After OPEC’s decision not to adjust its production quota, oil prices dropped to their lowest levels since 2009. Oil executives across the world were surely hoping for a different outcome from the meeting in Vienna. Now with the oil rout on – WTI prices plummeted below $70 per barrel after the announcement – all eyes will be on which producers will begin to feel the pain the most.

Saudi Arabia can weather a price crisis longer than most. It has low costs of production; much lower than most other oil producing regions. And despite the fact that it still needs high prices to balance out its budget, Saudi Arabia has built up a vast reserve of foreign exchange to cover deficits. This at least partially explains their motivation to let the market work itself out.

Public oil companies have investors to deal with, and operating in an unprofitable environment is not really a viable option. So the big question is which regions start to become unprofitable at today’s prices that are now approaching the mid-$60-per-barrel range for WTI.

Related: The US Shale Breakeven Price Debate

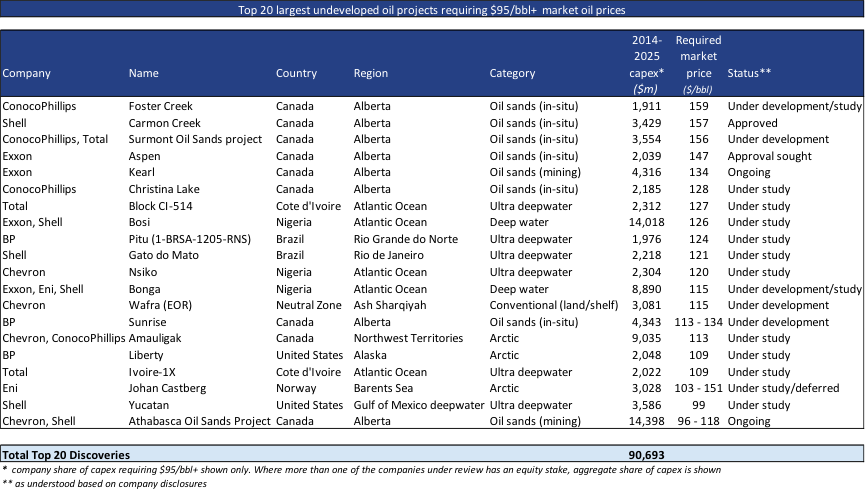

One plausible casualty could be Canada’s oil sands. Not only do oil sands companies produce some of the most expensive oil on the planet, they are also selling oil at a discount. The Western Canada Select, an oil sands benchmark, traded at $48.40 on November 28, the lowest in the world according to Bloomberg. The $17.75 per barrel discount is largely due to pipeline constraints, a fact not lost on environmental groups protesting several major proposed pipelines.

On the other hand, unlike shale companies, oil sands producers invest for the long-term. Oil sands projects often are only profitable with oil prices well above $100 per barrel, but they count on steady production for many years. This is a major difference from shale drillers, who see their production fizzle after an initial burst in the first few years. That means that oil sands producers are not as vulnerable to temporary price fluctuations.

Nevertheless, if oil prices remain below $70 per barrel, expensive oil sands will not be sustainable and Canada’s largest oil sands producers will most likely cut spending. A report from the Bank of Nova Scotia says that drilling in Western Canada may fall by 15 percent in 2015.

Another victim of low prices could be U.S. shale. There is a lot of variation between companies and between regions in terms of who can continue to profitably produce oil from U.S. shale. For example, many Bakken producers can turn a profit at just $42 per barrel.

But an estimated 4 percent of U.S. shale production is unprofitable with oil at $80 per barrel. These are places that operate on the margins in high cost environments – places like the Mississippi Lime formation in Oklahoma or the Tuscaloosa Marine Shale in Louisiana. Companies investing in these formations will see losses pile up, and they will be forced out of the market with prices low.

With WTI now dropping through the $70 per barrel threshold, more regions could become unprofitable. Parts of the Permian basin in Western Texas or the Niobrara in Colorado could begin to look less viable.

Related: 5 Reasons The Halliburton-Baker Hughes Deal Is Poisoned

Still, a study from IHS finds that 80 percent of U.S. shale oil production in 2015 could breakeven at prices between $50 and $69 per barrel for WTI. That means that there will still be a lot of projects out there that oil companies will pursue, but with each passing day as oil prices tumble, more and more could be scrapped.

While oil exploration companies are trembling because of low prices, it may actually be the oil field services companies that are first in the line of fire. Unlike oil producers, which can lean on existing production during lean times, service companies like Schlumberger depend on a steady pace of drilling to stay afloat. With oil majors potentially slated to cut back on drilling activity, demand for drilling services and rigs will be the first thing to go. Schlumberger’s shares have dropped 22 percent over the last three months.

ADVERTISEMENT

Few predicted the price collapse in 2014, so it is anybody’s guess what happens next. However, if prices stay low or drop further, there will be more companies pulling back on drilling, and more of their investors will be clamoring for the exits.

By Nick Cunningham of Oilprice.com

More Top Reads From Oilprice.com:

- Big Oil Going Big In The Gulf Of Mexico

- Russia Expects Oil Price To Rise, But Not Enough To Balance Moscow’s Budget

- What Low Oil Prices Mean For The U.S. Economy

{kind=link}

The $100/barrel are the most expensive projects from the smallest most inneficient companies. 90% of oil sands projects dont require prices that high. Most larger projects are actually $50 to $60 a barrel

I think they bring up the highest figures now because low oil prices are a threat to production and production cuts would begin with the highest cost projects. But current prices certainly woukdnt stop the industry as a whole anytime soon