In the past month, U.S. benchmark crude prices fell significantly, while domestic storage levels posted the largest series of builds so far this year. Lower prices and higher inventories represented trend reversals, highlighting the importance of constantly reassessing the state of affairs in the crude supply chain. In this blog, we will discuss several factors that contributed to the recent turn of events, as well as which components will be particularly important going forward.

Prices and Inventories Lose Ground After Largely Recovering From Multi-Year Oversupply

NYMEX Light Sweet Crude (WTI) front month prices plummeted nearly $10.00/bbl to $66.43/bbl between October 3 and October 23, falling from the highest daily close since November 2014. Prices closed at $67.59/bbl on October 26, remaining relatively low. Before the precipitous drop, WTI prices strengthened $11.40/bbl to $76.41 between August 15 and October 3. Several factors spurred lower prices in recent weeks, including storage builds, refinery maintenance and production growth in the U.S. and abroad.

Meanwhile, total U.S. crude inventories (excluding the Strategic Petroleum Reserve) rose 28.7mn bbls to 422.8mn bbls between weeks ending September 14 and October 19. The overall build was divided between PADDs 2 and 3, according to the U. S. Energy Information Administration (EIA). Stocks at Genscape-monitored storage locations in PADD 2 (Cushing, OK, and Patoka, IL) climbed more than 8.5mn bbls during that time, while inventories at monitored PADD 3 locations (West Texas, Texas Gulf Coast and Louisiana Gulf Coast) increased more than 12.5mn bbls.

U.S. crude stocks began climbing in mid-September, while WTI prices began a decline in early October (Sources: Genscape, CME Group). Click to enlarge

Both crude prices and inventories in the U.S. lost ground after posting a strong recovery in the first three quarters of 2018 from the oversupply that plagued the industry since late 2014. Some recent causes of the bearish reversal, such as refinery maintenance, should have a relatively short-term impact. However, certain drivers, such as growing production, are likely to be in the news headlines for the foreseeable future.

Refinery Maintenance Hinders Demand in the U.S. Mid-Continent

The Mid-Continent is in the midst of the strongest refinery maintenance season in years. The magnitude of unit turnaround was likely caused by two factors. First, refineries typically operate on a multi-year turnaround schedule, and several facilities’ schedules happened to coincide this year. Additionally, multiple refiners opted to defer fall maintenance last year to take advantage of strong margins in the wake of Hurricane Harvey, which bumped projects to 2018. Related: Is Libya's Latest Oil Production Target Too Ambitious?

Primary processing utilization, which includes crude processing units, at Genscape-monitored PADD 2 refineries, averaged below 87 percent for each of the four weeks between weeks ending September 28 and October 19. This was the first time levels dipped that low since April 2016. Utilization rebounded to 86.2 percent for week ending October 19 after slipping to a low of 82.6 percent during week ending October 5.

Primary processing utilization in the U.S. Mid-Continent dipped to the lowest level since April 2016 in October (Source: Genscape). Click to enlarge

The Fall 2018 refinery maintenance in PADD 2 hindered domestic crude oil demand, contributing to storage builds in Cushing and Patoka and putting downward pressure on domestic crude prices. Genscape expects unit restarts to continue in the coming weeks, potentially reversing the recent trend of inventory builds. However, primary processing utilization is not expected to return to the 95 percent level last observed in mid-September until mid-to-late November.

WTI Contracts Reach Widest Contango Structure Since November 2017

Meanwhile, the WTI front-to-second month contract spread switched into a contango structure in mid-October for the first time since May. The front month contract closed at a $0.19/bbl discount to the second month contract on October 23, the widest close since November 2017. The one-month spread remained in a contango structure as of October 26, with front month closing $0.16/bbl lower than second month.

A contango structure signifies that the front month contract price is lower than future month prices. If the spread is wide enough to cover the cost of storage, it opens an opportunity for market participants to buy barrels, store them for an extended amount of time, then sell them for a profit. This phenomenon typically leads to high storage levels, especially at Cushing, which serves as the original delivery point for WTI contracts.

Cushing stocks climbed in October while the WTI one-month contract spread switched into a contacgo structure (Sources: Genscape, CME Group). Click to enlarge

Storage capacity utilization in Cushing did not dip below 50 percent between February 2015 and January 2018. During that time, Genscape’s Cushing Crude Oil Storage Report revealed that Cushing hit a record-high utilization rate of 81 percent in May 2016, largely due to a persistent contango structure. If the current contango structure persists or widens, it could lead to continued storage builds in Cushing.

Permian Basin Drives Domestic Production Growth

While refinery maintenance is expected to conclude relatively soon and the future of contract spreads is unclear, long-term domestic supply growth seems imminent. U.S. crude production volumes averaged about 11mn bpd in September, reaching a record level after increasing nearly 2.5mn bpd from two years prior. The recent increase pushed the U.S. to the top supplier globally ahead of Saudi Arabia and Russia.

Genscape expects U.S. crude production to increase another 1.2mn bpd to more than 12.2mn bpd by September 2019. Ongoing domestic supply growth further contributed to recent stock builds and price decreases.

Production flows in the West Texas Permian Basin increased nearly 1.5mn bpd to more than 3.5mn bpd in the past two years, accounting for the majority of total U.S. growth. Genscape anticipates that this trend will continue, forecasting volumes to increase another 1mn bpd by September 2019, outpacing many Organization of Petroleum Exporting Countries (OPEC) countries.

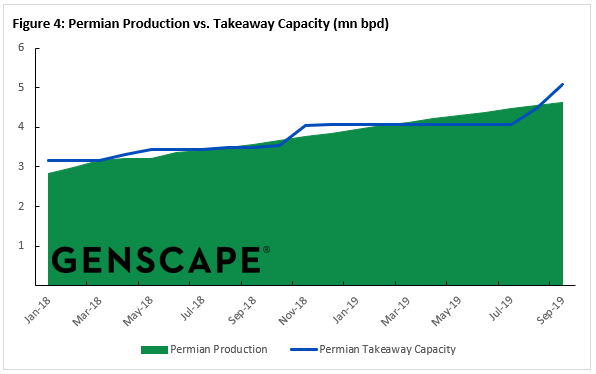

Growing Permian production met takeaway capacity constraints in 2018 (Source: Genscape). Click to enlarge

Supply in West Texas increased so rapidly in the past year that takeaway pipeline capacity became constrained, backing barrels into storage. West Texas crude inventories climbed 6.7mn bbls to 17.7mn bbls between weeks ending June 8 and October 19, accounting for 27 percent of the total Genscape-monitored PADD 3 build since September 14, according to Genscape’s West Texas Crude Storage Report. Related: Oil Prices Buoyed By Draws In Gasoline, Distillate Inventories

Several projects are in the works to increase pipeline capacity out of West Texas. The most immediate relief will come from the Plains All American 24” Sunrise Expansion, which will provide incremental capacity of 500,000 bpd from Midland, TX, to Wichita Falls, TX, allowing for higher flows to the Mid-Continent. Line fill is expected to be completed by October 31, with commercial operations beginning November 1, which is earlier than the original estimate, according to an August 31 FERC filing.

Reports from Genscape and other news outlets in September and October highlighted the upcoming Sunrise expansion and potential increase in supply to the Cushing market, contributing to lower WTI prices and a narrower differential for WTI in Midland. As Sunrise and other pipeline projects expand West Texas takeaway capacity, incremental barrels from the Permian will gain more access to downstream markets. From there, the impact on prices will depend on whether domestic production growth is met by sufficient demand from U.S. refineries and exports to international markets.

Global Supply/Demand Balance Faces Several Uncertainties

Reports of production growth on the international stage also contributed to lower crude prices in October. Saudi Arabia stated on October 23 that it would be ready to meet any demand that materializes, foreshadowing supply increases from the largest producer in OPEC. Meanwhile, Iraq reported that it reached record-high production volumes in late October, and that it has plans to further increase production.

However, increased production from Saudi Arabia and Iraq is likely to coincide with decreased output from other countries. U.S. sanctions on Iranian crude exports commence on November 4, which will likely result in lower production from the OPEC country. However, the depth of the expected cuts remains ambiguous. Some consumers of Iranian crude could continue importing barrels from the country, despite the risk of U.S. sanctions, according to market sources.

There is also significant downside risk for production in other countries. The economic crisis in Venezuela has had considerable ramifications on the country’s oil industry. Venezuelan production is forecast to fall below 1mn bpd by the end of 2019, despite exceeding 2mn bpd in early 2017, according to Genscape’s Global Oil Supply Report. Supply disruptions from other countries, such as Libya and Nigeria, are also plausible, as continual unrest makes production flows unpredictable. To help illuminate changes to production in these countries, Genscape recently combined its proprietary flare signature evaluation methodology with field-level liquids production data in Libya and Venezuela to create its High-Frequency Oil Production Monitor, which is a high-frequency estimate of total oil and other liquids production.

Questions on the supply side come amid reports of economic weakness and lowered projections of global consumer demand. The Dow Jones Industrial Average, the leading indicator for U.S. stock markets, fell considerably in October from near 27,000 October 3 to close at 24,688 on October 26, down 7.98 percent during the month. U.S. stock indices are considered to be a leading indicator of economic health, and the market correction in the Dow in recent weeks stoked concerns of slowing global economic growth.

U.S. real gross domestic product (GDP) increased at an annual rate of 3.5 percent in Q3 2018, which was a slowdown from 4.2 percent in Q2, according to an October 26 U.S. Bureau of Economic Analysis report. Also, this month, OPEC and the International Energy Agency (IEA) both cut their forecasts for oil demand growth through 2019. Widespread economic concerns pose considerable risk on the demand side of the global oil balance, further suppressing crude prices in late October.

With so many variables in flux, the December 5 OPEC meeting is shaping up to be a pivotal milestone for oil prices. Additional insight on OPEC countries’ interpretation of decreased supply from Iran and forecasts of weaker demand growth will inform markets as to what to expect on the supply side in the coming months.

Conclusion

The multitude of variables affecting crude markets present an uncertain story for how the supply/demand balance will progress through the end of the year. Strong refinery maintenance; the contango contract structure; production growth in the U.S. and abroad; and forecasts of lower-than-expected global demand all paint a bearish picture. Prices weakened accordingly in the past month. However, significant risk for international supply disruptions, especially in countries such as Iran and Venezuela, provides strong upside potential for prices.

Key factors to pay attention to in the coming months are U.S. inventories through the end of refinery turnaround; the structure of the WTI forward curve and subsequent storage activity in Cushing; Permian production growth and takeaway capacity additions; Iranian output in the wake of sanctions; and the supply discussion from other OPEC countries, particularly at the next meeting on December 5.

By Genscape

More Top Reads From Oilprice.com:

- Iran’s Worst Nightmare Is Coming True

- Cold Snap Could Send Natural Gas To $5

- Will Iran’s Oil Exports Fall To Zero?