Below are a number of Non-OPEC charts created from data provided by the EIA’s International Energy Statistics.

The charts and table below are primarily for the world’s largest Non-OPEC producers and are updated to July 2019, except for the U.S., which is updated to August 2019. The first set of charts is for Non-OPEC countries with production over 500 kb/d and the last few provide a world overview.

Under some charts are added country comments from the IEA since I have updated data from them up to September 2019. While the IEA production numbers reflect “all liquids”, their July to September increments provide an indication of how the trend in the EIA charts will change by September.

(Click to enlarge)

Listed above are the 14 countries with production greater than 500 kb/d. The largest production increases from one year ago come from the US, Brazil and China. The China chart further down indicates that overall, China is in decline. These 14 accounts for 87% of total Non-OPEC production of 49,620 kb/d in July 2019.

(Click to enlarge)

While Brazil’s 2017 and 2018 production were indicating the beginnings of a plateau or decline, July’s production hit a new high of 2775 kb/d by adding 218 kb/d. An additional 220 kb/d were added in August according to the IEA. Production should exceed 3.0 Mb/d by the end of the year. Brazil started four floating production, storage and offloading units (FPSO) in 2019, according to the IEA.

(Click to enlarge)

Canadian production continues to be limited by the curtailment rules imposed by the Alberta government. As an incentive to producers, the Alberta government is trying to offload the contract to an oil company. It is closing in on a deal to offload the crude-by-rail program to the private sector. A key point for the private sector will be retaining a provision that allows companies to produce more than their quota under the current curtailment rules as long as the additional oil leaves Alberta by rail. Speculation is that Canadian Natural Resources is the front runner since it has been most affected by the curtailment rules. It produces over 1 Mb/d of oil.

(Click to enlarge)

China’s production dropped by 83 kb/d to 3,835 kb/d in July. It is expected to maintain this level of production into 2020 due to increased spending by China’s major oil companies, according to the IEA.

(Click to enlarge)

The EIA has significantly revised its oil production for Egypt. Last month they were showing a drop to 586 kb/d. That has now been revised to 627 kb/d and has been flat since May.

(Click to enlarge)

Kazakhstan increased its production from January 2012 to January 2019. It may be close to peak production now.

(Click to enlarge)

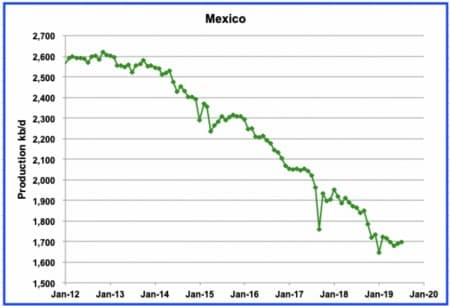

Mexican production is showing signs of stabilizing. The startup of a few small fields has slowed the decline but is not expected to stop it.

(Click to enlarge)

Norway’s production rebounded by 299 kb/d in July to 1,388 kb/d after summer maintenance was completed.

The October IEA report states the following: “On 5 October Equinor brought the much anticipated Johan Sverdrup field online two months ahead of schedule. Phase I of the project is expected to add 440 kb/d of oil production by mid-2020, which will account for over 20% of total Norwegian supply. The initial loading programme suggested that flows in October could average 225 kb/d but most of these cargoes have been delayed to November. However, if the current loading schedule is achieved it implies production at over 300 kb/d on average in November.”

The increased production from the Johan Sverdrup field should begin to show up in the EIA report a few months from now.

(Click to enlarge)

After reaching production of 11,051 kb/d in December 2018, Russia reduced production to 10,709 kb/d to comply with the OPEC+ agreement. For the last two months, Russia has stabilized its production close to 10,750 kb/d as tries to comply with its quota under the agreement.

(Click to enlarge)

Summer maintenance continues to curb the UK’s production. It is expected to return to producing between 1 Mb/d and 1.1 Mb/d once maintenance is complete.

(Click to enlarge)

US August production rebounded to 12,365 kb/d from the July hurricane induced slump. The participants/contributors to this site will continue to debate whether U.S. production will plateau in the near term or continue to rise? The STEO projection out to Feb 2020 has been added to show the EIA’s latest estimates for future production. The October STEO estimate and the actual August production numbers are very close.

(Click to enlarge)

These four countries complete the list of Non-OPEC countries with annual production between 500 kb/d and 1000 kb/d. All four are in decline. Columbia started to increase its production in July 2018, however that has stopped now due to riots. It has investment plans to increase production.

According to Reuters, “Some $700 million in investment spending by oil companies operating in Colombia is frozen because of contract delays caused by community protests and consultations, slow environmental licensing and court orders, the Colombia Petroleum Association (ACP), an industry group, said on Wednesday.”

(Click to enlarge)

World C + C production is down from 84,512 kb/d in November 2018 to 81,204 kb/d in July 2019, a drop of 3.308 Mb/d. Of the 3.308 Mb/d drop, 1.130 Mb/d was contributed by the drop in Non-OPEC during that same period. (See next chart)

Related: Saudi Arabia Bullies Ultra-Rich Into Buying Aramco Stock

The July drop was 505 kb/d and of that, the US accounted for 276 kb/d due to hurricane Barry. The major part of the drop is the reduction associated with OPEC+.

(Click to enlarge)

Non-OPEC production is down by 1,130 kb/d from December 2018 to July 2019. Primary contributors are Canada (-159), Norway (-147), Russia (-300), United Kingdom (-126), US (-231), Malaysia (-151) for a total drop 1,114 Mb/d. The production drop from these countries is related to temporary conditions and more than likely recoverable. However as time goes on, decline in those fields will continue.

(Click to enlarge)

OPEC production is down significantly and is expected to stay down. Will it ever get back to 34,413 kb/d or 34,976 kb/d, not likely using a conservative decline rate of 2% that never sleeps.

(Click to enlarge)

This chart shows two graphs; Non-OPEC W/O total US production and Non-OPEC W/O US LTO. To get the two graphs close and on the same scale, 3500 kb/d were arbitrarily added to the LTO production. As can be seen the trends are very similar. This is probably one of the more critical charts that bears watching in the future. It provides clear evidence that the Non-OPEC producing countries, excluding the US, are on a plateau. This year will be critical since Brazil and Norway are both bringing on new fields with a production capacity of approximately 400 kb/d each. Adding that production to the 37,800 kb/d in July would bring production to 38,600 by the end of the year. Of course, this excludes the decline that never sleeps and is discussed below.

(Click to enlarge)

This chart shows the total oil production from Non-OPEC countries that are experiencing declining production and meet the following two criteria:

1 ) Production declined between December 2014 and December 2018.

2 ) Production declined between December 2014 and July 2019. This second criteria is included to eliminate countries that have begun to increase production in 2019, such as Brazil.

The Red line shows the average decline rate over the last nine years and is slightly more than 30 kb/d/mth. There appears to be a higher decline rate starting in January 2015 and is approximately 48 kb/d/mth or close to 575 kb/d/yr. Using 15,000 kb/d/yr as a reference and the higher decline rate, the yearly decline for these Non-OPEC countries is 3.8%. An interesting case of a country in decline is shown below,

(Click to enlarge)

Shown above are two periods in which Norway’s production was in decline. The first period from January 2010 to January 2012 exhibited a decline rate of 9.62 kb/d/mth. The second from January 2016 to the present shows a decline rate of 8.32 kb/d/mth. The average of the two is 9 kb/d/mth. So while the Johan Sverdrup field is expected to add 440 kb/d of new production over the next year, the decline rate from older fields of slightly more than 100 kb/d/yr will constantly be there.

(Click to enlarge)

In a previous post, the question was raised regarding the recent low annual discovery rate of new fields and how it was close to 1/6 of the oil we consume annually. Above are BP’s estimate of remaining proved oil reserves. Plotted are the 2017 proven reserves (Taken June 2018 report) and 2018 proven reserves (Taken June 2019 report). Note the dramatic decrease in reserve additions after 2011. Also note how the updated 2018 data, shows lower reserve additions from the 2017 data up to 2016.

The jump in 2017 is due to the US adding 11.2 B bbls and Saudi Arabia adding 29.8 B bbls (Getting ready for the IPO??) for a total of 41 B bbls. However, these may be updated reserves in known fields, as opposed to new discoveries. The actual 2017 increase from 2016 was 36 B bbls on the chart. The increase from 2017 to 2018 is only 2 B bbls.

Clearly the world’s oil reserves are in the peaking phase. Considering that the world has consumed close to 1,400 B bbls up to now and there are an additional 1,700 B bbls left, this adds credibility to Dennis’ use of a URR close to 3,100 B bbls. Since we consume close to 30 B bbls annually, the world has about 55 yrs of oil left, provided we can continue to produce and consume C+C at the rate of 80 Mb/d.

By Peak Oil Barrel

More Top Reads From Oilprice.com:

- The Rig Count Collapse Is Far From Over

- The 10 Highest Paying Jobs In Oil & Gas

- The World’s Biggest EV Market Braces For Another Crippling Blow

Iraq is aiming to left its crude oil production from almost 5 million barrels a day (mbd) currently to 6-7 mbd by 2022/2023 but only if political stability and investments permit. In fact, Iraq has the potential to raise its production to 8-9 mbd in the next decade.

Russia is reported to have more than $8 trillion worth of untapped oil and gas in its sector of the Arctic. Oil production from the Russian Arctic could add more than 1.5 mbd to Russia’s current oil production of 11.24 mbd thus consolidating its position as the top oil producer in the world for the foreseeable future.

Brazil could raise its current production of 2.59 mbd to 4 mbd in the next 10 years. But this will not be easy given the extremely challenging oil province where its pre-salt oil reserves exist and the very high cost of production. That is part of the reason why Brazil’s latest oil auction on the 6th of November was virtually a flop with many oil majors including American oil giant ExxonMobil not participating.

Global oil production particularly OPEC’s declined in 2019 not because of peak oil production but because of the trade war between the United States and China. This war has depressed growth prospects of the global economy and also depressed global oil demand and prices. The war has widened the already existing glut in the market from a relatively manageable 1-1.5 mbd before the war to an estimated 4-5 mbd. The glut was big enough to neutralize any geopolitical impact on oil prices and absorb the loss of 5.7 mbd from Saudi oil production.

Dr Mamdouh G Salameh

International Oil Economist

Visiting Professor of Energy Economics at ESCP Europe Business School, London

We think that the earth houses a lot of oil, but when you look at what we've consumed during the last hundred years . . . what's next to burn? Maybe we need to do something different. Let's see, what's our national energy plan?

Within a couple of years of oil production peaking, the global economy will be forced to begin shrinking because of a shortage of energy to transport goods and people around the world. That is a physical fact. It takes oil products to move just about everything, so less liquid fuels available has to mean less products get moved.

Less production and consumption will cause a recession which can't end, since once oil production peaks, the supply of oil will never again increase because it is in finite supply. A downward spiral will begin which, due to the $250 TRILLION of debt, will soon collapse the financial system, as more and more debt goes bad, like nearly happened in 2008. The 2008 global financial crisis was nothing compared to what declining global oil production will cause.

Actually, peak oil is the only thing that is guaranteed to take out the banks, since any other banking problems can be managed by fake money creation out of thin air, if need be. But you can't print up energy obtained from oil. That has to mean shrinking economic activity which fractional banking can't deal with for long. Such a thing has never happened since the Industrial Revolution began. Look out when it does. Don't say you weren't warned.