The breakeven cost of producing oil from U.S. shale is roughly the same as non-shale, despite the tidal wave of investment into the sector.

According to the Federal Reserve Bank of Dallas, the breakeven prices for producing oil in the Delaware Basin is $49 per barrel and $48 per barrel in the Midland Basin, both of which are in the Permian. Meanwhile, what the Dallas Fed classifies as “other U.S. nonshale” has a breakeven of $49 per barrel. So, despite all the hype, shale is not more competitive on a cost basis than conventional and offshore production.

Notably, the breakeven price for the Permian outside of the Midland and Delaware basins is $54 per barrel on average. The Eagle Ford sits at $51, and the SCOOP/STACK in Oklahoma at $53.

To be sure, the Dallas Fed notes that these are high-level numbers and don’t account for the enormous amount of variation. The best acreage in the Permian has breakeven prices that are “routinely lower on average than other locations.” Bloomberg New Energy Finance says that breakeven prices in the Permian range from $46 per barrel in Loving County but shoot up to as high as $87 per barrel in Reagan County.

Also, there breakeven prices vary quite a bit between companies, even within the same basic location. “[W]ithin the Permian Basin, for example, individual responses to the most recent survey ranged from $23 to $70,” the Dallas Fed noted.

While shale may have roughly a similar breakeven price as other conventional sources of oil in the U.S., the massive wave of shale output has succeeded in lowering oil prices more broadly. More importantly, because the breakeven price of shale tends to hover between $40 and $60, a much larger volume of oil can come online when prices rise to the upper end of that range. It used to be the case that it would take triple-digit oil prices in order to induce more supply. Related: Saudi Arabia Scrambles To Calm Oil Markets

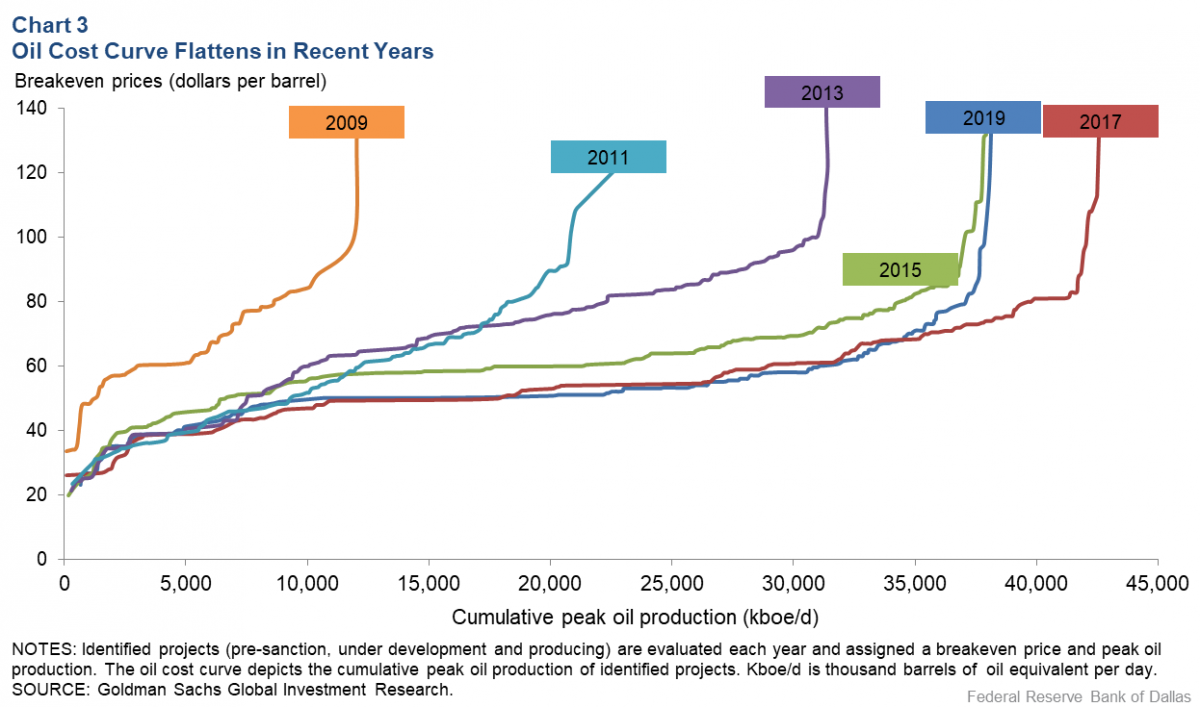

(Click to enlarge)

Another implication is that long-dated oil futures prices are likely to be correlated with these breakeven thresholds. In theory, though not in practice, long-term oil prices should be anchored to the marginal cost of supply. Because shale increasingly accounts for that marginal barrel – more supply comes online when prices rise to the roughly $50-$60 range – U.S. shale could keep a lid on prices for years to come, the Dallas Fed argues.

Similarly, the fast-depleting nature of shale ensures that prices can’t fall too low. As soon as crude prices fall below the breakevens price for shale operators, drilling stops and existing wells quickly deplete, knocking supply offline. That firms up the price.

This is a version of the “shale band” theory popularized a few years ago following the 2014 oil market collapse. While oil has temporarily traded outside of the $40-$60 range – prices crashed below $30 in 2016 and spiked above $70 for WTI last year – they tend to revert back to that range.

Rystad Energy says that U.S. shale will add another 1.1 to 1.2 million barrels per day (mb/d) this year, despite the slow start to the year. Over the medium-term, the IEA says the U.S. will make up the lion’s share of production growth. “This does not rule out the possibility of major oil price movements, but it does point to a strong tendency that oil prices will be range bound in the near future,” the Dallas Fed concluded. Related: Bearish EIA Data Sends Oil Lower

One large caveat to this thesis is that breakeven prices often don’t fully explain profitability, or the lack thereof. In fact, oil prices used to trade above $100 per barrel, but the shale industry burned through hundreds of billions of dollars. To date, despite lower breakeven prices, the industry is still largely cash flow negative.

Even last year, which the IEA expected to be the first year that U.S. shale would become profitable, drillers still burned through capital. Reuters surveyed 29 of the top independent shale companies and all but seven of them were cash flow negative. The group spent $6.69 billion more than they generated. Marathon Oil’s CEO Lee Tillman said that positive cash flow was “aspirational,” according to Reuters.

A separate Wall Street Journal survey from last year of the 30 largest shale producers found a combined $1.7 billion in profits in 2017, after the group burned through $50 billion in losses over the previous five years and over $100 billion in losses over the last 10 years. In reality there is a bifurcated market of companies in distress and other companies doing better.

As Bloomberg noted, this year’s best-performing stock in the oil sector is Hess Corp., which doesn’t have any operations in the Permian.

The drilling boom has been made possible by rock-bottom interest rates and a wave of finance from Wall Street. But with years of capital going up in smoke, it’s not clear how long Wall Street will stomach the losses. The industry is inching closer to positive cash flow, and may in fact reach that goal this year.

But, for investors, there are heftier returns in other businesses, such as new energy tech.

By Nick Cunningham of Oilprice.com

More Top Reads From Oilprice.com:

- Chinese Oil Buyers Shun U.S. Crude

- Natural Gas Prices In The Permian Flip Negative Again

- New Middle East Proxy War Could Jolt Oil Prices

A breakeven price for Saudi and Iraqi oil barrels is estimated at $7.5 and $3 respectively. Saudi and Iraqi oil wells produce on average some 8,500 and 13,700 barrels a day (b/d) respectively compared with 17 b/d for a US conventional well. It will take some 806 American wells to produce the equivalent of one Iraqi well or 500 US wells to match the production of one Saudi well.

At an oil price of $70 a barrel, a US conventional well generates $1190 worth of oil a day compared with $595,000 for a Saudi well and $749,000 for an Iraqi well. That is 500 and 629 times respectively the daily financial worth of a US well.

Furthermore, the claim by Rystad Energy that US shale will add another 1.1 to 1.2 million barrels a day (mbd) this year is hype of the highest order.

A recent report by Post Carbon Institute, one of many authoritative reports of recent times, highlights the fact that technological improvements don’t change the fundamental characteristics of shale production, namely a high depletion rate in US shale wells estimated at 70%-90% in the first year of production, declining well productivity, rising cost of production and declining acreage to allow for growth. They only speed up the boom-to-bust life cycle. The report points out that in 2018 the US shale oil industry spent $54 bn on tight oil plays, 70% of which served to offset field declines and 30% to increase production.

And despite hyped projections by the International Energy Agency (IEA) that US shale oil industry would become profitable in 2018, shale oil producers burned through capital. A survey by Wall Street Journal in 2018 found that the 30 largest shale producers made a combined $1.7 bn in profits in 2017 but only after they burned through $100 bn in losses over the last 10 years.

The US shale oil industry will never be a profitable industry. It is now in a state of decline with production projected to slow down to 10-11 mbd in 2019 and 10 mbd or even less in 2020.

Dr Mamdouh G Salameh

International Oil Economist

Visiting Professor of Energy Economics at ESCP Europe Business School, London