Drillers and investors who are getting pummeled in the threadbare LNG market might not be sold anymore on the idea that natural gas is the fuel of the future, but it’s not only the future: It’s the key to every major global energy strategy in the world right now.

It’s the key to dominion, and there’s every reason to be patient.

Patience is hard when gas prices have tumbled to multi-year lows.

Gas futures NGc1 prices have dropped to $2.29 per million British thermal units (mmBtu) at the time of this writing, down more than 40% over the past 12 months and the lowest level since May 2016.

A big part of the blame can be pinned on a supply glut coupled with not nearly enough pipeline capacity to transport the commodity.

Gas prices have even turned negative for some Permian Shale drillers

Gas prices at the Waha Hub in West Texas have remained severely depressed, touching a record low of negative $9/mmBtu in April; in essence meaning some drillers are paying other producers to take their gas.

This rather quirky situation happens because drillers who failed to commit to shipments in advance are only allowed to flare their gas for a certain amount of time--up to 6 months in Texas--when faced with low prices after which they must pay other drillers with pipeline space to take it.

Oil and gas output in the Permian has doubled over the past three years making it tough for pipeline infrastructure to keep up despite concerted efforts to add new capacity.

Source: Macrotrends

Yet, against this rather depressing backdrop, to be narrowly rational and overly focused on the short-term outlook could mean leaving big money on the table.

Gas demand continues to grow at a torrid pace (4.9% in 2018, the highest clip since 2010), while big-time infrastructure spending continues to flow into the industry (~$360 billion in 2018)--low gas prices be damned. Related: Emissions Soar As Permian Flaring Frenzy Breaks New Records

Indeed, some industry experts have nailed their colors to their masts with bullish long-term projections for the natural gas industry. The International Gas Union (IGU) has presented yet another strongly bullish yet compelling forecast for the industry.

The bottom line in the bullish theory is that LNG is the kingmaker when it comes to energy strategies.

As far as two decades out, this is the key to energy dominion, if not immense geopolitical power.

Cost Competitiveness

The biggest reason why gas is likely to remain the cornerstone of our green economy is, ironically, the same reason why many investors are fleeing for the hills--low gas prices.

Gas prices have become very competitive vis-a-vis other energy sources. While low spot prices at key hubs due to LNG surplus continue to hog the limelight, the media is missing the big picture here: Deep structural changes including new technology in the upstream market continue to lower breakeven costs, making it economical for drillers to continue production at prices that would have put them out of business just five years ago.

Nearly 70% of the world’s proven gas reserves are fields with an average breakeven price of less than $3/MMBtu. In the midstream section of the market, LNG prices have dropped by an average of 20% over the past two decades while growth of carbon pricing is helping close the gap between natural gas and coal.

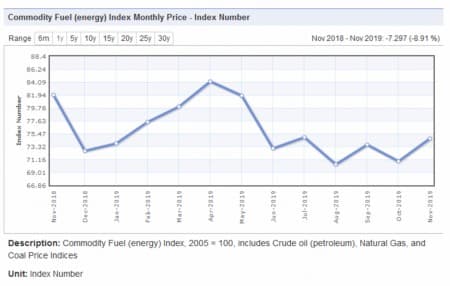

In 2018, natural gas cost 1.72x per MMbtu more than coal compared to 2.2x in 2014. The closing price gap, coupled with carbon pricing, are a big reason why natural gas is rapidly replacing coal as the favored fuel for electricity generation across the globe. In fact, natural gas prices have been falling much faster than any other energy sources--the commodity fuel index that tracks oil, gas, and coal prices has declined just 9% vs. 40.2% by natural gas over the past 12 months.

Source: Index Mundi

Source: Reuters.com

Better Supply Security

We’re a lot more flexible now.

The globe no longer has to rely on a narrow pool of producers with a stranglehold on supply thanks to no less than 21 new producers joining the fray over the past decade. Supply has also become a lot more diversified with the US and Australia becoming major exporters. Further, the LNG market has become much more liquid with spot and short-term sales representing 30% of global sales--a record high.

The pool of natural gas reserves keeps growing every year. Related: The Best And Worst Oil Predictions Of 2019

According to the EIA, proved reserves of natural gas by the United States increased 9% to 504.5 Tcf at year-end 2018, making the country the fourth largest producer and owner of natural gas reserves.

Qatar, the world’s largest natural gas producer, has vowed to become the world’s largest LNG producer as well, while production in Australia, the world’s second largest natural gas producer, has been growing at a quick pace.

Gas as a sustainable resource

The sui generis credential that makes natural gas a standout amongst fossil fuels is its sheer potential to mitigate climate change.

When used in power generation, natural gas emits ~50% less CO2 than coal and 30% less than oil, not to mention that it results in negligible emissions of nitrogen oxides, (NOx), mercury (Hg), sulfur dioxide (SO2), and particulates.

The sobering reality is that as much as we would love to quickly ramp up our renewable energy initiatives and put fossil fuels out of business, we simply won’t be able to do so fast enough to keep up with rapidly growing energy demand. The fossil fuel trifecta of oil, natural gas and coal supply 80% of the world’s energy and have cemented themselves as powerfully incumbent technologies greatly favored by “system inertia” i.e., the resistance to change.

The EIA estimates that natural gas will maintain its current 22% slice in the global energy market by 2040, whereas the fraction by oil+ coal combined is expected to fall quite dramatically.

Further, the IPCC (Intergovernmental Panel for Climate Change) has demonstrated a clear and sustained role for natural gas even under the ambitious 1.5° Celsius target wherein natural gas would still supply 19% of global energy needs by 2040 down from 22% currently.

The 1.5° Celsius scenario calls for global temperature rise due to climate change to be limited to 1.5° Celsius. But with the US having withdrawn from the Paris Accord and emissions remaining high in places like China, the outlook appears really grim—calling for an even faster transition from coal to natural gas.

LNG As The New Norm In Geopolitical Leverage

If you weren’t paying attention, you probably missed the quiet coup recently launched by Qatar, under Saudi-led economic blockade since June 2017.

Qatar found itself being punished by the Saudis and friends for its refusal to go after Iran. The blockade didn’t work. Qatar adapted, and foreign investors were still far too interested in pouring money into the country despite Saudi lobbying to the reverse.

That blockade has effectively been removed without any public fanfare. Last week, Saudi King Salman bin Abdulaziz invited Qatari emir Sheik Tamim bin Hamad Al-Thani to a GCC gathering in Riyadh, which will take place later this month.

The power of natural gas is the dictator here, and the Saudis need what Qatar is the king of. So, not only did LNG allow Qatar to survive the economic embargo, but it also just gave it immense power in regional relations because the fact is, Qatari gas will have to play a key role in Saudi Vision 2030, which calls for reducing reliance on oil for power generation.

The power of LNG is being felt in other ways around the world, as well.

The United States is trying to use this power to reduce Russia’s natural gas stranglehold over Europe, and its touch and go.

The battleground for supremacy is now defined by Russia’s Nordstream 2 pipeline, which the U.S. has waited far too long to truly attempt to stop. It’s gone too far now, and sanctions aren’t likely to lead to victory for Washington in this conflict.

When it comes to Russian piped gas or U.S. LNG, the cost is in favor of Russia’s, but some European countries are willing to spend more for political gain. But not enough, and the German powerhouse is one of them.

LNG is changing everything, and geopolitics is not the least of that.

By. Charles Kennedy for Oilprice.com

More Top Reads From Oilprice.com:

- Oil Hits Three-Month High On Trade Deal Optimism

- Is The Qatar Blockade Coming To An End?

- For The First Time Ever, Shell Signs $10B Emissions Linked Financing

The second inaccuracy is that Qatar is not the world’s number one natural gas producer as the author mentioned in his article. It is number one producer and exporter of LNG and is currently expanding its LNG capacity from 76 million tonnes per year (mt/y) to 110 mt/y by 2023 in order to consolidate its position at the top spot for the foreseeable future against rising competition from Australia, the United States and Russia.

LNG and natural gas have many accolades. They are the kingpin of energy transition from hydrocarbons to renewables, also the largest fuel for electricity generation in the world and are both indispensable factors in helping to mitigate climate change. Even the Intergovernmental Panel for Climate Change (IPCC) has acknowledged that natural gas will still be accounting for 19% of global energy needs by 2040.

There is also a geopolitical dimension to natural gas and LNG. Partly because of natural gas, Russia has emerged as the world’s superpower of energy. It is also the world’s superpower of natural gas since it has the largest proven gas reserves in the globe and is also the largest exporter of gas. Furthermore, it accounts for 40% of the European Union’s (EUs) growing gas market and is now the largest supplier of natural gas to China which is the world’s largest energy market.

Russia’s supremacy in gas supplies will be further enhanced by the completion early next year of both the Nord Sream 2 and Turk Stream gas pipelines which will be bringing more Russian gas supplies to the EU under the Baltic and the Black Seas respectively. Russian position will be further enhanced by the Power of Siberia gas pipeline which was inaugurated two weeks ago and which will be supplying 38 billion cubic meters (bcm) of gas annually to China for the next 30 years.

LNG exports have enabled Qatar to survive a harsh embargo imposed on it by Saudi-led alliance. Once the embargo is lifted, Qatar LNG supplies will help Saudi Arabia and UAE shift electricity generation from oil and gas currently to gas alone thus playing a major role in the diversification of both Saudi Arabia’s and UAE’s economies.

The shale gas revolution has enabled the United States to become a major LNG exporter and has also enabled it to cut domestically CO2 emissions and accelerate a shift from coal to gas in electricity generation.

Dr Mamdouh G Salameh

International Oil Economist

Visiting Professor of Energy Economics at ESCP Europe Business School, London

Clean you your act, stop relying on pr and spin the age of satellite monitoring, and the internet gives proof to your self serving planet killing lies.

The word is out that gas flaring and leakage essentially cancel the above stated potential for NG to compete with coal, relative to climate. Some progress is being made on flaring, leakage and occasional wells gone wild, but maybe not enough to convince some governing bodies. Long-range policy decisions, like no more NG gas hookups new buildings, are being made, including in my neck of the woods.

Can we really be content to stay dependent on fossil fuel, to the extent that we are today?