The price of oil is down. How should we expect the economy to perform in 2015 and 2016?

Newspapers in the United States seem to emphasize the positive aspects of the drop in prices. I have written Ten Reasons Why High Oil Prices are a Problem. If our only problem was high oil prices, then low oil prices would seem to be a solution. Unfortunately, the problem we are encountering now is extremely low prices. If prices continue at this low level, or go even lower, we are in deep trouble with respect to future oil extraction.

It seems to me that the situation is much more worrisome than most people would expect. Even if there are some temporary good effects, they will be more than offset by bad effects, some of which could be very bad indeed. We may be reaching limits of a finite world.

The Nature of Our Problem with Oil Prices

The low oil prices we are seeing are a symptom of serious problems within the economy–what I have called “increased inefficiency” (really diminishing returns) leading to low wages. See my post How increased inefficiency explains falling oil prices. While wages have been stagnating, the cost of oil extraction has been increasing by about ten percent a year, described in my post Beginning of the End? Oil Companies Cut Back on Spending.

Needless to say, stagnating wages together with rapidly rising costs of oil production leads to a mismatch between:

- The amount consumers can afford for oil

- The cost of oil, if oil price matches the cost of production

The fact that oil prices were not rising enough to support the higher extraction costs was already a problem back in February 2014, at the time the article Beginning of the End? Oil Companies Cut Back on Spending was written. (The drop in oil prices did not start until June 2014.)

Two different debt-related initiatives have helped cover up the growing mismatch between the cost of extraction and the amount consumers could afford:

- Quantitative Easing (QE) in a number of countries. This creates artificially low interest rates and thus encourages borrowing for speculative activities.

- Growth in Chinese spending on infrastructure. This program was funded by debt.

Both of these programs have been scaled-back significantly since June 2014, with US QE ending its taper in October 2014, and Chinese debt programs undergoing greater controls since early 2014. Chinese new home prices have been dropping since May 2014.

Figure 1. World Oil Supply (production including biofuels, natural gas liquids) and Brent monthly average spot prices, based on EIA data.

The effect of scaling back both of these programs in the same timeframe has been like a driver taking his foot off of the gasoline pedal. The already slowing world economy slowed further, bringing down oil prices. The prices of many other commodities, such as coal and iron ore, are down as well. Instead of oil prices staying up near the cost of extraction, they have fallen closer to the level consumers can afford. Needless to say, this is not good if the economy really needs the use of oil and other commodities.

Related: Gains From Low Oil Prices Could Be Wiped Out This Year

It is not clear that either the US QE program or the Chinese program of infrastructure building can be restarted. Both programs were reaching the limits of their usefulness. At some point, additional funds begin going into investments with little return–buildings that would never be occupied or shale operations that would never be profitable. Or investments in Emerging Markets that cannot be profitable without higher commodity prices than are available today.

First Layer of Bad Effects

1. Increased debt defaults. Increased debt defaults of many kinds can be expected, including (a) Businesses involved with oil extraction suffering from low prices (b) Laid off oil workers not able to pay their mortgages, (c) Debt repayable in US dollars from emerging markets, including Russia, Brazil, and South Africa, because with their currencies now very low relative to the US dollar, debt is difficult to repay (d) Chinese debt related to overbuilding there, and (e) Debt of failing economies, such as Greece and Venezuela.

2. Rising interest rates. With defaults rising, interest rates can be expected to rise, so that those making the loans will be compensated for the rising risk of default. In fact, this is already happening with junk-rated oil loans. Furthermore, it is possible that the US Federal Reserve will raise target interest rates in 2015. This possibility has been mentioned for several months, as part of normalizing interest rates.

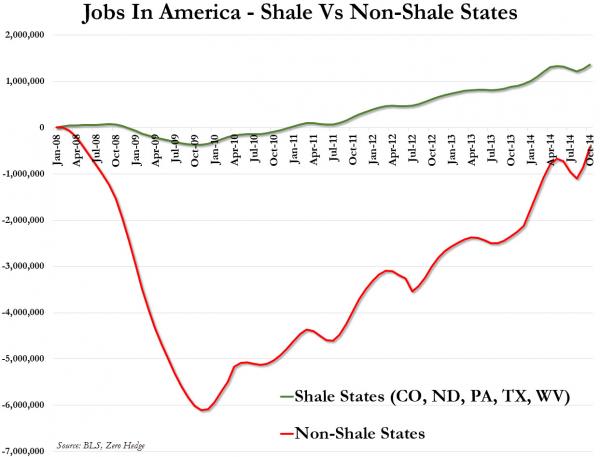

3. Rising unemployment. We know that nearly all of the increased employment since 2008 in the US took place in states with shale oil and gas production. As these programs are cut back, US employment is likely to fall. The UK and Norway are likely to experience drops in employment related to oil production, as their oil programs are cut. Countries of South America and Africa dependent on commodity exports are likely to see their employment cut back as well.

4. Increased recession. The combination of rising interest rates and rising unemployment will almost certainly lead to recession. At first, some of the effects may be offset by the impact of lower oil prices, but eventually recessionary effects will predominate. Eventually, broken supply chains may become a problem, if companies with poor credit ratings cannot get financing they need at reasonable rates.

5. Decreased oil supply, starting perhaps in late 2015. The timing is not certain. Businesses are likely to continue extraction where wells are already in operation, since most costs have already been paid. Also, some businesses have purchased price protection in the derivative market. They will likely continue drilling.

6. Disruptions in oil exporting countries, such as Venezuela, Russia, and Nigeria. Oil exporters generally get the majority of their government revenue from taxes on oil. If oil prices remain low, oil-related tax revenue will drop greatly, necessitating cutbacks in food subsidies and other programs. Some countries may experience overthrows of existing governments and a sharp drop in oil exports. Central governments may even disband, as happened with the Soviet Union in 1991.

7. Defaults on derivatives, because of sharp and long-lasting changes in oil prices, interest rates, and currency relativities. Securitized debt may also be at risk of default.

8. Continued low oil prices, except for brief spikes, because of high interest rates, recession, and low “demand” (really affordability) for oil.

9. Drop in stock market prices. Governments have been able to “pump up” stock market prices with their QE programs since 2008. At some point, though, higher interest rates may draw investors away from the stock market. Stock prices may also decline reflecting the poor prospects of the economy, with rising unemployment and fewer goods being manufactured.

10. Drop in market value of bonds. When interest rates rise, the market value of existing bonds falls. Bonds are also likely to experience higher default rates. The combined effect is likely to lead to a drop in the equity of financial institutions. At least at first, this effect is likely to occur mostly outside the US, because the “flight to security” will tend to raise the level of the US dollar and lower US interest rates.

11. Changes in international associations. Already, there is discussion of Greece dropping out of the Eurozone. Associations such as the European Union and the International Monetary Fund will find it increasingly difficult to handle problems, as their rich countries become poorer, and as loan defaults become increasing problems.

In total, eventually we are likely to experience a much worse situation than we did in the 2007-2009 period, although this may not be evident at first. It will be only over a period of time, after some of the initial “dominoes fall” that we will see what is really happening. Initially, economies of oil importing countries may appear to be doing fairly well, thanks to low oil prices. It will be later that the adverse impacts begin to take over, and eventually dominate.

Major Concerns

Inability to restart oil supply, even if prices should temporarily rise. The production of oil from US shale formations has been enabled by very low interest rates. If there is a major round of debt defaults by the shale industry, interest rates are unlikely to fall back to previously low levels. Because of the higher interest rates, oil prices will have to rise to an even a higher price than required in the past–in other words, to more than $100 barrel, say $125 to $140 barrel. There will also be a lag in restarting production, meaning that high prices will need to be maintained for some time. Bringing oil prices to a high level for a long time seems impossible without crashing the economies of oil importers. See my post, Ten Reasons Why High Oil Prices are a Problem.

Derivatives and Securitized Debt Defaults. The last time we had problems with these types of financial instruments was 2008. Governments around the world made huge payments to banks and other financial institutions, in order to bail them out of their difficulties. The financial services firm Lehman Brothers was allowed to go bankrupt.

Governments have declared that if this happens again, they will do things differently. Instead of bailing institutions out, they will make changes that will make these events less likely to happen. They will also make changes in how shortfalls are funded. In many cases, the result will be a bail-in, where depositors share in the losses by “haircuts” to their deposits.

Unfortunately, from what I can see, the changes governments have made are basically too little, too late. The new sharing of losses will have as bad, or worse, impacts on the economy than the previous government bailouts of banks. Regulators do not seem to understand that models used in pricing derivatives and securitized debt are not designed for a finite world. The models appear to work reasonably well when the economy is distant from limits. Once the economy gets close to limits, many more adverse events occur than the models would have predicted, potentially causing huge problems for the system.1

What we are likely to be encountering now is a combination of defaults of many kinds simultaneously–derivatives, securitized debt, and “ordinary” debt. Many of these risks will be shared among institutions, so that banking problems will be widespread. The sizes of the losses are likely to be very large. Businesses may find that funds intended for payroll or needed to pay suppliers are subject to haircuts. How can they operate in such a situation?

It is even possible that accounts under deposit insurance limits will be subject to haircuts. While deposit insurance is available in theory, the amount held in reserve is not very great. It could easily be exhausted by a few large claims (the scenario in Iceland a few years ago). If governments choose not to make up for shortfalls in funding of the insurance programs, the shortfalls could end up with depositors.

Peak Oil. There seems to be a distinct possibility that we will be reaching the peak in world oil supply very soon–2014 or 2015, or even 2016. The way we reach this peak though, is different from what most people imagined: low oil prices, rather than high oil prices. Low oil prices are brought about by low wages and the inability to add sufficient new debt to offset the low wages. Because the issue is one of affordability, nearly all commodities are likely to be affected, including fossil fuels other than oil. In some sense, the issue is that a financial crash is bringing down the financial system, and is bringing commodities of all kinds with it.

Figure 2 shows an estimate of future energy production of various types. The steep downslope is likely because of the financial problems we are headed into.2

Figure 2. Estimate of future energy production by author. Historical data based on BP adjusted to IEA groupings. Renewables in this chart includes hydroelectric, biofuels, and material such as dung gathered for fuel, in addition to renewables such as wind and solar. (It is based on an IEA inclusive definition.)

A major point of this chart is that all fuels are likely to decline simultaneously, because the cause is financial. For example, how does an oil company or a coal company continue to operate, if it cannot pay its employees and suppliers because of bank-related problems?

Our Long-Term Debt Problem. Long-term debt is an important part of our current system because (a) it enables buyers to afford products, and (b) it helps keep commodity prices high enough to encourage extraction. Unfortunately, long-term debt seems to require economic growth, so that we can repay debt with interest.

Figure 3. Repaying loans is easy in a growing economy, but much more difficult in a shrinking economy.

Economists conjecture that economic growth can continue, even if the extraction of fossil fuels and other commodities declines (as in Figure 2). But how likely is this in practice? Without fossil fuels, we can exchange baby-sitting services and we can give each other back rubs, but how much can we really do to grow the economy?

Almost any economic activity we can think of requires the use of petroleum or electricity and the use of commodities such as iron and copper. A more realistic view would seem to be that without the materials we generally use, our economy is likely to shrink. With this shrinkage, long-term debt will become increasingly impossible. This is one of the big problems we are encountering.

Our Physics Problem. Politicians and businesses of all types would like to advance the idea that our economy will continue forever; the politicians and businesses of every kind are in charge. Everything will turn out well.

Unfortunately, history is littered with examples of civilizations that hit diminishing returns, and then collapsed. Research indicates that the when early economies underwent collapse, the shape of the decline wasn’t straight down–declines tended to take a period of years. Not everyone died, either.

Figure 4. Shape of typical Secular Cycle, based on work of Peter Turkin and Sergey Nefedov in Secular Cycles.

ADVERTISEMENT

Physics gives us a reason as to why such a pattern is to be expected. Physics tells us that civilizations are dissipative structures. The world we live in is an open system, receiving energy from the sun. Examples of other dissipative structures include galaxy systems, the solar system, the lives of plants and animals, and hurricanes. They are born, grow, and eventually stop dissipating energy and die. New dissipative structures often arise, if sufficient energy sources are available to dissipate. Thus, there may be new economies in the future.

We would like to think that we can stop this process, but it is not clear that we can. Perhaps economies are expected to reach limits and eventually collapse. It is only if economies can add large amounts of inexpensive energy resources (for example, by discovering how to make use of fossil fuels, or by discovering a less-settled area of the world, or even by adding China to the World Trade Organization in 2001) that this scenario can be put off.

What Can We Do?

Renewable energy is has recently been advertised as the solution to nearly all of our problems. If my analysis of our problems is correct, renewable energy is not a solution to our problems. I mentioned earlier that adding China to the World Trade Organization in 2001 temporarily helped solve world energy problems, with its ramp up of coal production after joining (note bulge in coal consumption after 2001 in Figure 5). In comparison, the impact of non-hydro renewables has been barely noticeable in the whole picture.

Figure 5. World energy consumption by source, based on data of BP Statistical Review of World Energy 2014. Renewables are narrowly defined, excluding hydro-electric, liquid biofuels, and materials gathered by the user, such as branches and dung.

Guaranteed prices for renewable energy are likely to be an increasing problem, as the cost of fossil fuel energy falls, and as buyers become increasingly unable to afford high energy prices. Issues with banks, making it difficult to pay employees and suppliers, are likely to be a problem whether an energy company uses renewable energy sources or not.

Related: Canada: A Microcosm Of The Ultimate Effect Of Low Oil Prices?

The only renewable energy sources that may be helpful in the long term are one that do not require buying goods from a distance, and thus do not require the use of banks. Trees growing in a local forest might be an example of such renewable energy.

Another solution to the problems we are reaching would seem to be figuring out a new financial system. Unfortunately, debt–and in fact growing debt–seems to be essential to our current system. We can’t extract fossil fuels without a debt-based system, in part because debt allows profits to be moved forward, and thus lightens the burden of paying for products made with a fossil-fuel based system. If a financial system uses only on the accumulated profits of a system without fossil fuels, it can expand only very slowly. See my post Why Malthus Got His Forecast Wrong. Local currency systems have also been suggested, but they don’t fix the problem of, say, electricity companies not being able to pay their suppliers at a distance.

Adding more debt, or taking steps to hold interest rates even lower, is probably the closest we can come to a reasonable way of temporarily putting off financial collapse. It is not clear where more debt can be added, though. The reason current debt programs are being discontinued is because, after a certain level of expansion, they primarily seem to create stock market bubbles and encourage investments that can never pay back adequate returns.

One possible solution is that a small number of people with survivalist skills will make it through the bottleneck, in order to start civilization over again. Some of these individuals may be small-scale farmers. The availability of cheap, easy to use, local energy is likely to be a limiting factor on population size, however. World population was one billion or less before the widespread use of fossil fuels. We don’t have much time to fix our problems. In the timeframe we are looking at, the only other solution would seem to be a religious one. I don’t know exactly what it would be; I am not a believer in The Rapture. There is great order underlying our current system. If the universe was formed in a big bang, there was no doubt a plan behind it. We don’t know exactly what the plan for the future is. Perhaps what we are encountering is some sort of change or transformation that is in the best interests of mankind and the planet. More reading of religious scriptures might be in order. We truly live in interesting times!

Notes:

[1] Derivatives and Securitized Debt are often priced using the Black-Scholes Pricing Model. It assumes a normal distribution and statistical independence of adverse results–something that is definitely not the case as we reach limits. See my 2008 post that correctly forecast the 2008 financial crash.

[2] Points are plotted at five-year intervals, so the chart is a bit more pointed than it would have been if I had plotted individual years. The upper limit at 2015 is an approximation–it could be a year or so different.

By Gail Tverberg

Source - http://ourfiniteworld.com/

More Top Reads From Oilprice.com:

- Global Economy At Risk From Oil Price Dive

- Five Geopolitical Predictions for 2015

- Does The Oil Market Care Who Sits On Saudi Throne?

{kind=link}

are you serious? really?

The only hope we have of replacing the current failed un-sustainable world order with something better is to NOT listen to clowns like you.

Next up if I was in charge would be selling of only non coupon bonds, where there would be no payments for the ten year life of the bond but all due at the time of maturity. Why would other countries buy these? because we are the mother ship, they need us to survive and be healthy and it makes them healthier.

IT IS NOT CLEAR WHO WILL TAKE THIS HIT IN THE SYSTEM.ALREADY ONE COMPANY IN THE E&P SPACE HAS DECLARED BANKRUPTCY.A 2008 LIKE SITUATION SEEMS TO BE DEVELOPING WITH NO RECOVERY IN SIGHT OF CRUDE OIL PRICES.MONEY SHALL MOVE OUT OF RISKIER ASSET CLASSES LIKE EQUITY TO SAFER HEAVENS IS FEARED.AWAIT YOUR COMMENTS ON THE SAME.

WARM REGARDS.

do you think ,

in first that the rise of coal sales

(and the fact that we have 400 years of coal reserves !)

is the actual trigger for the temporary decline of the barrel of oil ?

strong stability of the 'nat gas' + strong stability of the 'coal '

= less tension on oil?

in second : the age of 'internet' with less consumption in oil

in developed country.

your source:World energy consumption by source, based on data of BP Statistical

But...what if the price of oil is simply not being driven by supply and demand, or indeed any macroeconomic factors?

What if, as I highly suspect, the price of oil is being driven by political considerations and actors, that are interfering intentionally with oil pricing mechanisms in order to destabilise certain oil producing countries - namely Russia? Or are being used as a proxy weapon amongst Muslim oil producers as part of the on-going Sunni - Shite campaign?

There is no history of the Saudis driving production in the face of cratering oil prices...such market dynamics have nearly always resulted in the Saudis leading OPEC to restrain production. And yet...weeks and weeks into depressed oil pricing, the Saudis are not backing down and reducing production. Instead, they are in full-tilt production, which given the depressed prices they are receiving is costing them quite a bit of revenue.

I would posit to the author that this cannot be explained by macroeconomic factors, and is most likely driven by an "agreement" with the US to punish Russia for their military actions and destabilise Putin's government (which is working), or a broadside against Shite Iran from the Saudis themselves over the sectarian Muslim conflicts in Syria and Iraq. Or both - nothing says it might not be planned with dual purposes.

In my mind the steepness of the decline of pricing, and the behaviours of the Saudis against their historical norms indicated that this is a planned decrease...don't look at economic data to predict when it will end, instead look at the political pages, and monitor the health of Putin's government and/or the Syrian war progress.

END TIMES= GAME. OVER