With the U.S. Energy Information Administration (EIA) projecting that production will outpace demand by 75% in the decades ahead, excess U.S. gas could be a game changer for global importers that have been forced to rely on politically riskier and/or less flexible suppliers.

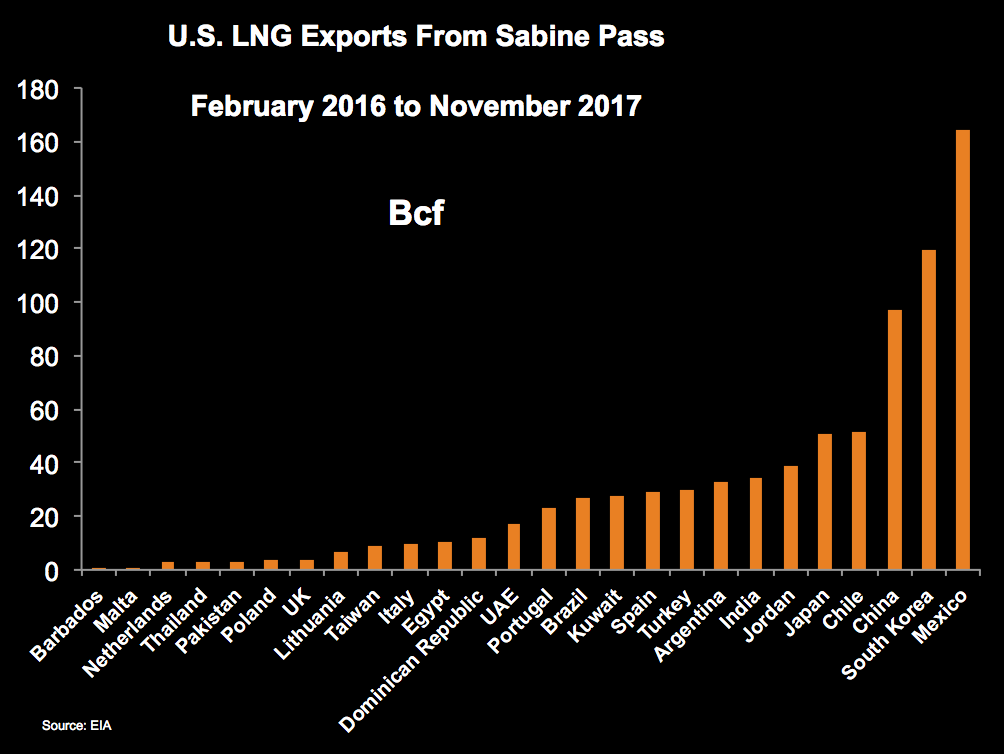

As the only major LNG export terminal in the U.S., Cheniere Energy’s (NYSE:LNG) Sabine Pass in Louisiana has exported about 820 Bcf since operations started in February 2016. Sabine has four liquefaction trains running with an export capacity of 3.3 Bcf/d, and is the flagship of the emerging U.S. LNG export boom that will play out over the next several years.

After numerous delays, Dominion Energy’s (NYSE:D) 0.8 Bcf/d Cove Point terminal in Maryland is set to enter service in early March and become the second major export facility in the U.S.

Four additional projects should come online by the end of 2019, potentially adding 8-10 Bcf/d of U.S. LNG exports to a global market that is soaring toward 45 Bcf/d of total demand. The projects being constructed today should make good headway, as the LNG market is widely expected to reverse from today’s glut to a supply deficit in the early 2020s.

Generally, for U.S. LNG shippers, U.S. free-trade agreements with potential buying nations are seen as vital because they are deemed in the “public interest” and therefore more easily approved FERC and DOE. Yet, the coming U.S. LNG projects have approval to export to countries both with and without free-trade agreements. Related: European Refiners Could Ditch Poor Quality Russian Crude

Looking forward, however, a lack of free-trade agreements could put the U.S. at a competitive disadvantage. The approval process takes longer — an obvious hindrance today because new projects take years to complete and need to start construction soon to be primed for the coming supply shortage. In fact, of the 20 nations that the U.S. has free-trade agreements with, only Chile, Mexico, Jordan, and South Korea could be considered significant LNG importers.

Although Mexico has been America’s main LNG buyer, this should change as the country builds more pipelines to alleviate the bottlenecks with U.S. shippers. This is another reason why the booming Asian market is so coveted by the U.S. LNG industry. China and India — easily the two most vital incremental LNG consumers — don’t make the U.S. free-trade list.

U.S. LNG exports mostly have bipartisan support, and some policymakers seek bills that would remove the distinction between free-trade-agreement and non-free-trade-agreement countries for the industry. The Trump administration has been a vocal supporter of LNG, but a more restrictive trading regime appears to be taking hold that could make the U.S. seem like a less reliable partner.

The good news is that global LNG prices have been rising from historic lows, opening up the arbitrage opportunity for U.S. LNG shippers. Today’s higher oil prices help because most global LNG exports are indexed to oil, in contrast to the nimble U.S. industry that offers attractive spot and short-term contracts that use hub-based pricing and lack the restrictive destination clauses that importers seek to avoid. Related: China’s Becomes World’s Next Top Oil Importer

Indeed, the IEA just predicted that the U.S. could become the largest LNG supplier by the mid-2020s, surpassing current global leaders Qatar and Australia. Gas giant Russia, however, now accounts for 25% of all global gas exports (mostly via pipeline) and understandably seeks a larger role. The LNG importing pool of nations is expected to double to about 80 nations or so in the next 12–15 years.

(Click to enlarge)

By Jude Clemente for Oilprice.com

More Top Reads From Oilprice.com:

- Oil Prices Fall On Rising Crude Inventories

- The Shale Driller's Dilemma

- The World’s Biggest Oil Benchmark Could Change Forever

With global demand for LNG growing by leaps and bounds, Qatar is planning to boost its LNG production capacity by 30% from 77 million tons (mt) currently to 100 mt per year with the aim of maintaining its position as the world’s largest producer and exporter of LNG. Qatar currently accounts for 32% of global LNG demand and 80% of all LNG exports to the Asia-Pacific region. Moreover, Qatar has the world's cheapest LNG production costs.

Then there is Australia which is investing heavily in expanding its LNG production and export capacities. By the 2020 Australia will have a production capacity of 85 mt compared with some 50 mt for the United States.

In 2017 the US exported an estimated 14 mt of LNG and this is projected to rise to 40 by 2020s compared with 70 mt by Qatar and some 60 mt by Australia.

Dr Mamdouh G Salameh

International Oil Economist

Visiting Professor of Energy Economics at ESCP Europe Business School, London