The rise of U.S. tight oil production over the last several years has upended the oil market and challenged OPEC’s hold on oil prices. This seemingly relentless growth in U.S. tight oil production has created the impression that oil prices will remain forever capped as each price spike is met by a massive wave of US tight oil supply.

Overview

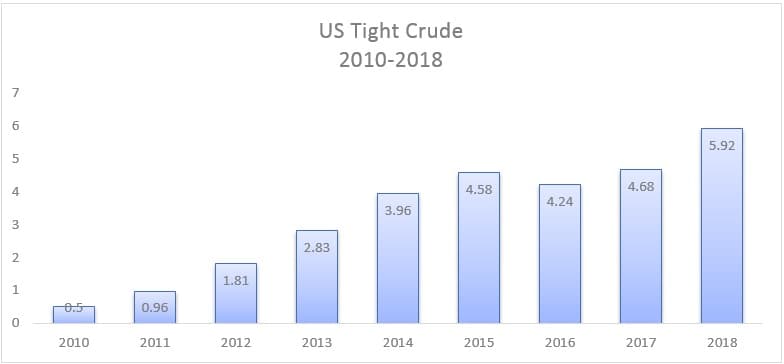

U.S. tight oil supply has grown from a mere 500K barrels in 2010 to just under 6M barrels in 2018. Following the oil crash of late 2014, U.S. tight oil growth experienced a brief pause in 2015-2016 before resuming its growth in 2017 and climbing to a new high by 2018. This latest growth spurt to a new record is even more impressive when we take in consideration the fact that WTI averaged $65 a barrel in 2018 as compared to $95 a barrel in the three years (2012-2014) preceding the oil crash.

(Click to enlarge)

(Source: OPEC WOO – 2018)

Most observers attribute this strong shale industry performance to technology and improved drilling and completion practices. We are told that American oil and gas companies have become more efficient. The widespread utilization of pad drilling, the introduction of longer laterals, pumping ever more sand per foot, closer and better well spacing, and smart fracture targeting are often mentioned as the driving factors behind the industry record beating performance. This narrative of technological prowess and innovation is an attractive one, but a deeper examination of the data reveals a different picture.

Analysis

This fallacious narrative of the U.S. tight oil industry overcoming the oil price crash of 2014 through innovation and better efficiency is the product of bundling various tight oil basins under one umbrella and the presentation of the resulting production data as a proof U.S. shale resiliency.

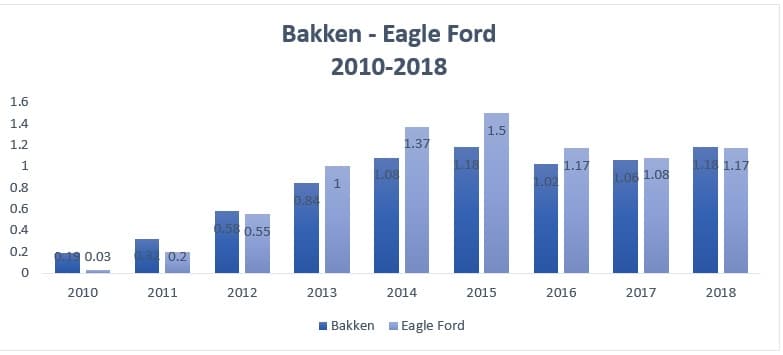

To properly understand the impact of the oil price crash of 2014 on U.S. tight oil production one must focus on shale basins with sufficient operating history prior to the oil price crash and examine their performance post the crash. To that end, the Bakken and the Eagle Ford are the perfect specimen. The Bakken and the Eagle Ford are the two oldest tight oil basins in the United States, with the former developed as early as 2007 and the latter in 2010. Examining the production performance of these two basins in the 4 years preceding the oil crash and contrasting it to the 4 years subsequent to it, offers important insight as to the resiliency of U.S. tight oil production in a low oil price environment. Related: Oil Jumps As Saudis Plan Further Production Cuts

(Click to enlarge)

(Source: OPEC WOO 2018)

Both the Bakken and the Eagle Ford grew at a phenomenal rate between 2010 and 2014. The Eagle Ford grew from practically nothing in 2010 to 1.3M barrels by 2014, while the Bakken grew five fold from 190K barrels to 1.08M barrels. Following the collapse in oil prices in late 2014, the Bakken and Eagle Ford growth continued for another year, albeit at a slower pace, as the pre-crash momentum carried production to new highs. However, by 2016, both the Bakken and the Eagle Ford went into a decline and have hardly recovered since. It took the Bakken three years to match its 2015 production level, meanwhile the Eagle Ford production remains 22% below its 2015 peak. During the pre-crash years these two fields grew by a combined yearly average of 600K to 700K barrels from 2012 to 2014. Post the oil price collapse, this torrid growth turned into a sizable decline by 2016 before stabilizing in 2017. Growth in both fields only resumed in 2018 at a combined yearly rate of 210K barrels, a 70% reduction from the combined fields pre-crash growth rate.

The dismal performance of these two fields over the last few years paints a different picture as to U.S. tight oil resiliency in a low oil price environment. The sizable declines, and muted production growth in both the Bakken and the Eagle Ford since 2014 discredit the leap in technology and the efficiency gains narrative that has been espoused as the underlying reason beyond the strong growth in U.S. oil production. As we expand our look into other tight oil basins, it becomes apparent that it was neither technology or efficiency that saved the U.S. tight oil industry, although these factors may have played a supporting role. In simple terms, the key reason as to the strength of U.S. production since the 2014 oil crash is better rock, or rather, the commercial exploitation of a higher quality shale resource, namely the Permian oil field.

(Click to enlarge)

(Source: OPEC WOO 2018)

The Permian oil field, unlike the Bakken and the Eagle Ford, was a relative latecomer to the U.S. tight oil story. It was only in 2013, only a year before the oil crash, that the industry commenced full scale development of that giant field’s shale resources. Prior to 2013, the Permian lagged both the Bakken and the Eagle Ford in total tight oil production and growth. As can be seen from the preceding graph, the oil crash had only a minor dampening effect on the Permian oil production growth. By 2017, Permian tight oil growth resumed at a healthy clip, and by 2018, Permian tight oil production growth shattered a new record with production skyrocketing by 860K barrels in a single year to 2.76M barrels. This timely unlocking and exploitation of the Permian oil basin masked to a large degree the devastation endured by the Bakken and the Eagle Ford post 2014. In essence, the U.S. tight oil story has two phases masquerading as one: the pre-2014 period marked by the birth and rise of the Bakken and Eagle Ford, and the post-2014 period, marked by the rise of the Permian. To speak of the U.S. tight oil industry as one is to mistake a long-distance relay race for the accomplishment of a single runner. Related: Which Oil Giant Generates The Most Cash?

The performance divergence between the Bakken, Eagle Ford, and the Permian has major implications as to the likelihood of U.S. tight oil production suppressing oil price over the medium and long term. A close examination of U.S. tight oil production data leads to a single indisputable conclusion: without the advent of the Permian, the U.S. tight oil industry would have lost the OPEC lead price war. Hence, it’s a misnomer to treat the U.S. tight oil industry as a monolith, in many ways, the Bakken and the Eagle Ford tight oil fields are as much a victim of the Permian success as the OPEC nations themselves.

Implications

This discordant panoply of shale fields known as the U.S. tight oil industry has been the key source of global non-OPEC oil supply growth over the last several years and is expected to be for years to come:

(Click to enlarge)

Considering that the majority of U.S. tight oil production growth is generated by a single field, the Permian, changes in the growth outlook of this basin have major implications as to the evolution of global oil prices over the short, medium and long term. Its important to keep in mind that the Permian oil field, despite its large scope, is bound to flatten, peak and decline at some point. While forecasters differ as to the exact year when the Permian oil production will flatten, the majority agree that a slowdown in Permian oil production growth will take place in the early 2020s.

According to OPEC (2018 World Oil Outlook), the Permian basin oil production curve is likely to flatten by 2020, with growth slowing down from 860K barrels in 2018 to a mere 230K barrels by 2020:

(Click to enlarge)

(Source: OPEC WOO 2018)

There are many factors that can accelerate or delay the projected flattening phase, but there is no doubt that sooner or later Permian oil production will flatten. An eventual plateau in Permian oil supply effectively translates into a flattening of non-OPEC global oil supply, the importance of this event can’t be overstated. The year the Permian flattens is the year OPEC will regain control of the market, this seminal event will have major implications on long term oil prices. There is no doubt that Saudi Arabia and Russia are aware of the Permian growth and flattening dynamic and are co-managing their oil supply over the short term and medium term to allow for an orderly entrance of U.S. tight oil supply, aka Permian oil supply, into the market. It’s indeed telling that OPEC is attempting to extend its alliance with Russia for another three years, exactly the time window required for growth in the Permian oil field to flatten and for pricing power to return to it.

The U.S. tight oil story is far more complex than meets the eye, and the oil market, like any market, is prone to the appeal of simple narratives and false conclusions. Those willing to drill behind the headlines stand to capitalize on the treasures buried in the details.

By Nawar Alsaadi for Oilprice.com

More Top Reads From Oilprice.com:

- Hedge Funds Unsure Where Oil Prices Are Going

- Oil Market Tightens On OPEC Cuts

- The Renewable Revolution Has A Lithium Problem

The Permian formation is the place where rapid running can actually take you some place. The resource is rich. If memory serves me correctly, the Permian originally was know as having a unique "stacked" resource of conventional oil. Seems it became an outstanding shale play from out of an illustrious past.

As always, we can't become mesmerized by production volume without keeping close tabs on production cost and market price. We all know that, but do we practice it when the market is exuberant and we're always "bouncing back?"

Some day, U.S. shale oil will be a fond memory, just as conventional oil is becoming. What then? Clean energy seems to be our destiny. At what point do we recognize clean energy as opportunity and clearly necessary?

When judging the impact of US shale oil production on the global oil market and oil prices, observers and analysts alike shouldn’t be duped by the hype doled out day after day by the US Energy Information Administration (EIA) in cahoots with the International Energy Agency (IEA), the Financial Times, Rystad Energy and BP Statistical Review of World Energy about the rising production of US shale oil and how technology is helping to enhance the potential of shale oil.

There are some facts about shale oil which observers and analysts should know before they venture with their opinions and views on the impact of shale oil on the global oil supplies and prices.

The first fact is that the hype can never disguise the fact that shale wells suffer from a steep depletion rate estimated at 70%-90% in their first year of production necessitating the drilling of some 10,000 wells at a cost of $50 bn a year just to maintain production. This will always be the Achilles heel of the US shale oil industry and its eventual demise.

The second fact is that the US shale oil industry will never be profitable now or ever irrespective of oil prices. US shale oil producers are so heavily indebted to Wall Street to the extent that they will continue to produce oil even at a loss just to remain afloat and in so doing they pile more debts. The adage of “robbing Peter to pay Paul” fits them like hand in glove. If this is the case, then there is no long-term future for the US shale oil industry. Within 5-10 years it could be a thing of the past.

The third fact is the bulk of US shale oil production has recently been coming from the Permian which is often described as the best shale play in the world particularly after the steep decline of both the Bakken and the Eagle Ford shale plays in 2016. It is neither technology nor efficiency that saved the US shale oil industry, although these factors may have played a supporting role. In simple terms, the key factor was the Permian oil field.

The fourth fact is that the Permian production is bound to flatten and decline at some point. According to OPEC (2018 World Oil Outlook), the Permian basin oil production curve is likely to flatten by 2020, with growth slowing down from 860,000 barrels a day (b/d) in 2018 to a mere 230,000 b/d barrels by 2020. The Permian is already facing a slowdown resulting from a decline in drilling, well productivity and rig count. Such developments not only definitely argue against any pronounced rise in US oil production, but they also confirm what a pioneer of the US shale oil industry like Continental Resources’ Harold Hamm, the world’s largest oilfield services company ‘Schlumberger’ and many others have been talking about the uncertain outlook for US shale oil output in 2019.

The fifth fact is that considering that the majority of US shale oil production growth is generated by a single field, the Permian, changes in the growth outlook of this basin have major implications for oil prices over the short, medium and long term. An eventual plateau in Permian oil supply effectively translates into a flattening of non-OPEC global oil supply, the importance of this event can’t be overstated. The year the Permian flattens is the year OPEC will regain control of the market. Such a development will have profound implications for long term oil prices.

The sixth fact is that even with a widening gap between the hype by the EIA and its cahoots and the reality about the potential of US shale oil production, the EIA is still projecting a production of 12.1 million barrels a day (mbd) in 2019 and 12.8 mbd in 2020. Moreover, the IEA and Rystad Energy are also projecting that the United States is set to produce more oil and liquids than Russia and Saudi Arabia combined by 2025 surpassing 24 mbd.

Dr Mamdouh G Salameh

International Oil Economist

Visiting Professor of Energy Economics at ESCP Europe Business School, London

Thank you for comments I always find them very informative.