Via Metal Miner

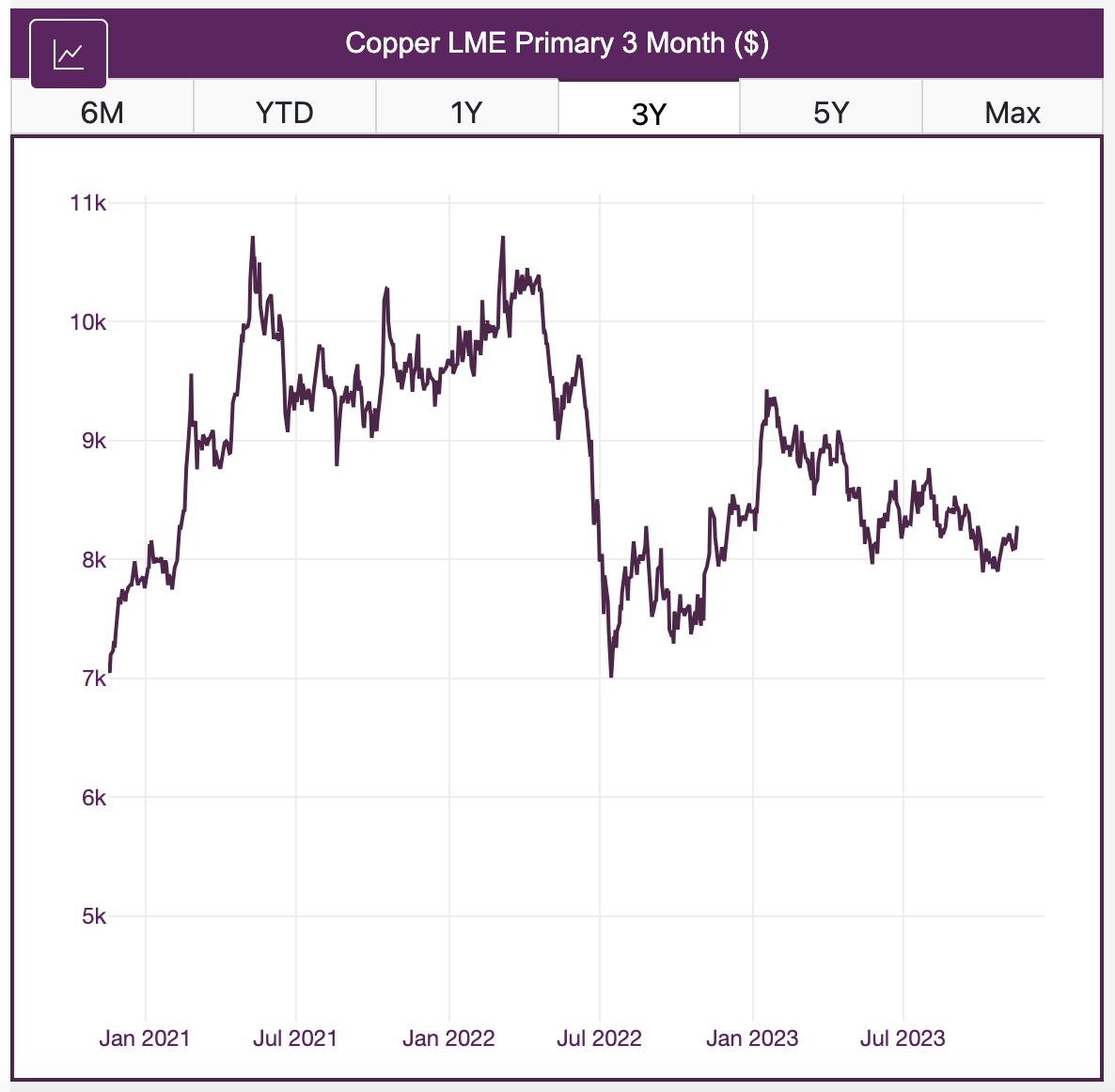

Although they appear on the rebound from last month’s lows, copper prices have yet to break out of their long-term sideways range. Nonetheless, following an almost 2% overall decline throughout October, prices have now retraced to their highest levels since September.

For the second consecutive month, all prices within the index edged lower. That said, the declines proved modest. As a result, the Copper Monthly Metals Index (MMI) remained sideways, with a 0.59% fall from October to November.

EV Inventories Rise as Automakers Back Away from EV Investments

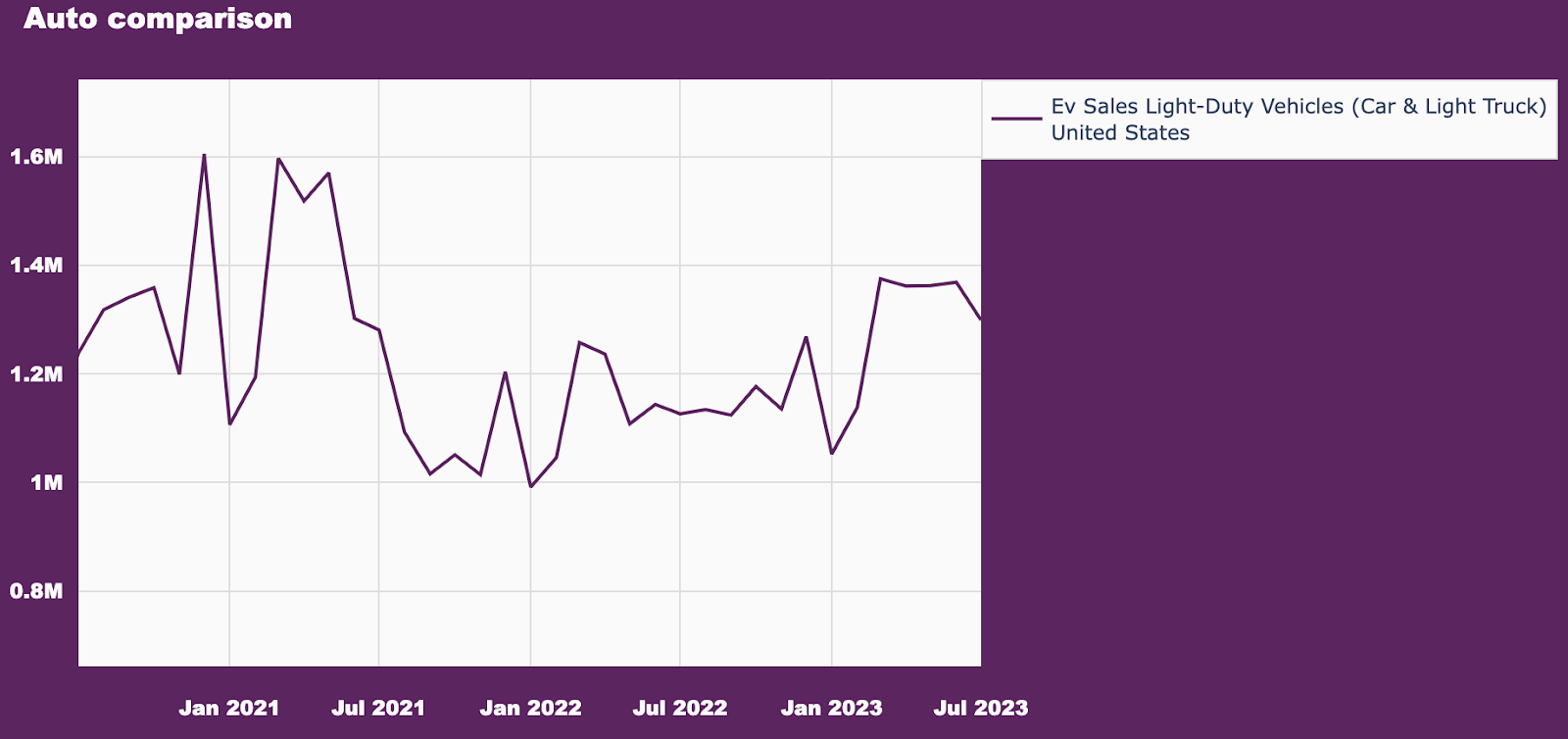

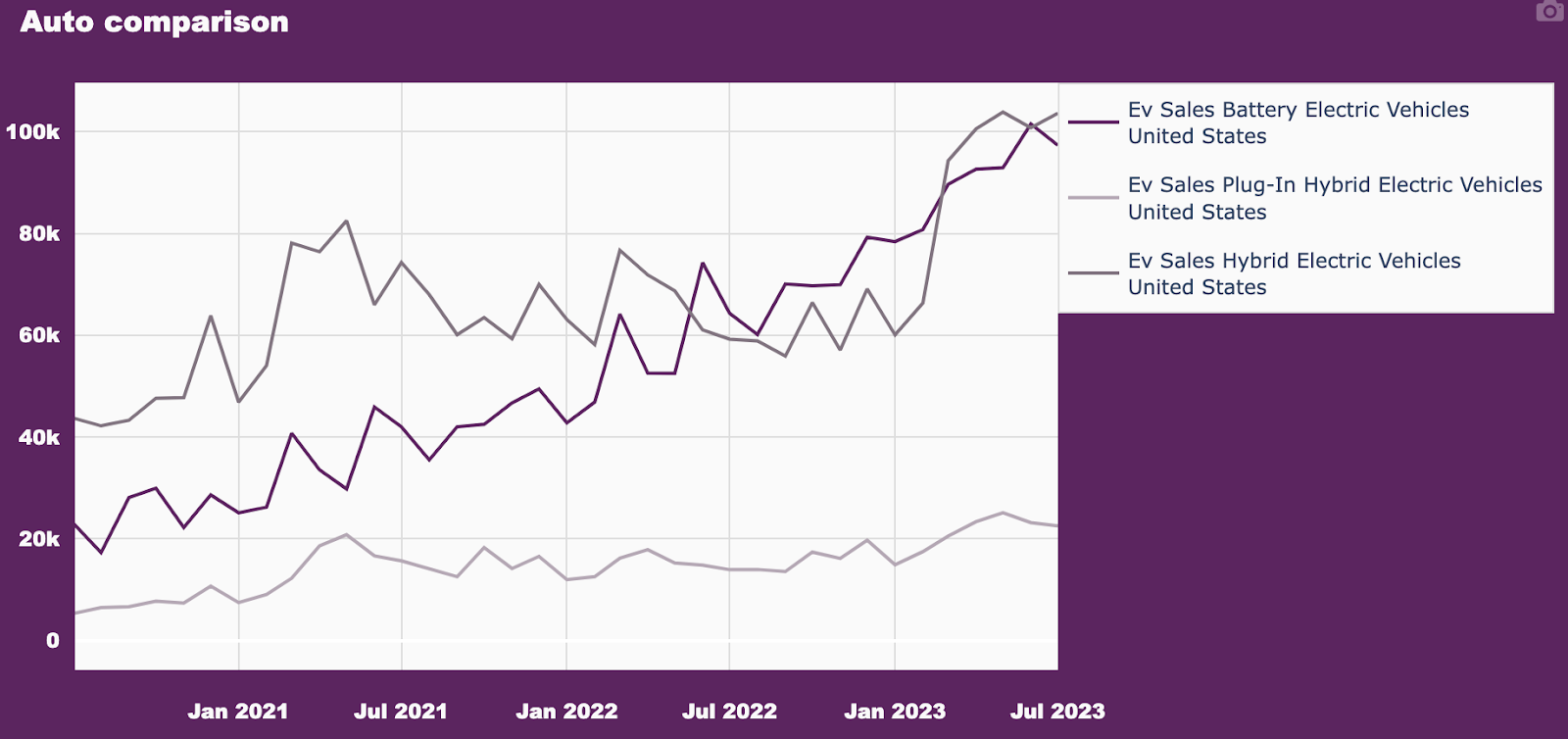

While EV sales remain on the rise, the pace of growth has started to show signs of exhaustion. Should this portend a smaller-than-expected outlook for the sector, commodities like copper could see downwardly revised demand forecasts. This is because EVs require as much as four times more copper than their internal combustion engine (ICE) counterparts.

According to a recent report from CarGurus, U.S. EV inventory levels in October sat 506% above last year’s total. As stocks build, EVs have started to sit on lots for longer periods. Compared to their ICE counterparts, EVs sit on the market an average of 18 days longer.

While CarGurus attributed the apparent slowdown to prices, as EVs have a nearly 28% markup on top of already high interest rates, buyer hesitancy appears more nuanced. Indeed, polls conducted in early 2023 indicated that 47% of respondents had no intention of buying an EV as their next car, often citing a lack of charging stations as a concern.

Automakers appear well aware of slowing growth within the sector, as numerous companies have either curtailed or canceled investments. Among the most recent cuts, GM and Honda called off a $5 billion plan to develop an affordable EV line. Meanwhile, Ford paused work on a Michigan EV battery plant, GM delayed EV truck production until late 2025, and Volkswagen reduced EV production in addition to canceling a new $2 billion factory in Germany. The moves are hardly isolated, as many automakers have shifted their outlook for EVs.

EV’s Still not Widely Purchased Within the US

Just two years ago, automotive sector appeared at the helm of a new era. Major economies began setting carbon emission targets and green-lighting renewable investments to help shift the world’s energy balance away from fossil fuels. In both China and the U.S., that amounted to considerable EV subsidies. President Biden’s even set the target for EVs to represent 50% of auto sales by 2030.

Just six years away from that goal, U.S. EVs have yet to scratch 10% of the overall market. In fact, the share EVs have managed to gain likely already encompasses “low-hanging fruit” like wealthy households and Eco-conscious buyers. In other words, the “easy wins.” To meet its target, the U.S. must win over the remaining consumers, which is a much bigger ask. This latest pullback among automakers seems to suggest that, at the very least, the U.S. will not meet its EV target. Meanwhile, the overall outlook for the sector is completely up to consumer adoption.

Copper Demand in Limbo Amid Two More Wind Project Cancelations

Infrastructure efforts, which have helped support copper prices thus far, are well underway. However, the renewable sector overall continues to face setbacks. In early November, developer Orstead canceled two large offshore wind projects set for construction in New Jersey. Orstead attributed the cancelations to higher interest rates, supply chain problems, and insufficient tax credits.

Higher prices and logistics challenges continue to impact others in the sector similarly. Massachusetts lost two separate projects in recent months, as both SouthCoast Wind and Commonwealth Wind backed out of previously negotiated agreements due to challenging market conditions.

Like EVs, wind development stood as part of a larger bull narrative for copper prices. Indeed, for years, some claimed this would help fuel a forthcoming “supercycle.” Of course, copper demand will continue to benefit from infrastructure spending worldwide. However, the latest challenges seem to suggest that once-lofty forecasts for renewable growth are due for revisions. All said, while copper prices will eventually find an uptrend once again, they may not climb as high or as long as markets previously believed.

Deficit May Offer Support for Copper Prices, But When?

Not all of the “supercycle” narrative has fallen apart. Although demand from the renewable sector appears unlikely to live up to the hype, bullish fundamentals remain within the market from a long-term perspective. Indeed, lower ore grades, protests, and insufficient investment continue to plague the mining industry. While the copper market currently sits in surplus, a deficit still appears on the horizon in the coming years.

MetalMiner Insights covers price points, correlation charts, and price forecasting for a full suite of industrial and precious metals. See our full metals catalog.

However, the widely-expected deficit has yet to hit the market, which continues to grapple with oversupply. Even amid booming output in China and demand from ongoing infrastructure efforts, mine supply remains in glut. Codelco, Chile’s state-owned mining company, saw refining premiums plunge by 36% for 2024. For context, Treatment and Refining Charges (TC/RCs) rise during high demand and tight supply, but decline under opposite conditions.

From a refining perspective, market conditions will offer little support. For example, China will see an 800,000-ton increase in its smelter capacity in 2024. This is in addition to its already robust output levels. The decision stems from China Nonferrous Metals Industry Association’s warnings about overcapacity within the sector, demand not yet living up to supply, and rising LME inventories, which have shown a sharp turnaround in recent months.

By Nichole Bastin

More Top Reads From Oilprice.com:

- 2.8 Billion Tonnes of Metals Extracted Globally in 2022

- EU’s Energy Resilience Tested as Winter Approaches

- Tensions Rise as Azerbaijan Snubs U.S.-Mediated Peace Talks