Via Metal Miner

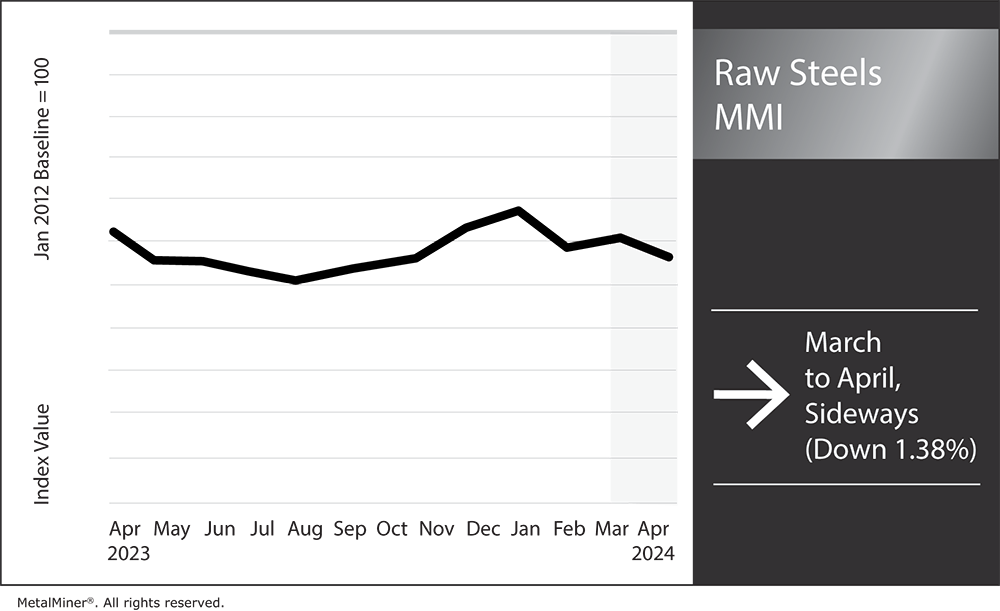

The Raw Steels Monthly Metals Index (MMI) moved sideways, with a modest 1.38% decline in steel prices from March to April.

U.S. flat rolled steel prices continued to trade down throughout March. Meanwhile, HRC prices fell 8.35% to close the month at a new lower low. However, hot rolled coil prices traded up during the first week of April, returning to where they stood in early March.

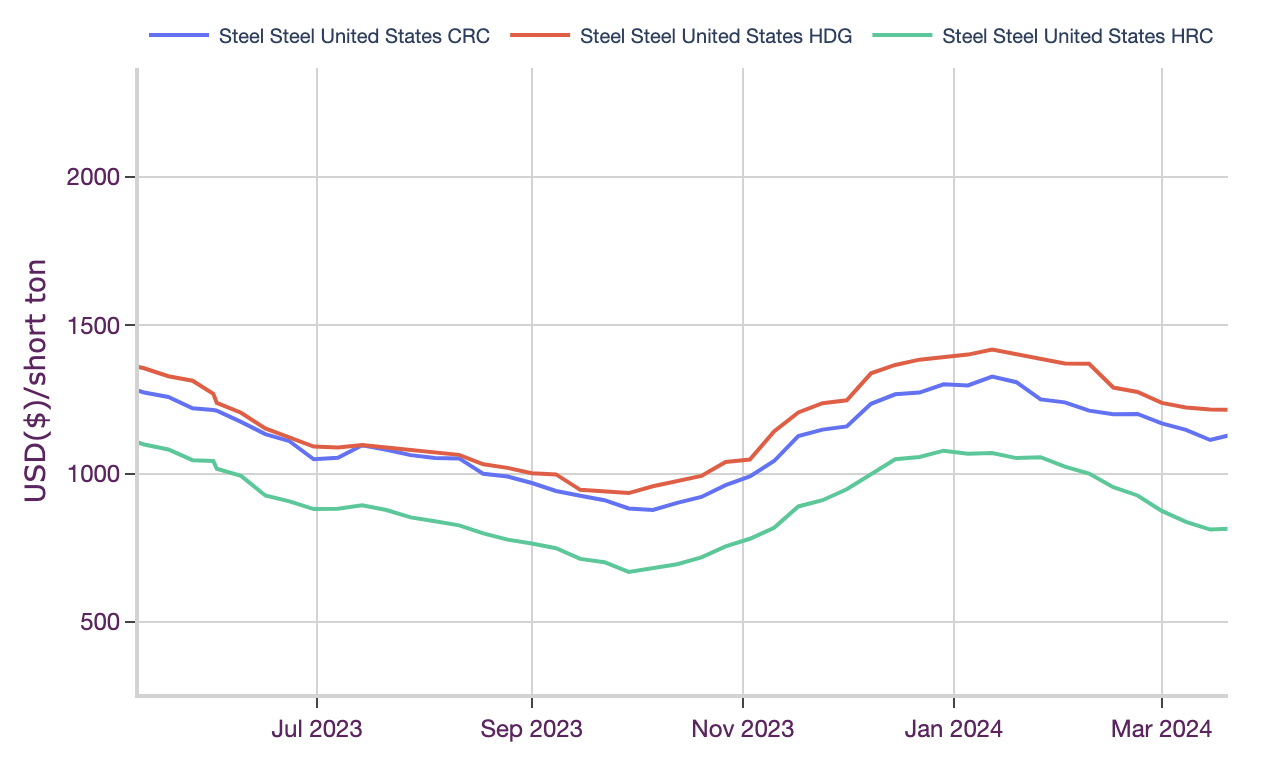

Steel Prices Flatten After Price Hikes

Steelmaker price hikes throughout March offered a visible hurdle to the flat rolled downtrends as steel prices began to move sideways after trading lower last month. HRC and HDG prices showed slight increases during the first week of April after both found a bottom at the close of March. Meanwhile, CRC prices continued to edge lower, still searching for a new bottom. However, the tempo of price declines appeared increasingly slow over recent weeks.

As the steel price downtrends lost momentum, market signals continued to conflict, leading to significant directional uncertainty over the future of the price trends. While they proved enough to stem further losses, price hikes from mills have yet to spark uptrends for steel prices. Cleveland-Cliffs offered the last price hike on March 27, impacting HRC, CRC, and HDG. The $60/st increase brought its minimum HRC price up to $900/st, which is still higher than where HRC prices currently sit at $815/st.

Source: MetalMiner Insights, charts and correlation analysis

By the close of March, mill lead times remained largely unchanged from the previous month, which suggests the supply-demand balance shifted very little during the month. Longer mill lead times also suggest a tighter market. Meanwhile, HRC mill lead times trended slightly shorter throughout March and now sit beneath their long-term average. Though the month-over-month change appeared minimal, supply continued to outpace demand, even as mills initiated maintenance outages that will likely extend through May.

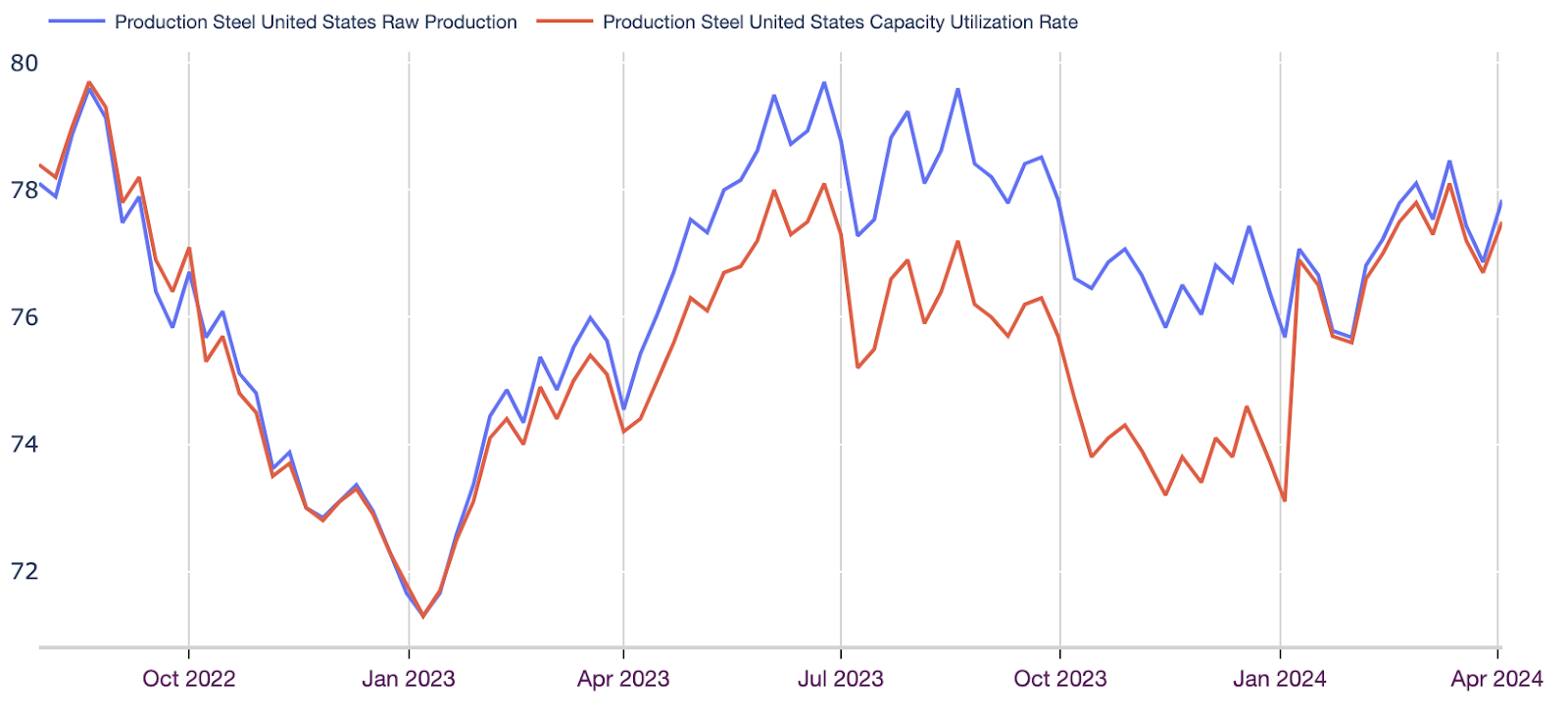

Steel Production Appears Steady Amid Outages

In a bid to spook buyers, mills warned that Spring outages would tighten the supply balance. However, data from the American Iron and Steel Institute show that cuts thus far appeared modest at best. While down from its recent peak in mid-March, raw steel production levels continued to trend higher from Q4 2023 to Q1 2024. Meanwhile, the capacity utilization rate has held above the 75% mark since January.

Source: MetalMiner Insights, Chart & Correlation Analysis Tool

Outages will likely continue to constrain output from its historic highs. Still, absent a meaningful shift in demand conditions, outage cuts may prove too little to tighten the overall market balance. Meanwhile, the ISM Manufacturing PMI returned to growth in March, breaking out of a 16-month negative trend. Sustained growth of the manufacturing sector would offer support to steel demand. However, it may also delay rate hikes from the Federal Reserve in its bid to cool inflation, which means high interest rates will remain an ongoing drag to the U.S. economy.

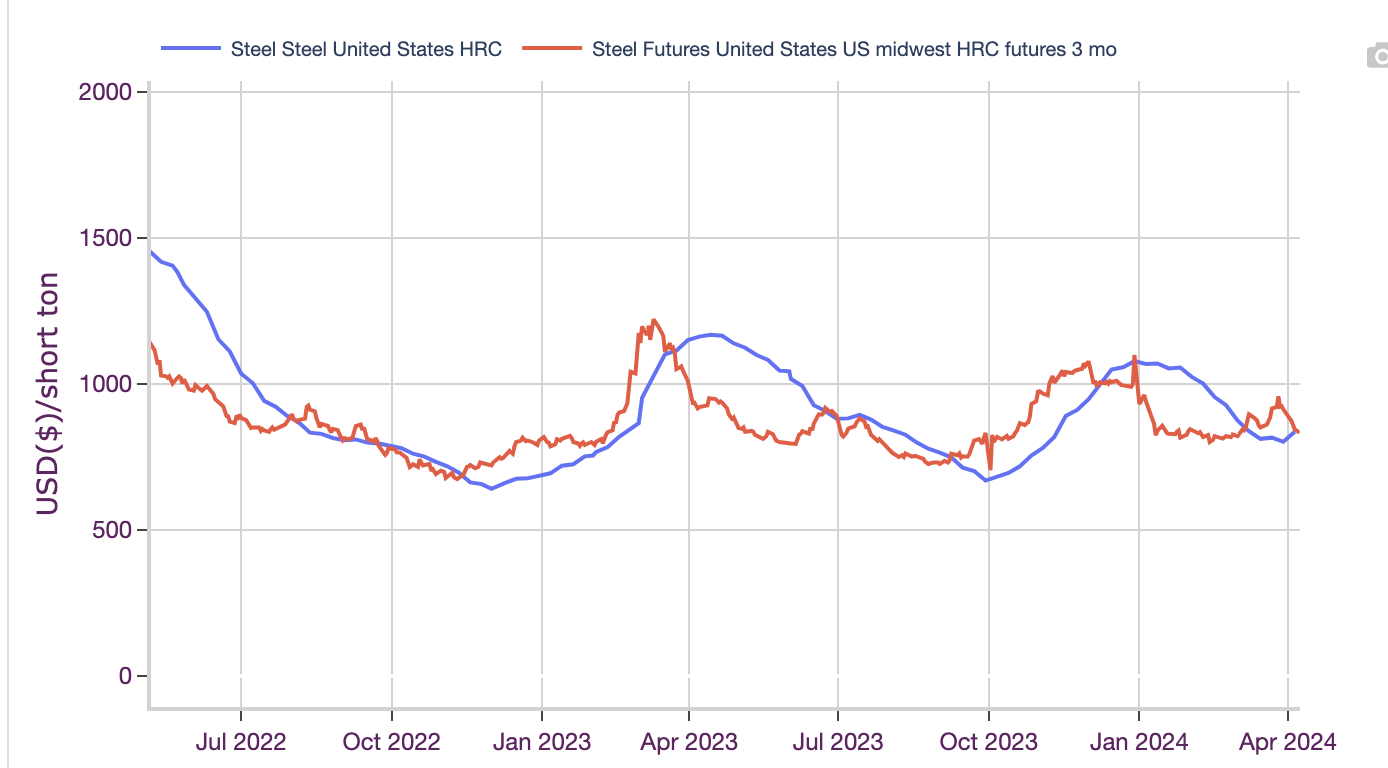

HRC Futures Drift Lower Threatening Market Contango

The HRC spot-futures spread showed an eroding delta by early April. The market experienced a growing contango that peaked by late March, with futures holding a $142/st premium over spot prices. However, buyers’ tepid response to steelmaker efforts to invert the price trend saw market sentiment shift in the ensuing weeks. After HRC futures found a peak at $957/st on March 26, they started to drift lower. By April 5, the premium narrowed to $8/st. While the market remained in contango, backwardation appears increasingly likely should prices continue within their short-term trends.

Source: MetalMiner Insights, Chart & Correlation Analysis Tool

Due to the strong correlation between futures and spot prices, the current direction of HRC futures suggests mills may struggle to secure an uptrend. Mill lead times throughout April will prove telling as to whether producers have executed enough capacity discipline to shore up a seemingly oversupplied market.

By Nichole Bastin

More Top Reads From Oilprice.com:

- Oil Ticks Lower on EIA Inventory Report

- Shell's Undervalued London Listing a "Major Issue," Says Ex-Chief

- China's Mediation Efforts: A Closer Look at Beijing's Ukraine Strategy