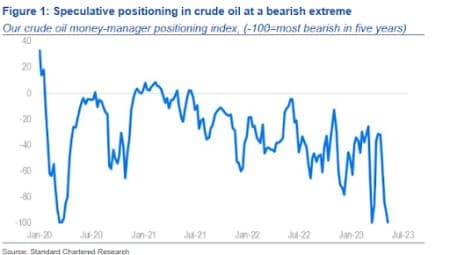

Nowadays, the oil bulls just can’t catch a proper break. After a heavy selloff following the collapse of Silicon Valley Bank routed the markets, the markets returned to a semblance of normalcy after the 2nd of April decision of some OPEC+ members to make voluntary output cuts. Unfortunately for the bulls, the shorts have now returned with a vengeance. According to commodity experts at Standard Chartered, speculative positioning in crude oil has now returned to its March bearish extreme despite the OPEC+ cuts taking effect in the current month.

StanChart has reported that its proprietary crude oil money-manager positioning index fell 8.5 w/w to -99.6, a positioning very similar to the one following the collapse of SVB and also comparable to the positioning at the start of the pandemic in 2020. The analysts have revealed that speculative short positions have increased by 123.9 million barrels (mb) over the past four weeks alone, the largest four-week rise since November 2018, while long positions have declined by 107.9mb over the same period.

But whether the oil price shorts will have their way remains to be seen. After all, Saudi Arabia has often expressed its determination not to give speculators free rein, meaning there’s a high probability that OPEC+ will announce a fresh round of production cuts when it meets on 4th June. The physical oil markets actually remain in relatively good shape, with strong fuel demand boosting prices.

Source: Standard Chartered Research

Oil Economists Turn Positive

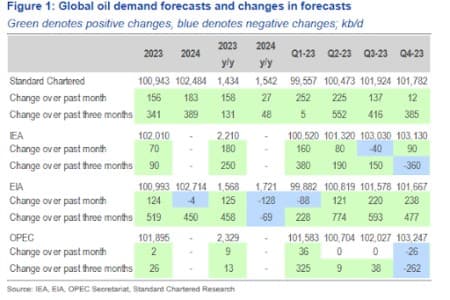

Last month, we reported that energy experts have been growing increasingly bearish on the oil price outlook compared to previous sentiment. Now it turns out that these economists are turning more bullish even as the overall market becomes more bearish.

The International Energy Agency (IEA) published its monthly oil balances report

May, about a week after similar reports were released by the Energy Information Administration (EIA) and OPEC Secretariat. Commodity experts at Standard Chartered have created a heatmap of demand forecast changes, including their own, in the latest reports relative to one and three months ago. You will notice that the heatmap provides a positive view of demand, with most estimates for 2023 quarters and the annual average having moved higher over both time periods. Interestingly, the biggest upwards revisions have come from the more bearish agencies namely StanChart and the EIA, while more bullish ones including the IEA and OPEC Secretariat have not changed significantly. Related: Iraq Awaits Turkey’s Go-Ahead To Resume Kurdistan Oil Exports

In sharp contrast, there’s a disconnect between what energy economists are seeing in the data and what speculative traders are acting on. Oil prices have touched multi-year lows on several occasions over the past two months, with StanChart speculating that the disconnect could be the result of the increasingly top-down and macro-led nature of oil-market sentiment.

Source: Standard Chartered Research

As we have pointed out before, it’s hard to find a proper justification for the growing bearishness in the oil markets.

According to the International Energy Agency, global oil consumption remains on track to rise by 2M bbl/day this year to an all-time high 101.9M bbl/day. Inventories are gradually tightening and should deplete further as OPEC+ implements new production cuts. Crude oil inventories have fallen below the five-year average for the first time this year. Last week, implied gasoline demand rose by 992 thousand barrels per day (kb/d) w/w to a 15-month high of 9.511mb/d.

StanChart has predicted that the OPEC+ cuts will eventually eliminate the surplus that had built up in the global oil markets at the beginning of the year. According to the analysts, a large oil surplus started building in late 2022 and spilled over into the first quarter of the current year. The analysts estimate that current oil inventories are 200 million barrels higher than at the start of 2022 and a good 268 million barrels higher than the June 2022 minimum.

However, they are now optimistic that the build over the past two quarters will be gone by November if cuts are maintained all year. In a slightly less bullish scenario, the same will be achieved by the end of the year if the current cuts are reversed around October. This should shore up prices.

Meanwhile, natural gas prices are expected to increase in the latter half of the year as Europe goes on yet another buying spree. Europe has failed to secure enough long-term LNG contracts to offset cut-off Russian gas imports, with Reuters predicting this may prove costly next winter and could sharply tighten the market. The European Union views natural gas as a bridge fuel in the transition to renewable energy, and buyers generally struggle to commit to long-term contracts. This means that Europe might be forced to buy more from the spot markets as it did in 2022, which in turn is likely to push prices up:

"Since the green lobby in Europe has managed to persuade politicians wrongly that hydrogen to a large extent can replace natural gas as an energy carrier by 2030, Europe has become far too reliant on spot and short term purchases of LNG," consultant Morten Frisch has told Reuters.

By Alex Kimani for Oilprice.com

More Top Reads From Oilprice.com:

- Chevron To Buy Shale Firm PDC Energy In $6.3-Billion Deal

- Alberta Wildfires Still Sapping Crude Oil Production

- Bank Of America Sees Oil Prices Heading Toward $90 This Year

The proof is that Russia’s exports of crude and petroleum products have broken records for the third time in April 2023 when Russian exports hit 8.3 million barrels a day (mbd) or 3.75% higher than pre-Ukraine level of 8.0 mbd.

Therefore, there is no need for a new production cut by OPEC+. Once fears about the US banking system and the health of the US economy subside, oil prices won’t waste time recouping their losses and resuming their surge with Brent crude hitting $90 a barrel in 2023 and even touching $100.

Dr Mamdouh G Salameh

International Oil Economist

Global Energy Expert