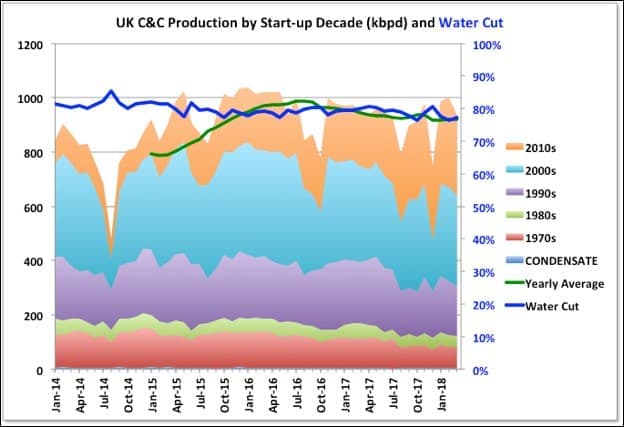

UK C&C

It was expected by many, me included but more importantly UKOGA and a couple of the bigger oil and gas consultancies, that UK offshore oil production would increase significantly from 2017 to exceed 1000 kbpd for the yearly average in 2018. So far this is proving a bit of a challenge. March production was 934 kbpd, down 7 percent m-o-m and 2 percent y-o-y (but up 0.8 percent for the first quarter compared with 2017). It’s possible that some fields have not reported but those showing zero for the month are not big producers. The biggest single field drop came from Clair but most field saw declines, even the newer ones. Jodi data indicates there will be a rise in May, but not above 1000 kbpd, and after that there is usually a summer dip because of maintenance shutdowns (plus this year some strikes at Total platforms).

(Click to enlarge)

Two of the largest oil producers, Buzzard and the Golden Eagle Area Development, both operated by Nexen, have started accelerated decline following increasing water breakthrough (especially noticeable in GEAD over the past year). The newest large field is Scheihallion. This is a redevelopment with its neighbouring field, Loyal, through the Glen Lyon FPSO (also called the Quad 204 project), which was started last year. So far the combined decline in Buzzard and GEAD has exceeded growth in Scheihallion.

The Clair Ridge platforms, which also exploit the heavy oil in the Clair field, were installed last year but there have been multiple delays and production is not now expected until later this year. Once it is ramped up, which could take three or four years despite it having some predrilled wells, it will be the largest producer at 100 to 120 mmbpd and has an eight-year plateau, while Scheihallion/Loyal will plateau and decline quickly.

(Click to enlarge)

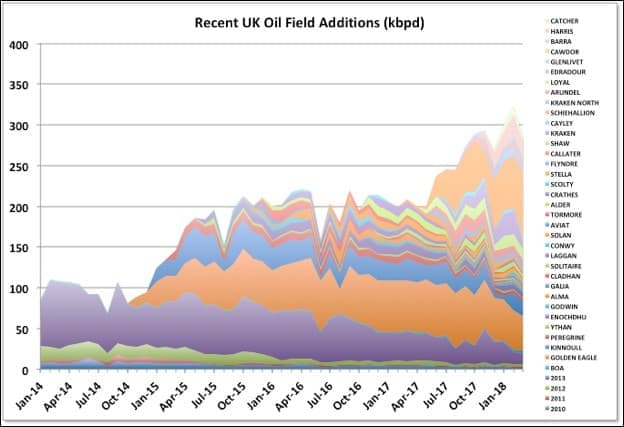

Pierce and Captain are heavy oil developments. Pierce was redeveloped in 2009 and Captain has recently switched to using polymer injection to improve the water flood performance. Heavy oil projects require many wells, tend to produce high water cuts from the outset and have low recovery factors. Clair and Clair ridge are mentioned above. Kraken was a heavy oil start-up in June last year, it has the largest water processing capacity in the UK North Sea and has already seen water at 60 to 65 percent. Mariner is another due to start later this year for Statoil, it uses condensate for EOR, and there are other heavy oil prospects like Bressay (cancelled by Statoil when the oil price collapsed) and Bentley.

(Click to enlarge)

Another reason for the possibly lower than expected total production is early decline in many of the smaller producers started up from late 2015 through 2017. For example the P10 production plan for Scolty & Crathes had over 7,000 bpd average in 2018 and a decline out to 2032, but the current production is around 3,000 bpd and declining, all from Crathes as the Scolty field expired after about four months. Similarly, Solan was predicted to average around 18,000 bpd in 2017 but achieved 10,000 bpd only briefly and is now below 5,000 and declining.

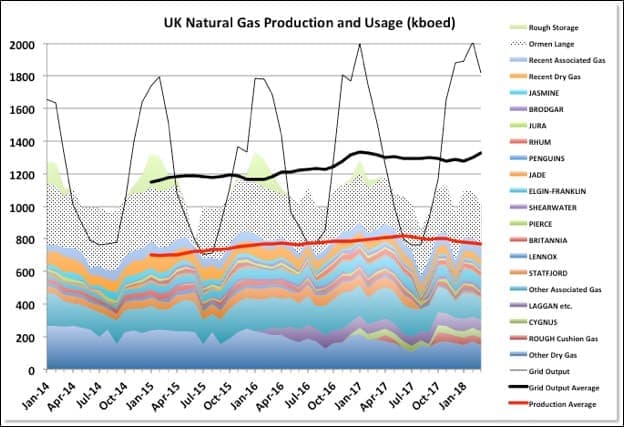

UK NATURAL GAS

(Click to enlarge)

UK Natural Gas production is in decline, probably terminal, while usage continues to grow. The biggest single supplier is the Ormen-Lange field in Norway, which is also in decline but it well be augmented by newer Norwegian developments like Aasta Hansteen and Dvalin that are due in the next few years and will deliver to the same gas plant at Nyhamna as Ormen Lange and then export via the Langeled pipeline to the UK.

(Grid data is from DUKES – Digest of UK Energy Statistics).

SHETLAND GAS PLANT

The Shetland Gas Plant (SGP) in Sullom Voe is a Total operated facility, receiving production from gas-condensate fields West of Shetland, and was one of the largest recent North Sea projects. I think there is enough evidence now to declare this project to be something less than a rip-roaring success. I don’t know if they will make money on it but the construction phase had a lot of problems (Petrofac took it on as a lump sum contract and lost money through various different issues) and the reservoirs look much poorer than expected, with the main ones of Laggan and Tormore only containing about a third of the expected reserves.

Related: Oil Selloff Gives Trump More Room On Iran

The green dots in the chart show the originally planned production for these two, with them coming of plateau to be replaced by Glenlivet and Edradour about now. In fact the original fields are approaching exhaustion and the smaller additions are now declining after being brought on-line early. The gas plant has recently been in turn around and some work may have been done to improve well delivery. (Note I think I’ve got the correct data shown now after messing up the Edradour numbers in two different ways previously.)

(Click to enlarge)

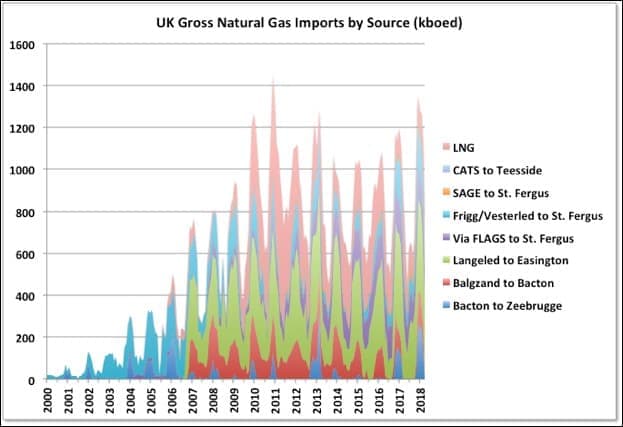

NATURAL GAS IMPORTS

(Click to enlarge)

The chart shows gross imports, net numbers are slightly less as there is some balancing through the Bacton interconnectors. Imports have been fairly steady since 2010, mainly because newer production in the North Sea balanced decline in mature fields (some of the new gas production is actually the final blow down of gas caps on mature oil fields). Imports are likely to need to increase now as overall production decline is accelerating again and demand appears to be increasing. Most new gas is likely to have to come from LNG.

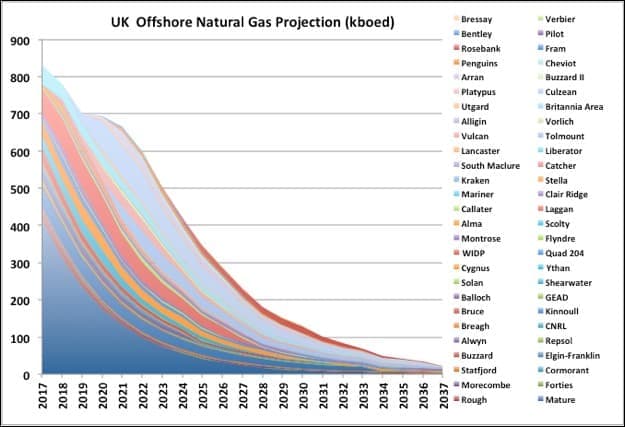

UK PRODUCTION PROJECTIONS

Previously I’d made an estimate of future production based on simple, assumed decline curves and overall reserves. The steepness of the curves, especially for natural gas, was striking so I have tried to get some better data using Environmental Statements, which each project is required to submit to the UKOGA as part of the development approval process. These include expected production profiles and are usually available on the E&P company web sites. Some later prospects that are still in the planning stages I’ve estimated based on available data from companies’ news releases and presentations. Overall the oil projection came out similar to before, but for natural gas it is slightly worse. The biggest unknown is the decline in small fields labelled “Mature” that I’ve approximated based on eyeballing recent performance and fitting overall reserves reported by UKOGA. Related: Goldman Predicts Major Solar Market Contraction

The production profiles presented in the applications are usually for P10 cases, so actual decline will be steeper than shown, for example this year’s drop off in Buzzard was actually not predicted until next year, even in their P50 case (which was presented as part of the Buzzard II development application), and if the new projects perform as well as Laggan or Scolty & Crathes then the decline will be very quick indeed.

(Click to enlarge)

(Click to enlarge)

I have included all known discoveries that look commercial with reasonable oil prices but have not included any allowance for future discoveries, though there aren’t many of those at the moment. Also not included are some larger discoveries that have not been fully appraised (e.g. Cambo, which is close to Rosebank and of similar size, Jackdaw, which is an ultra-high pressure / high temperature marginal gas field, and some other gas prospects in the West of Shetland area) plus several smaller discoveries that may be commercial at high prices or may need neighbouring discoveries to become so.

The UK oil industry is in its declining years and there is a fair number of mergers and acquisitions activity as the E&Ps seek to reduce costs. ConocoPhilips is swapping assets with BP and pulling back from the North Sea to concentrate on Alaska and LTO, Maersk Oil and Gas has sold up to Total which is now looking to offload a fair chunk of its assets, Chevron is looking to sell all its North Sea operating assets (but retain Rosebank as a development project), Repsol bought into some assets but it seems now it wants to get out again. With smaller players taking over there is sometimes a short-term production increase from mature fields, but it also tends to signify there are fewer large projects to come.

By Peak Oil Barrel

More Top Reads From Oilprice.com:

- Oil Investors Look To Utah For Long-Term Riches

- Wind Energy Is Getting Cheaper And Cheaper

- U.S. Bid To Ban Fuel Shipments To North Korea Fails