t really in charge; the laws of physics ultimately determine what happens.

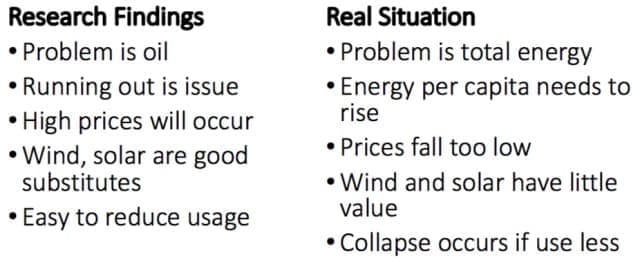

In my view, Peak Oilers were correct about energy supplies eventually becoming a problem. What they were wrong about is the way the problem can be expected to play out. Major differences between my view and the standard view are summarized on Figure 1.

(Click to enlarge)

Figure 1. Prepared by Author.

Let me explain some of the issues involved.

[1] Modeling is a lot more difficult than it looks.

Let’s take one common model of the part of the earth where we live, a street map:

(Click to enlarge)

Figure 2. Source: Edrawsoft.com

If we want to scale the model up to cover the whole world, we need to add a whole new dimension. In other words, we need to make a globe.

The same problem occurs with what seem to be simple economic models, like supply and demand:

(Click to enlarge)

Figure 3. From Wikipedia: The price P of a product is determined by a balance between production at each price (supply S) and the desires of those with purchasing power at each price (demand D). The diagram shows a positive shift in demand from D1 to D2, resulting in an increase in price (P) and quantity sold (Q) of the product.

If we are trying to model the situation a long way from limits (running out, or whatever the real limit is) then this model is perhaps “good enough.”

But if energy is the item that is in scarce supply as we approach limits, it can affect both quantity and price. Lack of energy supply at an inexpensive enough price can reduce both the quantity of the goods produced and the wages of workers. For example, distributors of goods in the United States may choose to buy imported goods from China or India to work around the problem of too high a cost of production (including energy costs).

The resulting competition with low-wage countries reduces the wages of many workers, especially those with low skill levels and those just finishing their educations. With such low wages, workers cannot afford to buy as many cars, motorcycles, and other goods that use energy products. The lack of demand from these workers indirectly brings down the prices of commodities of all kinds, including oil. In fact, prices can fall below the cost of production for extended periods. This has happened since 2014 for many energy products, including oil.

The model by the economists isn’t right. It doesn’t have enough dimensions to it. Peak Oil researchers did not understand that economists had put together a badly incomplete model. Their model only represents simple cases away from energy limits. Their model doesn’t explain what we should expect near energy limits.

[2] Simple two-dimensional models can work for some purposes, but not for others.

One thing that has been confusing to Peak Oil researchers is the base model in the 1972 book The Limits to Growth seems to present a fairly accurate timeline regarding when energy limits might hit. The indications are that the limits will happen about now.

The model reflects a simple, quantity-based approach that does not consider problems such as how debt might be repaid with interest if the economy is shrinking, or how pension payments would fare in a shrinking economy. The model is based on the assumption that our problem is only inadequate supply, not economic problems that indirectly result from short supply.

(Click to enlarge)

Figure 4. Base scenario from 1972 Limits to Growth, printed using today’s graphics by Charles Hall and John Day in “Revisiting Limits to Growth After Peak Oil” http://www.esf.edu/efb/hall/2009-05Hall0327.pdf

The thing that is easy to miss is the fact that this model is too simple to show how the limits will hit. For example, will the limits apply to oil or all fuels combined? What will be the impact on wage disparity? How will the impact on wage disparity affect demand for goods and services? Will the economy start growing too slowly and fail for that reason?

Related: Houthi Missile Hits Saudi Oil Tanker

The authors of The Limits to Growth wisely pointed out that their models could not be relied on to show what would happen after collapse, but this warning seems to have been missed by many readers. I have suggested that it might have been better if the model had been truncated at an earlier date, to emphasize how limited the model’s predictive abilities really are because of its omission of a financial system that includes debt, wages, and prices.

(Click to enlarge)

Figure 5. Limits to Growth forecast, truncated shortly after production turns down, since modeled amounts are unreliable after that date.

[3] Energy is a critical need for the economy. Many prior economies collapsed when energy consumption stopped rising sufficiently rapidly.

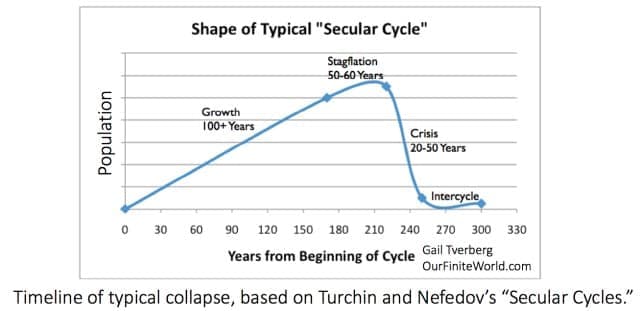

Much research has been done on the huge number of historical economies that have collapsed. Peter Turchin and Sergey Nefedov examined eight agricultural economies that collapsed. This is a chart I prepared, explaining the approximate timing of the eight collapses, and the population growth pattern that seemed to occur.

(Click to enlarge)

Figure 6. Chart by author based on Turchin and Nefedov’s Secular Cycles.

According to Turchin and Nefedov, when a new resource became available (for example, land available after cutting down trees, or a new discovery of improved food yields because of irrigation), the population grew rapidly until the population reached the carrying capacity of the land with the new resource. The carrying capacity would reflect the energy resources that were easily available: land for farming and biomass that could be harvested and burned.

As limits were reached, population growth tended to plateau. The plateau would tend to come when the area could only support its existing population, without adding some sort of complexity to try to produce more goods and services using the existing energy resources. Joseph Tainter, in The Collapse of Complex Societies, tells us that by adding complexity (including improved technology, larger businesses and expanded government functions), it was possible to increase the output of the economy over what initially seemed to be available. There are at least two reasons why using technology to work around natural limits doesn’t work for very long, however:

[a] There are diminishing returns to adding new technology. Eventually, it costs more to add technology than its benefit is worth.

[b] Growing technology is associated with growing wage disparity. New technology replaces some jobs. Some new jobs may be high paying (managers, highly trained technical people), but if growth in economic output is not sufficient, a disproportionate share of the jobs may be very low-paying. In fact, some former workers may be left without jobs because technology replaces earlier jobs.

History shows that there are many things that contribute to the collapse of economies:

[a] Governments cannot collect sufficient taxes, because as wage disparity grows, many workers are increasingly impoverished and can barely support themselves.

[b] The slow economic growth rate makes it difficult to repay debt with interest.

[c] Investments in new businesses don’t pay enough to make them worthwhile.

[d] The health of the marginalized lower-paid workers deteriorates, at least partly because of poorer nutrition. They tend to catch diseases more easily, and epidemics spread farther.

[e] Prices of essential goods may fall below the cost of production because of wage disparity among workers. The lower-paid workers cannot afford to buy very many goods and services. Because these workers cannot afford many goods and services, the price of commodities used in creating these goods and services falls.

[f] The economy has less resilience against chance variations, such as temporary variability in climate, or a neighbor that suddenly has a stronger army, if the economy is operating near its carrying capacity. A problem that might not have brought the economy down may bring it down, because of a lack of reserves to handle chance fluctuations.

[4] We get evidence of a need for rising energy consumption per capita by analyzing the ratio of US wages to GDP, and how it has fallen over the years.

(Click to enlarge)

Figure 7. US wages as a percentage of GDP (based on BEA data) compared to Brent oil price in $2016 dollars, based on BP Statistical Review of World Energy data.

If the only energy need of humans were food, we would expect human per capita energy consumption to be flat. The issue, however, is that humans are not living within normal food limits of the economy. Humans gained an initial advantage over other plants and animals over one million years ago, when they learned to burn biomass and use it for many purposes (cooking food to get more energy value, scaring away predators and catching prey, expanding the range of humans to colder climates).

Now, humans must maintain their earlier advantage over other species, or they will lose the contest to some predator, such as microbes. With today’s huge population, maintaining humans’ prior advantage requires a surprising amount of energy supplies, in addition to food energy.

Human labor represents only part of the economy. Figure 7 shows that wages as a percentage of GDP were fairly flat between 1940 and 1970, when oil prices were low, and oil was in abundant supply. The big drop in the ratio of wages to GDP started after 1970, when oil prices have been higher. To work around the problem of higher oil prices, the economy has become more complex: businesses and governments have grown; international trade has become more important; debt and the financial system have taken on a greater role.

If, over the long term, wages have been falling as a percentage of GDP, then the remainder of the economy is growing even faster. Government is growing. The size of businesses and the amount of technology used by those businesses, is increasing. All of these things need to be supported, indirectly, by energy products. For these reasons, energy consumption needs to grow faster than population, even if technology is making individual processes more efficient.

[5] Analysis of historical data since 1820 shows what happens when the world economy hits flat spots in per capita energy consumption.

(Click to enlarge)

Figure 8. World per Capita Energy Consumption with two circles relating to flat consumption. World Energy Consumption by Source, based on Vaclav Smil estimates from Energy Transitions: History, Requirements and Prospects (Appendix) together with BP Statistical Data for 1965 and subsequent, divided by population estimates by Angus Maddison.

The 1920-1940 Flat Period was definitely a period of “not enough energy to go around.” The Great Depression of the 1930s was a time of little GDP growth and great wage disparity. There is evidence that both World War I and World War II (coming immediately before and immediately after the 1920-1940 period) were, indirectly, energy wars.

The 1980-2000 Flat Period represents a time when the US and Europe both intentionally reduced their oil consumption because it was feared that oil would be in short supply in the future. This was a period that required huge debt growth to make the necessary changes (Figure 9).

(Click to enlarge)

Figure 9. Growth in US Wages vs. Growth in Non-Financial Debt. Wages from US Bureau of Economics “Wages and Salaries.” Non-Financial Debt is discontinued series from St. Louis Federal Reserve. (Note chart does not show a value for 2016.) Both sets of numbers have been adjusted for growth in US population and for growth in CPI Urban.As mentioned previously, it is also the period that a huge amount of complexity was added, and wages fell as a percentage of GDP. It is doubtful this pattern could be repeated again, without serious economic problems occurring

There were other problems in the 1980 to 2000 period. The collapse of the central government of the Soviet Union occurred in 1991. Low oil prices for several years prior to the collapse reduced the revenue of the Soviet Union. This seems to have been a major contributor to the collapse. Oil exporters are again encountering the issue of inadequate tax revenue, as a result of low oil prices since 2014.

[6] It is total energy growth (not simply oil consumption growth) that correlates well with GDP growth.

(Click to enlarge)

Figure 10. X-Y graph of world energy consumption (from BP Statistical Review of World Energy, 2017) versus world GDP in 2010 US$, from World Bank.

Peak Oil followers haven’t stopped to think through how the economy works. It is really the growth of total energy that we need to be concerned about, from the point of view of operating the economy.

[7] Indirectly, debt and asset prices are promises of future energy consumption.

We don’t think of debt as a promise of future energy consumption. The connection comes because debt can only be redeemed (through a financial transaction) for future goods and services. Making these future goods and services will require energy consumption.

The same principle applies to asset prices of all kinds: prices of shares of stock, home prices, land prices, and pension values. If an asset-owner wants to sell an asset and use the proceeds to buy other goods and services, the asset-owner encounters the same situation as the bond-owner: the goods and services that will be provided in exchange depend on the energy supplies available at the date of the exchange. Thus, indirectly, the prices represent promises of future energy consumption.

[8] One essential part of the economic growth system seems to be an ever-falling price of energy services, where energy services are defined as the cost of energy, plus whatever efficiency savings are available that make the cost of energy services less expensive.

For example, the cost of transporting a 100 kg. package 100 kilometers, or of heating a 100 square meter residence for a winter, must keep falling. If this happens, businesses can afford to buy ever more tools for their workers. With these tools, the workers can become ever more productive.

Furthermore, because of their growing productivity, workers find that their wages are rising, so that they can buy ever more goods and services. In this way, demand continues to rise. Changes such as these allow the economy to keep growing.

(Click to enlarge)

Figure 11. Energy services chart is by Roger Fouquet, from Divergences in Long Run Trends in the Prices of Energy and Energy Services. Second chart is figure from UNEP Global Material Flows and Resource Productivity.

In fact, the prices of energy services do seem to keep falling, even if the cost of providing these services is not falling. This is a major reason why energy prices seem to have fallen below the cost of production for practically every type of energy in recent years. This situation is not sustainable; it can be expected to lead to the collapse of the system.

[9] If the growth rate of the economy is not fast enough, the danger is that the economy will collapse.

We can think of the GDP situation as being similar to that of a bicycle. GDP needs to be rising rapidly enough, or the economy will collapse. A bicycle needs to be traveling fast enough, or it will fall over. Economists often talk about an economy slowing to stall speed.

(Click to enlarge)

Figure 12. Author’s view of analogies of speeding upright bicycle to speeding economy.

Reported world GDP growth rates in recent years are likely somewhat overstated for several reasons.

- World GDP represents a weighting of country reported GDP. One approach to weighting gives disproportionate influence to China, India, and other developing countries.

- The use of Quantitative Easing and of higher government debt temporarily inflates the quantity of goods and services an economy can make.

- Artificially low energy prices give a boost to oil importing counties. They also keep the prices of goods and services artificially low, compared to wages. These artificially low energy prices cannot continue without the failure of governments of oil exporters, and without businesses producing energy products collapsing.

Whether or not the economy can continue operating is determined by the economy itself, because the economy is a self-organized system. Its continued operation doesn’t depend on published statistics of varying quality.

[10] Researchers studying oil limits thought that they had found a whole new phenomenon, “Peak Oil.”

In fact, they had found a special case of a phenomenon that tends to lead to collapse, namely, conditions that lead to energy consumption per capita that is not rising rapidly enough. Such conditions can occur in many different ways, such as these:

[a] Population rises sufficiently that it is hard to keep energy consumption per capita rising. This seems to be a major problem in many historical collapses.

[b] Collapse indirectly comes from diminishing returns in energy extraction. The standard workaround for diminishing returns is growing use of complexity (including technology). This tends to encourage the non-wage portions of the economy to grow, as in Figure 7. Adding complexity becomes increasingly expensive for the benefit obtained. Ultimately, wage disparity and falling commodity prices become a problem, and the system collapses.

[c] Random fluctuations in climate occur. An economy collapses because it doesn’t have the strength to respond to such random fluctuations.

[11] Peak oil researchers did the best they could, with the limited understanding of the day. The unfortunate problem was that the model they put together wasn’t really correct.

The fundamental problem of the Peak Oil researchers was that the economic researchers, upon whom they depended, did not really understand the interconnected nature of the economy. They continued to use two-dimensional economic models, when they needed multidimensional models. Economists predicted that prices would rise near limits, when it is increasingly clear that this cannot be true. The world has been struggling with low prices for many commodities since 2014. Prices now are temporarily less low, but they still are not high enough to allow adequate tax revenue for oil exporting countries.

The Energy Return on Energy Invested (EROEI) Model of Prof. Charles Hall depended on the thinking of the day: it was the energy consumption that was easy to count that mattered. If a person could discover which energy products had the smallest amount of easily counted energy products as inputs, this would provide an estimate of the efficiency of an energy type, in some sense. Perhaps a transition could be made to more efficient types of energy, so that fossil fuels, which seemed to be in short supply, could be conserved.

The catch is that it is total energy consumption that matters, not easily counted energy consumption. In a networked economy, there is a huge amount of energy consumption that cannot easily be counted: the energy consumption to build and operate schools, roads, health care systems, and governments; the energy consumption required to maintain a system that repays debt with interest; the energy consumption that allows governments to collect significant taxes on exported oil and other goods. The standard EROEI method assumes the energy cost of each of these is zero. Typically, wages of workers are not considered either.

There is also a problem in counting different types of energy inputs and outputs. Our economic system assigns different dollar values to different qualities of energy; the EROEI method basically assigns only ones and zeros. In the EROEI method, certain categories that are hard to count are zeroed out completely. The ones that can be counted are counted as equal, regardless of quality. For example, intermittent electricity is treated as equivalent to high quality, dispatchable electricity.

The EROEI model looked like it would be helpful at the time it was created. Clearly, if one oil well uses considerably more energy inputs than a nearby oil well, it would be a higher-cost well. So, the model seemed to distinguish energy types that were higher cost, because of resource usage, especially for very similar energy types.

Another benefit of the EROEI method was that if the problem were running out of fossil fuels, the model would allow the system to optimize the use of the limited fossil fuels that seemed to be available, based on the energy types with highest EROEIs. This would seem to make best use of the fossil fuel supply available.

[12] There are corrections to the EROEI method that might allow it to work in the manner that it should. The catch is that these corrections seem to show wind and solar not to be solutions to our problems. In fact, the system is so integrated, and our need for rising energy consumption per capita so great, that it is doubtful that any substitute for fossil fuels can really be solution.

Professor Hall observed that if a fish had to swim too far to get food, it could not use very much of the food’s energy to catch the food, because most of its energy was needed for everyday metabolism and reproduction. A fish would typically need an EROEI of at least 10:1 for catching its prey, if it expected to have enough energy left to cover its full metabolic needs (including reproduction), plus the energy required to catch its prey.

If catching some prey only provided an energy return of 1:1, it would be pretty much worthless as a food source, since it would not cover any of the metabolic costs. Certainly, it would not make sense to call any energy in excess of an EROEI of 1:1 “net energy,” because it makes no contribution to covering a fish’s metabolic or reproduction activities. “Net energy” should only come from food sources with an EROEI very close to, or above, a ratio of 10:1.

A similar approach can be used to incorporate the large amount of energy that is lost by zeroing out the equivalent of the metabolism of the fish, for the economy. Based on Figure 11, the required average EROEI (to match what the economy can afford to pay for) needs to rise over time. Thus, if the required average EROEI is 10:1 now, it might be 11:1 later, simply because the increasingly complex world economy needs energy services that are becoming ever less expensive.

The story, “Higher energy prices will work in the future” is simply a myth, created by economists who do not understand how the economy really operates, considering all of the feedbacks involved. In inflation-adjusted terms, the price of energy services needs to keep falling as a percentage of GDP, to keep the system operating.

To fix the net energy calculation, some suitable minimum EROEI ratio for the economy needs to be determined–probably about 10:1–to incorporate the large share of energy consumption that is missing from the economy. Net energy would be then determined as the energy in excess of 10:1 EROEI, rather than in excess of 1:1 EROEI. This approach would make solar and wind look much less beneficial than most calculations to date.

In the case of intermittent renewables, a determination needs to be made whether the role of wind or solar in a particular situation is to replace electricity or fuel. If the role is to replace electricity (as is generally the case), then sufficient buffering must be provided in the model, so that the model can calculate the proper EROEI for dispatchable electricity (not intermittent electricity). Adding buffering will generally substantially reduce the EROEIs of intermittent electricity types. This adjustment makes it clear that there is much less benefit of wind and solar.

If the purpose of the intermittent electricity is only to replace fuel (such as a proposed new Saudi solar installation), then there is no need for buffering in the calculation. Of course, a cost comparison could also be used, and this might be the simpler approach. The cost comparison will generally be favorable if the fuel being replaced is oil, because oil is a high-priced fuel.

Related: Escalating Trade War Ups Pressure On Oil Prices

Too often, wind or solar is added to the system in a way that overlooks the real cost of buffering. Coal and nuclear electricity production find themselves with the unpaid job of providing buffering services for wind and solar. The net impact of adding intermittent renewables is that they push necessary backup power out of business. We end up with an electrical system that is worse off for adding intermittent renewables, even though this was not the intent of those requiring the use of such generation.

Conclusion

The number one need of the world economy is rising per capita energy consumption. In order to maintain economic growth, the price of energy services needs to fall as a percentage of GDP. The system will try to rebalance to the least expensive cost of energy production using globalization and other techniques. When this is no longer possible, the current world economic system is likely to fail.

Peak Oil modelers did not understand how complex our economy is. In their defense, no one else did either, especially back in the 1970 to 2005 era. They did the best they could, using the models that economists had put together. Because of the assumption of ever-rising energy prices, Peak Oil models assume that far more fossil fuels are extractable than is likely to really be the case. Optimists (oil companies, politicians, government agencies) assume even higher extraction of fossil fuels than is reasonable. The result is considerable concern about climate change.

When a person realizes how tightly integrated the world economy is, and its need to grow, it becomes clear that using less is not a solution. Prices of commodities would plunge even farther below the cost of production. The economic system would experience a far worse recession than the Great Recession of 2008-2009. Some governments would fail. The spiral might permanently be downward.

Standard solutions don’t work either. Substitutes don’t scale up quickly. Biomass cannot be used heavily because the world’s ecosystems depend on biomass; we are already using more than our share. Intermittent renewables such as wind and solar have their own high energy cost, but it is hard to count. They depend on international trade to make and repair the devices. They depend on debt for financing. They are really only part of the fossil fuel system, contrary to what the name “renewables” would suggest.

Energy modelers did their best. Unfortunately, with modeling it is hard to see what is going wrong. This is especially true when the academic world is divided into silos, each of which tends to look primarily at the writings of the people in its own field. It is easy for an incorrect model to get firmly embedded into people’s minds.

By Gail Tverberg via Our Finite World

More Top Reads From Oilprice.com:

- Saudi Officials Worried About Oil’s Future

- Oil Prices Bristle As U.S. Rig Count Climbs

- Is The Iran Nuclear Deal Coming To An End?

Only charts that matter are the ones that show that the price of renewables and storage are falling AND will continue to do so. And the potential of those sources are almost unlimited.

And all the fears about renewables/storage are shown to be baloney. AND in many ways they deliver better.

Only things that renewables can't deliver is "stuff" when needed. Can't make tires out of solar...

Besides that their is a great fossil free life coming.

How do we mine the rare earth materials to manufacture the solar panels or wind mills with just reneweables? Not to mention delivery and setup to the scale needed to replace fossil fuel generation, including storage, etc globally. We needed cheap energy to get to where we are now. Wind/solar are only cheap if you neglect the cost of the whole process that brings them online as well as maintenance. Can not do the scale you are hoping without cheap liquid fuels like oil and its derivatives. The same goes for all the batteries needed.