Via Metal Miner

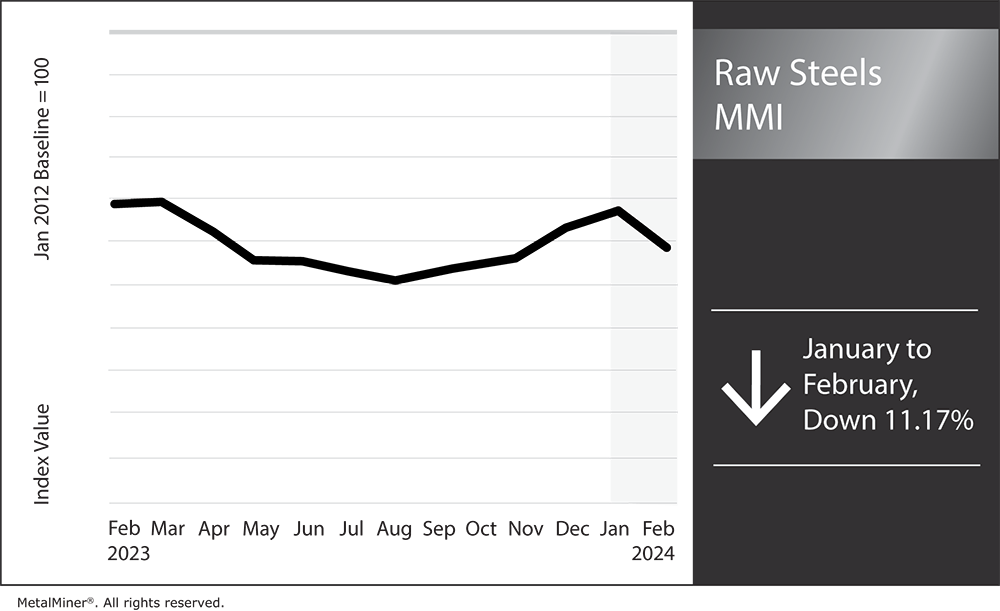

The Raw Steels Monthly Metals Index (MMI) fell 11.17% from January to February as steel prices declined.

U.S. flat rolled steel prices continued to slide after finding a peak at the close of 2023. Following a 2% decline throughout January, hot rolled coil prices fell over 5% during the first half of February. HRC prices now sit at the $1,000/st mark, as bearish momentum appeared to accelerate in recent weeks.

Producer Q4 Results Show Lower Volume Despite Steel Prices Uptrend

In their late January quarterly financial statement releases, both Cleveland Cliffs and Nucor reported slowdowns in steel shipments during Q4 of 2023. While both companies remained profitable, the bearish market conditions led to a significant decrease in earnings.

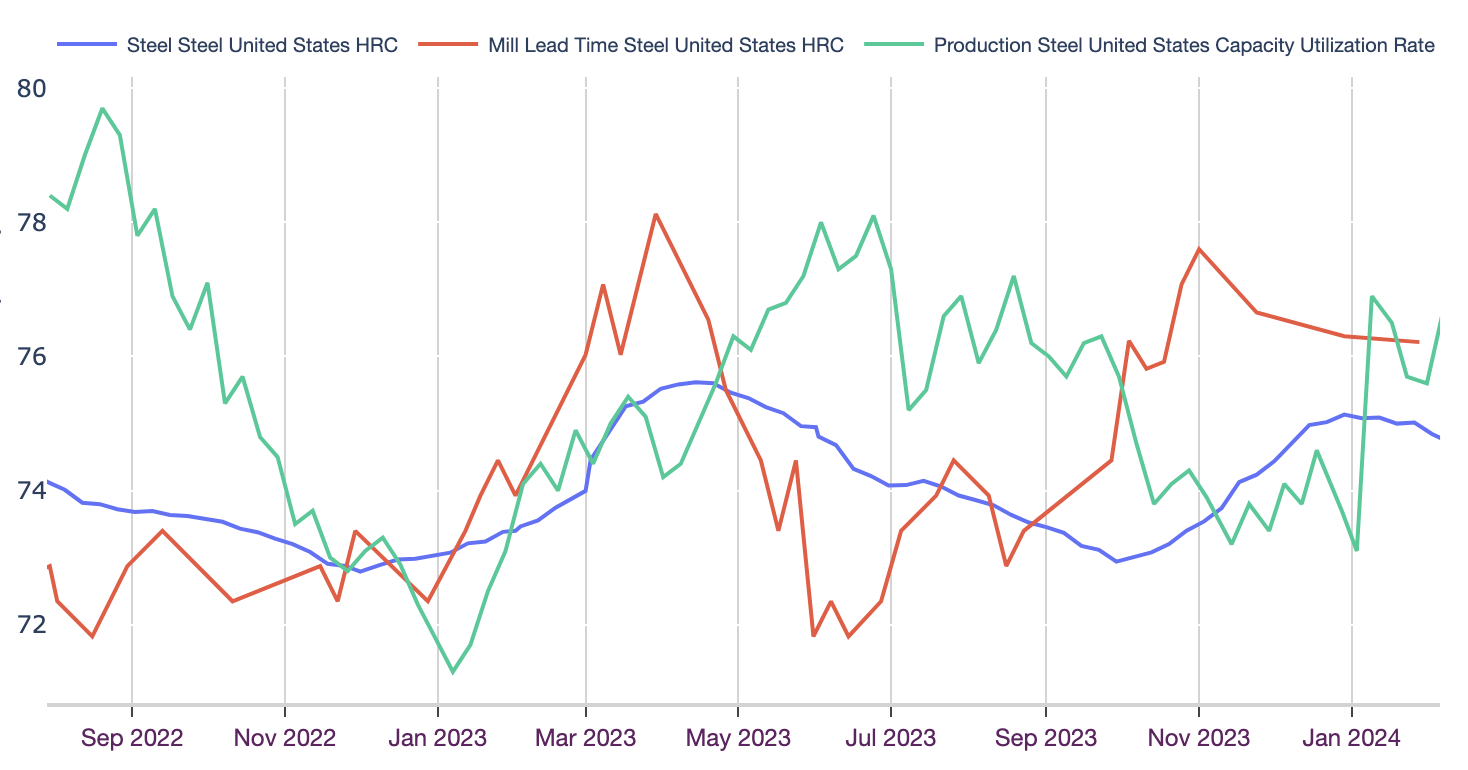

Meanwhile, reports of lower steel shipments from major domestic producers during Q4 contrasted the roughly three-month uptrend seen by flat rolled steel prices. Although HRC, CRC, and HDG prices found a peak at the turn of the year, uninterrupted week-over-week increases saw HRC prices jump by over 61%. By the end of 2023, they were at their highest level since May.

At the start of the uptrend in early October, the market showed no indication of a turnaround. To this day, the manufacturing sector remains in contraction. While subsequently resolved, the UAW strikes offered an additional downside risk to U.S. steel demand. And although steel mill lead times began to stretch longer from their short summer bottom, by October, they remained beneath their historical average, indicating a well-supplied market.

However, the steel price bear trend throughout Q2 saw steelmakers turn the levers on capacity to tackle oversupply within the domestic market. The capacity utilization rate, a leading indicator for steel prices and mill lead times, peaked at the end of June 2023 before mostly trending lower for the rest of the year.

This received some assistance from scheduled maintenance-related outages, which some producers implemented early to stem potential losses from the UAW strikes. Although it took months, domestic steelmakers managed to invert the steel price trend by October as the capacity utilization rate dropped below the 75% mark, where it held through the remainder of Q4.

Steel Producers Expect Q1 Boost

While steel prices appear increasingly weak, both Nucor and Cliffs remain optimistic about the new year. This confidence may explain the recent jump in the domestic raw steel capacity utilization rate after months of discipline among steel producers. According to data from the American Iron and Steel Institute, the raw steel capacity utilization rate hit 76.9% by the end of the first week of January. This represents its highest level since August 2023.

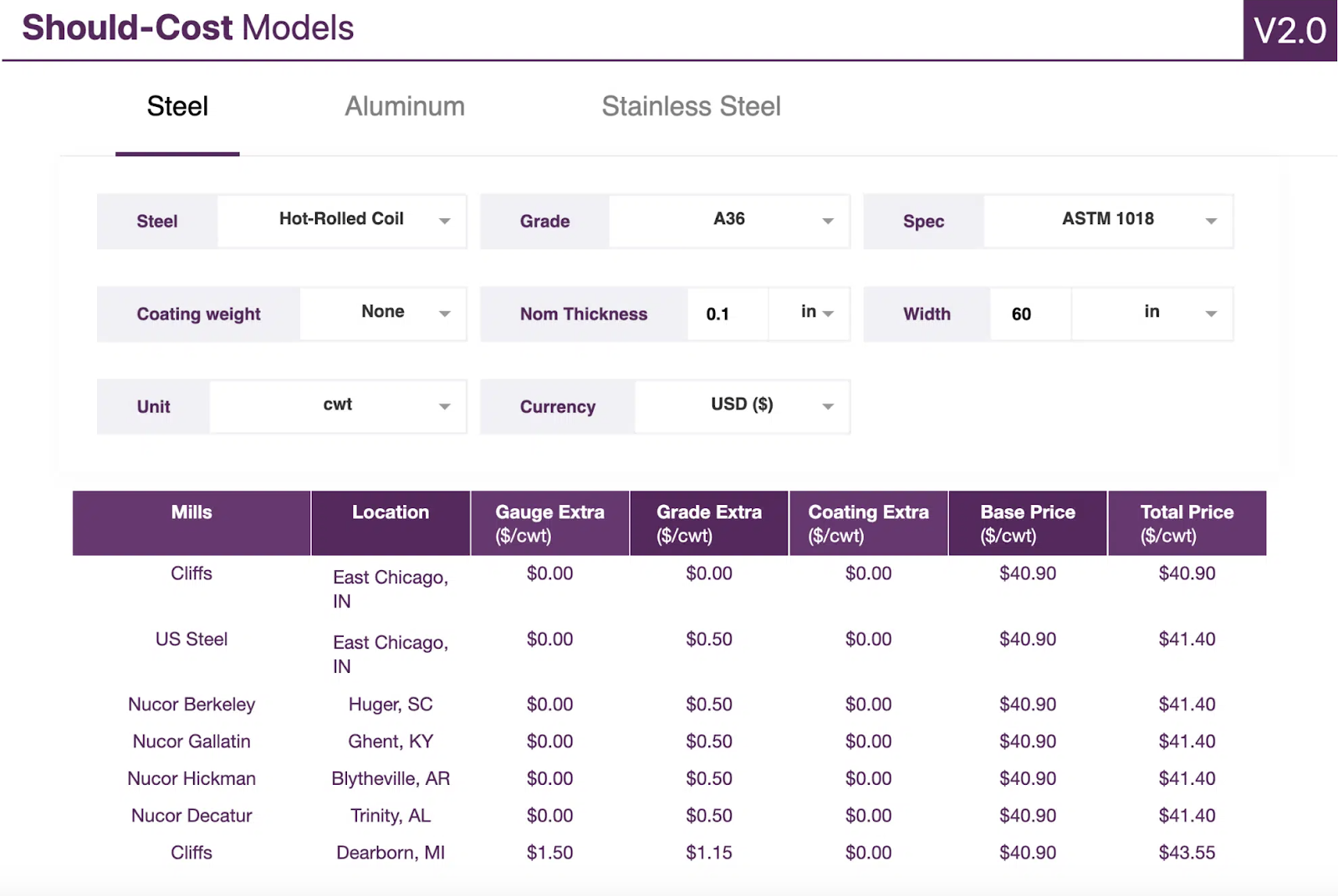

MetalMiner should-cost models: Give your organization levers to pull for more price transparency, from service centers, producers and part suppliers. Explore the models now.

In its Q4 financial report, Nucor said it anticipated a quarterly rise in shipments from Q4 2023 to Q1 2024. That said, increased buying activity at the start of the year remains typical of seasonal patterns. Nonetheless, such a surge would help maintain a tighter market despite the rise in production levels, should it come to fruition. However, as both steel prices and mill lead times have started to slide in recent weeks, the market outlook appears increasingly bearish, which may translate into further downside in the short term.

Trump Vows to Block Nippon-U.S. Steel Sale

As domestic producers lose their grip on steel prices, Japan’s Nippon Steel faces a new setback in its bid to acquire U.S. Steel. Former President Donald Trump told reporters he would block Nippon’s purchase of U.S Steel should he be reelected in November. Following a meeting with the Teamsters union, Trump told media outlets, “I would block it, I think it’s a horrible thing. When Japan buys U.S. Steel, I would block it instantaneously. Absolutely.”

While the outcome of the impending presidential election remains uncertain, Trump’s comments add to a growing list of criticisms of the deal. Although he stopped short of promising to block it, President Biden offered “personal assurances” to the United Steelworkers union following other comments that the sale should receive “serious scrutiny.”

ADVERTISEMENT

Politicians from both parties appear resistant to the potential acquisition of the mill by a foreign buyer. While Nippon successfully negotiated the necessary loan from three of Japan’s megabanks, numerous lawmakers, including Senator John Fetterman, JD Vance, and Marco Rubio, pushed back on the over $14 billion purchase due to national security concerns.

Nippon’s Big Question: Will the Deal Go Through?

The weight of an election year appears to be an increasing risk to Nippon’s efforts to buy U.S. Steel. For one, the United Steelworkers union remains staunchly opposed, with President David McCall stating in early February, “Unfortunately, the proposed sale agreement between Nippon Steel and U.S. Steel puts our members’ and our nation’s interests in jeopardy.” Courting the support of unions, including the USW, could see politicians like Biden adopt a more critical approach to the sale, which could upend Nippon’s bid.

Based on its historical records, Nippon would likely prove much more aggressive than U.S. Steel with regard to price hikes. However, should the sale go through, Nippon would also prevent the further consolidation of the domestic steel sector. Considering the most recent evidence that last quarter’s steel price uptrend did not stem from a turnaround in market conditions but rather steelmaker capacity discipline, the potential failure of Nippon’s purchase appears to be a larger risk to buyers. Furthermore, it would seemingly guarantee the purchase of U.S. Steel by one of the U.S.’s many willing steelmakers.

By Nichole Bastin

More Top Reads From Oilprice.com:

- Banking Giant JP Morgan Exits Climate Action Group

- Buffett’s Berkshire Increases Stake in Chevron and Occidental

- Redox Flow Desalination Offers Potable Water and Energy Storage